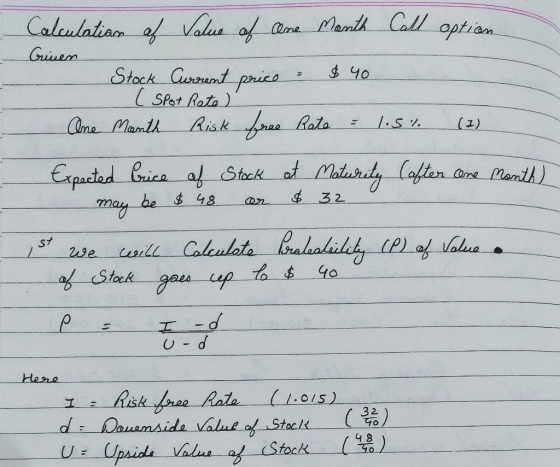

The stock of Kingbird is currently trading for $40 and will either rise to $48 or...

The stock of Kingbird is currently trading for $40 and will

either rise to $48 or fall to $32 in one month. The risk-free rate

for one month is 1.5 percent. What is the value of a one-month call

option with a strike price of $40? (Round intermediate

calculations to 4 decimal places, e.g. 1.2514 and final answer to 2

decimal places, e.g. 15.25.)

| Value of a call option is $enter the dollar value of the call option rounded to 2 decimal places . |

Homework Answers

Add Answer to:

The stock of Kingbird is currently trading for $40 and will

either rise to $48 or...

The stock of Splish Brothers is currently trading for $40 and will either rise to $48...

The stock of Splish Brothers is currently trading for $40 and will either rise to $48 or fall to $36 in one month. The risk-free rate for one month is 1.5 percent. What is the value of a one-month call option with a strike price of $40? (Round intermediate calculations to 4 decimal places, e.g. 1.2514 and final answer to 2 decimal places, e.g. 15.25.) Value of a call option is $

Dynamic Energy Systems stock is currently trading for $29 per share. The stock pays no dividends....

Dynamic Energy Systems stock is currently trading for $29 per share. The stock pays no dividends. A one-year European put option on Dynamic with a strike price of $32 is currently trading for $3.69. If the risk-free interest rate is 3% per year, what is the price of a one-year European call option on Dynamic with a strike price of $32? (Rounded to the nearest cent.)

Dynamic Energy Systems stock is currently trading for $29 per share. The stock pays no dividends. A one-year European put option on Dynamic with a strike price of $32 is currently trading for $3.69. If the risk-free interest rate is 3% per year, what is the price of a one-year European call option on Dynamic with a strike price of $32? (Rounded to the nearest cent.)

RST, Inc. stock is currently trading for $33 per share. The stock pays no dividends. A...

RST, Inc. stock is currently trading for $33 per share. The stock pays no dividends. A one-year European call option on RST with a strike price of $36 is currently trading for $2.99. If the risk-free interest rate is 6% per year, what is the price of a one-year European put option on RST with a strike price of $36? (Rounded to the nearest cent.)

RST, Inc. stock is currently trading for $33 per share. The stock pays no dividends. A one-year European call option on RST with a strike price of $36 is currently trading for $2.99. If the risk-free interest rate is 6% per year, what is the price of a one-year European put option on RST with a strike price of $36? (Rounded to the nearest cent.)

Koka Kola common stock is currently trading for $29 per share. A put option on the...

Koka Kola common stock is currently trading for $29 per share. A put option on the stock with a strike price of $32 that expires in 334 days is selling for $3.76. A call option on the stock with a strike price of $32 that expires in 334 days is currently trading for $1.99. What is the exercise value of the put option? (Rounded to the nearest cent.) $ What is the put option's time premium? (Rounded to the nearest...

Koka Kola common stock is currently trading for $29 per share. A put option on the stock with a strike price of $32 that expires in 334 days is selling for $3.76. A call option on the stock with a strike price of $32 that expires in 334 days is currently trading for $1.99. What is the exercise value of the put option? (Rounded to the nearest cent.) $ What is the put option's time premium? (Rounded to the nearest...

A stock price is currently $40. It is known that at the end of 1 month...

A stock price is currently $40. It is known that at the end of 1 month it will be either $42 or $38. The risk-free interest rate is 8% per annum with continuous compounding. What is the value of a 1-month European call option with a strike price of $39?

imagine that googles stock price will either rise by one third or fall by 25% over...

imagine that googles stock price will either rise by one third or fall by 25% over the next six months. Assume the 6 month risk free interest rate is 1%. Both the stock price amd the excersie price are $530. 1. Calculate the value of the 6 month call option using the replicating porfolio method 2. Calculate the value of the 6 month call option using the risk neutral method.

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

A stock currently sells for $50. In six months it will either rise to $60 or...

A stock currently sells for $50. In six months it will either rise to $60 or decline to $45. The continuous compounding risk-free interest rate is 5% per year. Using the binomial approach, find the value of a European call option with an exercise price of $50. Using the binomial approach, find the value of a European put option with an exercise price of $50. Verify the put-call parity using the results of Questions 1 and 2.

A stock is currently priced at $68 and has an annual standard deviation of 48 percent....

A stock is currently priced at $68 and has an annual standard deviation of 48 percent. The dividend yield of the stock is 3.5 percent, and the risk-free rate is 6.5 percent. What is the value of a call option on the stock with a strike price of $65 and 55 days to expiration? (Round your answer to 2 decimal places. Omit the "$" sign in your response.)

Suppose IBM's stock price is currently $100. In the next year it will either fall to...

Suppose IBM's stock price is currently $100. In the next year it will either fall to $70 or rise to $130. What is the price today of a one-year European call option on IBM with an exercise price of 100? The one-year risk-free interest rate is 2% per year. 6 10 0 15.69

Suppose IBM's stock price is currently $100. In the next year it will either fall to $70 or rise to $130. What is the price today of a one-year European call option on IBM with an exercise price of 100? The one-year risk-free interest rate is 2% per year. 6 10 0 15.69

Dynamic Energy Systems stock is currently trading for $29 per share. The stock pays no dividends. A one-year European put option on Dynamic with a strike price of $32 is currently trading for $3.69. If the risk-free interest rate is 3% per year, what is the price of a one-year European call option on Dynamic with a strike price of $32? (Rounded to the nearest cent.)

Dynamic Energy Systems stock is currently trading for $29 per share. The stock pays no dividends. A one-year European put option on Dynamic with a strike price of $32 is currently trading for $3.69. If the risk-free interest rate is 3% per year, what is the price of a one-year European call option on Dynamic with a strike price of $32? (Rounded to the nearest cent.)

RST, Inc. stock is currently trading for $33 per share. The stock pays no dividends. A one-year European call option on RST with a strike price of $36 is currently trading for $2.99. If the risk-free interest rate is 6% per year, what is the price of a one-year European put option on RST with a strike price of $36? (Rounded to the nearest cent.)

RST, Inc. stock is currently trading for $33 per share. The stock pays no dividends. A one-year European call option on RST with a strike price of $36 is currently trading for $2.99. If the risk-free interest rate is 6% per year, what is the price of a one-year European put option on RST with a strike price of $36? (Rounded to the nearest cent.)

Koka Kola common stock is currently trading for $29 per share. A put option on the stock with a strike price of $32 that expires in 334 days is selling for $3.76. A call option on the stock with a strike price of $32 that expires in 334 days is currently trading for $1.99. What is the exercise value of the put option? (Rounded to the nearest cent.) $ What is the put option's time premium? (Rounded to the nearest...

Koka Kola common stock is currently trading for $29 per share. A put option on the stock with a strike price of $32 that expires in 334 days is selling for $3.76. A call option on the stock with a strike price of $32 that expires in 334 days is currently trading for $1.99. What is the exercise value of the put option? (Rounded to the nearest cent.) $ What is the put option's time premium? (Rounded to the nearest...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

Suppose IBM's stock price is currently $100. In the next year it will either fall to $70 or rise to $130. What is the price today of a one-year European call option on IBM with an exercise price of 100? The one-year risk-free interest rate is 2% per year. 6 10 0 15.69

Suppose IBM's stock price is currently $100. In the next year it will either fall to $70 or rise to $130. What is the price today of a one-year European call option on IBM with an exercise price of 100? The one-year risk-free interest rate is 2% per year. 6 10 0 15.69

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago