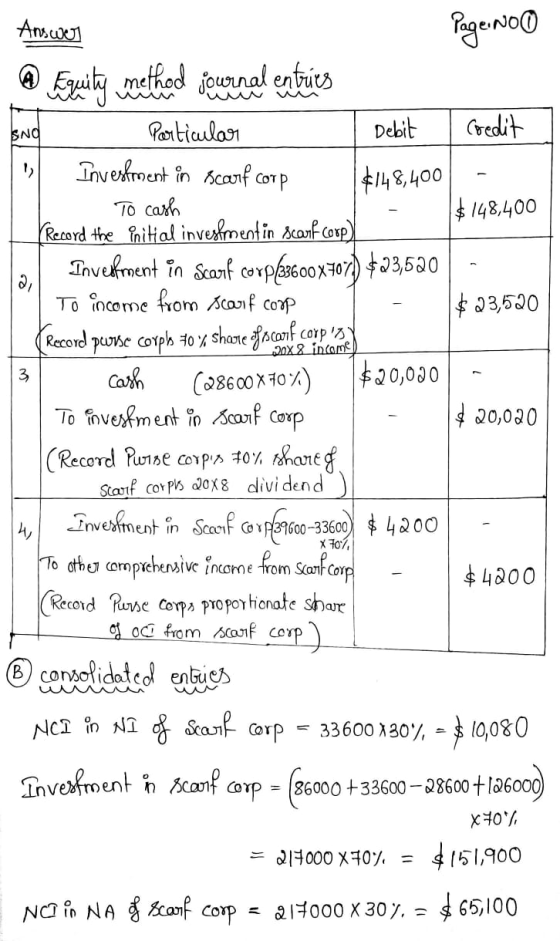

A. Purse Corporation acquired 70 percent of Scarf Corporation's ownership on January 1, 20X8, for $148,400....

A. Purse Corporation acquired 70 percent of Scarf Corporation's ownership on January 1, 20X8, for $148,400. At that date, Scarf reported capital stock outstanding of $126,000 and retained earnings of $86,000, and the fair value of the noncontrolling interest was equal to 30 percent of the book value of Scarf. During 20X8, Scarf reported net income of $33,600 and comprehensive income of $39,600 and paid dividends of $28,600.

Required:

a. Present all equity-method entries that Purse would have recorded

in accounting for its investment in Scarf during 20X8. (If

no entry is required for a transaction/event, select "No journal

entry required" in the first account field.)

1. Record the initial investment in scarf corp.

2. Record Purse Corps 70% sgare of scarf corps 20X8 income

3. Record Purse Corps 70% sgare of scarf corps 20X8 dividend

4. Record Purse corps proportionate share of OCI from Scarf corp

B. Present all consolidation entries needed at December 31, 20X8, to prepare a complete set of consolidated financial statements for Purse Corporation and its subsidiary. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)

1. Record the basic cosolidation entry

2. Record the other comprehensive income entry

Homework Answers

Add Answer to:

A. Purse Corporation acquired 70 percent of Scarf Corporation's

ownership on January 1, 20X8, for $148,400....

Purse Corporation acquired 70 percent of Scarf Corporation’s ownership on January 1, 20X8, for $145,600. At...

Purse Corporation acquired 70 percent of Scarf Corporation’s ownership on January 1, 20X8, for $145,600. At that date, Scarf reported capital stock outstanding of $124,000 and retained earnings of $84,000, and the fair value of the noncontrolling interest was equal to 30 percent of the book value of Scarf. During 20X8, Scarf reported net income of $32,400 and comprehensive income of $38,400 and paid dividends of $27,400. Required: 1. Present all equity-method entries that Purse would have recorded in accounting...

Palmer Corporation acquired 70 percent of Krown Corporation’s ownership on January 1, 20X8, for $148,400. At...

Palmer Corporation acquired 70 percent of Krown Corporation’s ownership on January 1, 20X8, for $148,400. At that date, Krown reported capital stock outstanding of $126,000 and retained earnings of $86,000, and the fair value of the noncontrolling interest was equal to 30 percent of the book value of Krown. During 20X8, Krown reported net income of $33,600 and comprehensive income of $39,600 and paid dividends of $28,600. Required: a. Present all equity-method entries that Palmer would have recorded in...

Palmer Corporation acquired 70 percent of Krown Corporation’s ownership on January 1, 20X8, for $149,800. At...

Palmer Corporation acquired 70 percent of Krown Corporation’s ownership on January 1, 20X8, for $149,800. At that date, Krown reported capital stock outstanding of $127,000 and retained earnings of $87,000, and the fair value of the noncontrolling interest was equal to 30 percent of the book value of Krown. During 20X8, Krown reported net income of $34,200 and comprehensive income of $40,200 and paid dividends of $29,200. Present all equity-method entries that Palmer would have recorded in accounting for...

Purse Corporation owns 70 percent of Scarf Company’s voting shares. On January 1, 20X3, Scarf sold...

Purse Corporation owns 70 percent of Scarf Company’s voting shares. On January 1, 20X3, Scarf sold bonds with a par value of $705,000 at 98. Purse purchased $470,000 par value of the bonds; the remainder was sold to nonaffiliates. The bonds mature in five years and pay an annual interest rate of 8 percent. Interest is paid semiannually on January 1 and July 1. Required: a. What amount of interest expense should be reported in the 20X4 consolidated income statement?...

Purse Corporation owns 70 percent of Scarf Company’s voting shares. On January 1, 20X3, Scarf sold...

Purse Corporation owns 70 percent of Scarf Company’s voting

shares. On January 1, 20X3, Scarf sold bonds with a par value of

$675,000 at 98. Purse purchased $450,000 par value of the bonds;

the remainder was sold to nonaffiliates. The bonds mature in five

years and pay an annual interest rate of 8 percent. Interest is

paid semiannually on January 1 and July 1.

Required:

a. What amount of interest expense should be reported in the 20X4

consolidated income statement?...

Purse Corporation owns 70 percent of Scarf Company’s voting

shares. On January 1, 20X3, Scarf sold bonds with a par value of

$675,000 at 98. Purse purchased $450,000 par value of the bonds;

the remainder was sold to nonaffiliates. The bonds mature in five

years and pay an annual interest rate of 8 percent. Interest is

paid semiannually on January 1 and July 1.

Required:

a. What amount of interest expense should be reported in the 20X4

consolidated income statement?...

Price Corporation acquired 100 percent ownership of Saver Company on January 1, 20x8, for $158,000. At...

Price Corporation acquired 100 percent ownership of Saver Company on January 1, 20x8, for $158,000. At that date, the fair value of Saver's buildings and equipment was $32,000 more than the book value. Buildings and equipment are depreciated on a 10-year basis. Although goodwill is not amortized, Price's management concluded at December 31, 20x8, that goodwill involved in its acquisition of Saver shares had been impaired and the correct carrying value was $5,500. Trial balance data for Price and Saver...

Price Corporation acquired 100 percent ownership of Saver Company on January 1, 20x8, for $158,000. At that date, the fair value of Saver's buildings and equipment was $32,000 more than the book value. Buildings and equipment are depreciated on a 10-year basis. Although goodwill is not amortized, Price's management concluded at December 31, 20x8, that goodwill involved in its acquisition of Saver shares had been impaired and the correct carrying value was $5,500. Trial balance data for Price and Saver...

Ravine Corporation purchased 40 percent ownership of Valley Industries for $116,400 on January 1, 20X6, when...

Ravine Corporation purchased 40 percent ownership of Valley Industries for $116,400 on January 1, 20X6, when Valley had capital stock of $246,000 and retained earnings of $45,000. The following data were reported by the companies for the years 20X6 through 20X9: Dividends Declared Operating Income, Net Income, Valley Year Ravine Corporation Valley Industries Ravine 20X6 20X7 20X8 20X9 $149,000 94,000 224,000 169,000 $41,000 61,000 10,000 51,000 $ 74,000 $31,000 74,000 94,000 104,000 51,000 40,000 31,000 Required: a. What net income...

Ravine Corporation purchased 40 percent ownership of Valley Industries for $116,400 on January 1, 20X6, when Valley had capital stock of $246,000 and retained earnings of $45,000. The following data were reported by the companies for the years 20X6 through 20X9: Dividends Declared Operating Income, Net Income, Valley Year Ravine Corporation Valley Industries Ravine 20X6 20X7 20X8 20X9 $149,000 94,000 224,000 169,000 $41,000 61,000 10,000 51,000 $ 74,000 $31,000 74,000 94,000 104,000 51,000 40,000 31,000 Required: a. What net income...

Pistol Corporation purchased 100 percent ownership of Scope Products on January 1, 20X6, for $60,000, at...

Pistol Corporation purchased 100 percent ownership of Scope Products on January 1, 20X6, for $60,000, at which time Scope Products reported retained earnings of $12,000 and capital stock outstanding of $29,000. The differential was attributable to patents with a life of four years. Income and dividends of Scope Products were Year 20x6 20x7 20X8 Net Income $23,000 31,000 39,000 Dividends $ 8,000 10,000 10,000 Required: 1. Prepare the equity method entries that Pistol should record to account for this investment...

Pistol Corporation purchased 100 percent ownership of Scope Products on January 1, 20X6, for $60,000, at which time Scope Products reported retained earnings of $12,000 and capital stock outstanding of $29,000. The differential was attributable to patents with a life of four years. Income and dividends of Scope Products were Year 20x6 20x7 20X8 Net Income $23,000 31,000 39,000 Dividends $ 8,000 10,000 10,000 Required: 1. Prepare the equity method entries that Pistol should record to account for this investment...

Callas Corporation paid $380,000 to acquire 40 percent ownership of Thinbill Company on January 1, 20X9....

Callas Corporation paid $380,000 to acquire 40 percent ownership

of Thinbill Company on January 1, 20X9. The amount paid was equal

to Thinbill’s underlying book value. During 20X9, Thinbill reported

operating income of $45,000 and income of $20,000 from gains on

derivative contracts that were designated as cash flow hedges, so

these gains were reported in Other Comprehensive Income (OCI).

Thinbill paid dividends of $9,000 on December 10, 20X9.

Required:

a. Give all journal entries that Callas Corporation recorded in...

Callas Corporation paid $380,000 to acquire 40 percent ownership

of Thinbill Company on January 1, 20X9. The amount paid was equal

to Thinbill’s underlying book value. During 20X9, Thinbill reported

operating income of $45,000 and income of $20,000 from gains on

derivative contracts that were designated as cash flow hedges, so

these gains were reported in Other Comprehensive Income (OCI).

Thinbill paid dividends of $9,000 on December 10, 20X9.

Required:

a. Give all journal entries that Callas Corporation recorded in...

Pistol Corporation purchased 100 percent ownership of Scope Products on January 1, 20X6, for $60,000, at...

Pistol Corporation purchased 100 percent ownership of Scope Products on January 1, 20X6, for $60,000, at which time Scope Products reported retained earnings of $13,000 and capital stock outstanding of $26,000. The differential was attributable to patents with a life of four years. Income and dividends of Scope Products were Year Net Income Dividends 20X6 $ 17,000 $ 7,000 20X7 25,000 9,000 20X8 33,000 9,000 Required: 1. Prepare the equity method entries that Pistol should record to account for this...

Purse Corporation owns 70 percent of Scarf Company’s voting

shares. On January 1, 20X3, Scarf sold bonds with a par value of

$675,000 at 98. Purse purchased $450,000 par value of the bonds;

the remainder was sold to nonaffiliates. The bonds mature in five

years and pay an annual interest rate of 8 percent. Interest is

paid semiannually on January 1 and July 1.

Required:

a. What amount of interest expense should be reported in the 20X4

consolidated income statement?...

Purse Corporation owns 70 percent of Scarf Company’s voting

shares. On January 1, 20X3, Scarf sold bonds with a par value of

$675,000 at 98. Purse purchased $450,000 par value of the bonds;

the remainder was sold to nonaffiliates. The bonds mature in five

years and pay an annual interest rate of 8 percent. Interest is

paid semiannually on January 1 and July 1.

Required:

a. What amount of interest expense should be reported in the 20X4

consolidated income statement?...

Price Corporation acquired 100 percent ownership of Saver Company on January 1, 20x8, for $158,000. At that date, the fair value of Saver's buildings and equipment was $32,000 more than the book value. Buildings and equipment are depreciated on a 10-year basis. Although goodwill is not amortized, Price's management concluded at December 31, 20x8, that goodwill involved in its acquisition of Saver shares had been impaired and the correct carrying value was $5,500. Trial balance data for Price and Saver...

Price Corporation acquired 100 percent ownership of Saver Company on January 1, 20x8, for $158,000. At that date, the fair value of Saver's buildings and equipment was $32,000 more than the book value. Buildings and equipment are depreciated on a 10-year basis. Although goodwill is not amortized, Price's management concluded at December 31, 20x8, that goodwill involved in its acquisition of Saver shares had been impaired and the correct carrying value was $5,500. Trial balance data for Price and Saver...

Ravine Corporation purchased 40 percent ownership of Valley Industries for $116,400 on January 1, 20X6, when Valley had capital stock of $246,000 and retained earnings of $45,000. The following data were reported by the companies for the years 20X6 through 20X9: Dividends Declared Operating Income, Net Income, Valley Year Ravine Corporation Valley Industries Ravine 20X6 20X7 20X8 20X9 $149,000 94,000 224,000 169,000 $41,000 61,000 10,000 51,000 $ 74,000 $31,000 74,000 94,000 104,000 51,000 40,000 31,000 Required: a. What net income...

Ravine Corporation purchased 40 percent ownership of Valley Industries for $116,400 on January 1, 20X6, when Valley had capital stock of $246,000 and retained earnings of $45,000. The following data were reported by the companies for the years 20X6 through 20X9: Dividends Declared Operating Income, Net Income, Valley Year Ravine Corporation Valley Industries Ravine 20X6 20X7 20X8 20X9 $149,000 94,000 224,000 169,000 $41,000 61,000 10,000 51,000 $ 74,000 $31,000 74,000 94,000 104,000 51,000 40,000 31,000 Required: a. What net income...

Pistol Corporation purchased 100 percent ownership of Scope Products on January 1, 20X6, for $60,000, at which time Scope Products reported retained earnings of $12,000 and capital stock outstanding of $29,000. The differential was attributable to patents with a life of four years. Income and dividends of Scope Products were Year 20x6 20x7 20X8 Net Income $23,000 31,000 39,000 Dividends $ 8,000 10,000 10,000 Required: 1. Prepare the equity method entries that Pistol should record to account for this investment...

Pistol Corporation purchased 100 percent ownership of Scope Products on January 1, 20X6, for $60,000, at which time Scope Products reported retained earnings of $12,000 and capital stock outstanding of $29,000. The differential was attributable to patents with a life of four years. Income and dividends of Scope Products were Year 20x6 20x7 20X8 Net Income $23,000 31,000 39,000 Dividends $ 8,000 10,000 10,000 Required: 1. Prepare the equity method entries that Pistol should record to account for this investment...

Callas Corporation paid $380,000 to acquire 40 percent ownership

of Thinbill Company on January 1, 20X9. The amount paid was equal

to Thinbill’s underlying book value. During 20X9, Thinbill reported

operating income of $45,000 and income of $20,000 from gains on

derivative contracts that were designated as cash flow hedges, so

these gains were reported in Other Comprehensive Income (OCI).

Thinbill paid dividends of $9,000 on December 10, 20X9.

Required:

a. Give all journal entries that Callas Corporation recorded in...

Callas Corporation paid $380,000 to acquire 40 percent ownership

of Thinbill Company on January 1, 20X9. The amount paid was equal

to Thinbill’s underlying book value. During 20X9, Thinbill reported

operating income of $45,000 and income of $20,000 from gains on

derivative contracts that were designated as cash flow hedges, so

these gains were reported in Other Comprehensive Income (OCI).

Thinbill paid dividends of $9,000 on December 10, 20X9.

Required:

a. Give all journal entries that Callas Corporation recorded in...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago