Homework Answers

| Q 1) NOT CLEAR WITH MATTERS AND REQUIREMENTS | |||

| Q 16) | |||

| Answer: | d) Unrealised Holding Gain or Loss- equity (loss) | 10000 | |

| Fair Value Adjustment (available for sale) | 10000 | ||

| because present adjustment is for 10000, as | |||

| (Cost 80000 -4000 already done - present value 66000) | |||

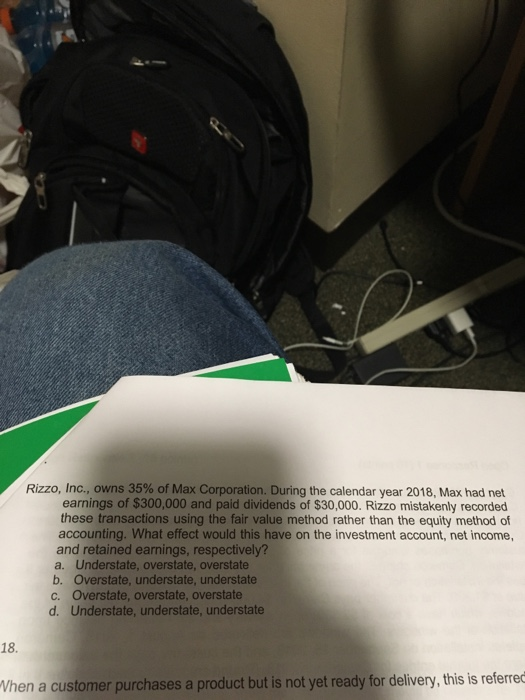

| Question Last: Answer : a. Understate, overstate, overstate | |||

| Because Max share in net earnings is not added to investment, | |||

| dividend is taken as revenue income instead of capital income, | |||

| retained earnings goes up as net income overstated. | |||

Add Answer to:

The

first and second photo are all part of one question.

c. 9,100,000 d. 5,800,000 Pernt...

At December 31, 2018, Atlanta Company has an equity portfolio valued at $160,000. Its cost was...

At December 31, 2018, Atlanta Company has an equity portfolio valued at $160,000. Its cost was $132,000. If the Securities Fair Value Adjustment has a debit balance of $8,000, which of the following journal entries is required at December 31, 2018? Select one: a. Fair Value Adjustment 28,000 Unrealized Holding Gain or Loss-Income 28,000 b. Unrealized Holding Gain or Loss-Income 20,000 Fair Value Adjustment 20,000 c. Unrealized Holding Gain or Loss-Income 28,000 Fair Value Adjustment 28,000 d. Fair Value Adjustment...

Carpark Services began operations in 20X1 and maintains long-term investments in available-for-sale securities. The year-end cost...

Carpark Services began operations in 20X1 and maintains long-term investments in available-for-sale securities. The year-end cost and fair values for its portfolio of these investments follow. The year end adjusting entry to record the unrealized gain/loss at December 31, 20X1 is: Available-for-Sale Securities December 31, 20x1 December 31, 20x2 December 31, 20X3 Cost $295,000 $376,000 $446,000 Fair Value $277,000 $396,000 $495,000 Multiple Choice O Debit Unrealized Gain-Equity $18,000: Credit Fair Value Adjustment - Available-for-Sale (LT) $18,000. 0 O Debit Unrealized...

Carpark Services began operations in 20X1 and maintains long-term investments in available-for-sale securities. The year-end cost and fair values for its portfolio of these investments follow. The year end adjusting entry to record the unrealized gain/loss at December 31, 20X1 is: Available-for-Sale Securities December 31, 20x1 December 31, 20x2 December 31, 20X3 Cost $295,000 $376,000 $446,000 Fair Value $277,000 $396,000 $495,000 Multiple Choice O Debit Unrealized Gain-Equity $18,000: Credit Fair Value Adjustment - Available-for-Sale (LT) $18,000. 0 O Debit Unrealized...

- 15-17 0 Saved Help Save & Exit Submit Carpark Services began operations in 20%1 and...

- 15-17 0 Saved Help Save & Exit Submit Carpark Services began operations in 20%1 and maintains long-term investments in available for sale debt securities. The year-end cost and fair values for its portfolio of debt securities follows. The year end adjusting entry to record the unrealized gain/loss at December 31, 20X2 is: Available-for-Sale Securities Cost Fair Value December 31, 20x1 $295,000 $277,000 December 31, 20x2 $376,000 $396,000 Multiple Choice Debit Fair Value Adjustment - Available for Sale (LT) $20,000...

- 15-17 0 Saved Help Save & Exit Submit Carpark Services began operations in 20%1 and maintains long-term investments in available for sale debt securities. The year-end cost and fair values for its portfolio of debt securities follows. The year end adjusting entry to record the unrealized gain/loss at December 31, 20X2 is: Available-for-Sale Securities Cost Fair Value December 31, 20x1 $295,000 $277,000 December 31, 20x2 $376,000 $396,000 Multiple Choice Debit Fair Value Adjustment - Available for Sale (LT) $20,000...

At December 31, 2021, Jeter Corporation had the following debt securities that were purchased during 2021,...

At December 31, 2021, Jeter Corporation had the following debt securities that were purchased during 2021, its first year of operation: Fair Unrealized Cost Value Gain (Loss) Trading Securities: Security A $ 85,000 $ 65,000 $(20,000) 15,000 20,000 5,000 Totals $100,000 $ 85,000 $(15,000) Available-for-Sale Securities: Security Y $ 70.000 $ 80,000 $ 10,000 Z 85,000 55,000 (30,000) Totals $ 155,000 $135.000 $(20,000) All market declines are considered temporary. Fair value adjustments at December 31, 2021 should be established with...

At December 31, 2021, Jeter Corporation had the following debt securities that were purchased during 2021, its first year of operation: Fair Unrealized Cost Value Gain (Loss) Trading Securities: Security A $ 85,000 $ 65,000 $(20,000) 15,000 20,000 5,000 Totals $100,000 $ 85,000 $(15,000) Available-for-Sale Securities: Security Y $ 70.000 $ 80,000 $ 10,000 Z 85,000 55,000 (30,000) Totals $ 155,000 $135.000 $(20,000) All market declines are considered temporary. Fair value adjustments at December 31, 2021 should be established with...

Saved Help Save Carpark Services began operations in 20X1 and maintains long-term investments in available-for-sale debt...

Saved Help Save Carpark Services began operations in 20X1 and maintains long-term investments in available-for-sale debt securities. The year end cost and fair values for its portfolio of these debt securities follows. The year-end adjusting entry to record the unrealized gain/loss at December 31, 20X1is: Available-for-Sale Securities Cost Fair Value December 31, 20x1 $300,000 $281,000 December 31, 20x2 $380,000 $401,500 Multiple Choice Debit Unrealized Gain-Equity $19000 Credit Fair Value Adjustment - Available for Sale (LT) $19.000 Debit Unrealized Loss -...

Saved Help Save Carpark Services began operations in 20X1 and maintains long-term investments in available-for-sale debt securities. The year end cost and fair values for its portfolio of these debt securities follows. The year-end adjusting entry to record the unrealized gain/loss at December 31, 20X1is: Available-for-Sale Securities Cost Fair Value December 31, 20x1 $300,000 $281,000 December 31, 20x2 $380,000 $401,500 Multiple Choice Debit Unrealized Gain-Equity $19000 Credit Fair Value Adjustment - Available for Sale (LT) $19.000 Debit Unrealized Loss -...

On its December 31, 2017 balance sheet, Calhoun Company appropriately reported a $10,000 credit balance in...

On its December 31, 2017 balance sheet, Calhoun Company appropriately reported a $10,000 credit balance in its Fair Value Adjustment (available-for-sale) account. There was no change during 2018 in the composition of Calhoun’s portfolio of debt investments held as available-for-sale securities. The following information pertains to that portfolio: Security Cost Fair value at 12/31/18 X $125,000 $160,000 Y 100,000 85,000 Z 175,000 125,000 $400,000 $370,000 The amount of unrealized loss to appear as a component of comprehensive income for the year ending December...

Most of my answers are wrong Ticker Services began operations in Year 1 and holds long-term...

Most of my answers are wrong

Ticker Services began operations in Year 1 and holds long-term investments in available-for-sale debt securities. The year-end cost and fair values for its portfolio of these investments follow. Portfolio of Available-for-Sale Securities December 31, Year 1 December 31, Year 2 December 31, Year 3 December 31, Year 4 Cost $ 12,200 18,100 20,600 14,800 Fair Value $ 18,900 27,800 32,700 21,800 Prepare journal entries to record each year-end fair value adjustment for these securities....

Most of my answers are wrong

Ticker Services began operations in Year 1 and holds long-term investments in available-for-sale debt securities. The year-end cost and fair values for its portfolio of these investments follow. Portfolio of Available-for-Sale Securities December 31, Year 1 December 31, Year 2 December 31, Year 3 December 31, Year 4 Cost $ 12,200 18,100 20,600 14,800 Fair Value $ 18,900 27,800 32,700 21,800 Prepare journal entries to record each year-end fair value adjustment for these securities....

Situation 1: Goebel Company acquired a 20% interest in Dobbs Company on December 31, 2018 for...

Situation 1: Goebel Company acquired a 20% interest in Dobbs Company on December 31, 2018 for $350,000. During 2019 Dobbs Company had net income of $150,000 and paid a cash dividend of $60,000. (Dobbs Company paid $60,000 cash dividend to all of its shareholders.) 12. Based on the information regarding Goebel's investment in Dobbs Company: Fair Value 12/31/18 12/31/19 $350,000 $365,000 Cost $350,000 Equity investment If the Fair Value Adjustment has a debit balance of $8,000, what amount of unrealized...

Situation 1: Goebel Company acquired a 20% interest in Dobbs Company on December 31, 2018 for $350,000. During 2019 Dobbs Company had net income of $150,000 and paid a cash dividend of $60,000. (Dobbs Company paid $60,000 cash dividend to all of its shareholders.) 12. Based on the information regarding Goebel's investment in Dobbs Company: Fair Value 12/31/18 12/31/19 $350,000 $365,000 Cost $350,000 Equity investment If the Fair Value Adjustment has a debit balance of $8,000, what amount of unrealized...

On December 31, 2018, Marsh Company held Xenon Company bonds in its portfolio of available-for-sale securities....

On December 31, 2018, Marsh Company held Xenon Company bonds in

its portfolio of available-for-sale securities. The bonds have a

par value of $14,000, carry a 10% annual interest rate, mature in

2025, and had originally been purchased at par. The market value of

the bonds at December 31, 2018 was $12,000. The December 31, 2018,

balance sheet showed the following:

Marsh Company

Partial Balance Sheet

December 31, 2018

1

Assets

2

Investment in Available-for-Sale Securities

$14,000.00

3

Less: Allowance...

On December 31, 2018, Marsh Company held Xenon Company bonds in

its portfolio of available-for-sale securities. The bonds have a

par value of $14,000, carry a 10% annual interest rate, mature in

2025, and had originally been purchased at par. The market value of

the bonds at December 31, 2018 was $12,000. The December 31, 2018,

balance sheet showed the following:

Marsh Company

Partial Balance Sheet

December 31, 2018

1

Assets

2

Investment in Available-for-Sale Securities

$14,000.00

3

Less: Allowance...

exercise 16-06 in its first year of operations Sheridan corporation purchased as a long term investment...

exercise 16-06

in its first year of operations Sheridan corporation purchased as a

long term investment available for sale debt securities costing

$68,500. December 21,2020 the fair value of the securities is $

63,650

We were unable to transcribe this imageList of Accounts CLOSE Brief Exercise 16-06 Debt Investments Dividend Revenue Fair Value Adjustment-Available-for-Sale Fair Value Adjustment-Stock Fair Value Adjustment-Trading Gain on Sale of Debt Investments Gain on Sale of Stock Investments Interest Receivable Interest Revenue Loss on Sale of...

exercise 16-06

in its first year of operations Sheridan corporation purchased as a

long term investment available for sale debt securities costing

$68,500. December 21,2020 the fair value of the securities is $

63,650

We were unable to transcribe this imageList of Accounts CLOSE Brief Exercise 16-06 Debt Investments Dividend Revenue Fair Value Adjustment-Available-for-Sale Fair Value Adjustment-Stock Fair Value Adjustment-Trading Gain on Sale of Debt Investments Gain on Sale of Stock Investments Interest Receivable Interest Revenue Loss on Sale of...

Carpark Services began operations in 20X1 and maintains long-term investments in available-for-sale securities. The year-end cost and fair values for its portfolio of these investments follow. The year end adjusting entry to record the unrealized gain/loss at December 31, 20X1 is: Available-for-Sale Securities December 31, 20x1 December 31, 20x2 December 31, 20X3 Cost $295,000 $376,000 $446,000 Fair Value $277,000 $396,000 $495,000 Multiple Choice O Debit Unrealized Gain-Equity $18,000: Credit Fair Value Adjustment - Available-for-Sale (LT) $18,000. 0 O Debit Unrealized...

Carpark Services began operations in 20X1 and maintains long-term investments in available-for-sale securities. The year-end cost and fair values for its portfolio of these investments follow. The year end adjusting entry to record the unrealized gain/loss at December 31, 20X1 is: Available-for-Sale Securities December 31, 20x1 December 31, 20x2 December 31, 20X3 Cost $295,000 $376,000 $446,000 Fair Value $277,000 $396,000 $495,000 Multiple Choice O Debit Unrealized Gain-Equity $18,000: Credit Fair Value Adjustment - Available-for-Sale (LT) $18,000. 0 O Debit Unrealized...

- 15-17 0 Saved Help Save & Exit Submit Carpark Services began operations in 20%1 and maintains long-term investments in available for sale debt securities. The year-end cost and fair values for its portfolio of debt securities follows. The year end adjusting entry to record the unrealized gain/loss at December 31, 20X2 is: Available-for-Sale Securities Cost Fair Value December 31, 20x1 $295,000 $277,000 December 31, 20x2 $376,000 $396,000 Multiple Choice Debit Fair Value Adjustment - Available for Sale (LT) $20,000...

- 15-17 0 Saved Help Save & Exit Submit Carpark Services began operations in 20%1 and maintains long-term investments in available for sale debt securities. The year-end cost and fair values for its portfolio of debt securities follows. The year end adjusting entry to record the unrealized gain/loss at December 31, 20X2 is: Available-for-Sale Securities Cost Fair Value December 31, 20x1 $295,000 $277,000 December 31, 20x2 $376,000 $396,000 Multiple Choice Debit Fair Value Adjustment - Available for Sale (LT) $20,000...

At December 31, 2021, Jeter Corporation had the following debt securities that were purchased during 2021, its first year of operation: Fair Unrealized Cost Value Gain (Loss) Trading Securities: Security A $ 85,000 $ 65,000 $(20,000) 15,000 20,000 5,000 Totals $100,000 $ 85,000 $(15,000) Available-for-Sale Securities: Security Y $ 70.000 $ 80,000 $ 10,000 Z 85,000 55,000 (30,000) Totals $ 155,000 $135.000 $(20,000) All market declines are considered temporary. Fair value adjustments at December 31, 2021 should be established with...

At December 31, 2021, Jeter Corporation had the following debt securities that were purchased during 2021, its first year of operation: Fair Unrealized Cost Value Gain (Loss) Trading Securities: Security A $ 85,000 $ 65,000 $(20,000) 15,000 20,000 5,000 Totals $100,000 $ 85,000 $(15,000) Available-for-Sale Securities: Security Y $ 70.000 $ 80,000 $ 10,000 Z 85,000 55,000 (30,000) Totals $ 155,000 $135.000 $(20,000) All market declines are considered temporary. Fair value adjustments at December 31, 2021 should be established with...

Saved Help Save Carpark Services began operations in 20X1 and maintains long-term investments in available-for-sale debt securities. The year end cost and fair values for its portfolio of these debt securities follows. The year-end adjusting entry to record the unrealized gain/loss at December 31, 20X1is: Available-for-Sale Securities Cost Fair Value December 31, 20x1 $300,000 $281,000 December 31, 20x2 $380,000 $401,500 Multiple Choice Debit Unrealized Gain-Equity $19000 Credit Fair Value Adjustment - Available for Sale (LT) $19.000 Debit Unrealized Loss -...

Saved Help Save Carpark Services began operations in 20X1 and maintains long-term investments in available-for-sale debt securities. The year end cost and fair values for its portfolio of these debt securities follows. The year-end adjusting entry to record the unrealized gain/loss at December 31, 20X1is: Available-for-Sale Securities Cost Fair Value December 31, 20x1 $300,000 $281,000 December 31, 20x2 $380,000 $401,500 Multiple Choice Debit Unrealized Gain-Equity $19000 Credit Fair Value Adjustment - Available for Sale (LT) $19.000 Debit Unrealized Loss -...

Most of my answers are wrong

Ticker Services began operations in Year 1 and holds long-term investments in available-for-sale debt securities. The year-end cost and fair values for its portfolio of these investments follow. Portfolio of Available-for-Sale Securities December 31, Year 1 December 31, Year 2 December 31, Year 3 December 31, Year 4 Cost $ 12,200 18,100 20,600 14,800 Fair Value $ 18,900 27,800 32,700 21,800 Prepare journal entries to record each year-end fair value adjustment for these securities....

Most of my answers are wrong

Ticker Services began operations in Year 1 and holds long-term investments in available-for-sale debt securities. The year-end cost and fair values for its portfolio of these investments follow. Portfolio of Available-for-Sale Securities December 31, Year 1 December 31, Year 2 December 31, Year 3 December 31, Year 4 Cost $ 12,200 18,100 20,600 14,800 Fair Value $ 18,900 27,800 32,700 21,800 Prepare journal entries to record each year-end fair value adjustment for these securities....

Situation 1: Goebel Company acquired a 20% interest in Dobbs Company on December 31, 2018 for $350,000. During 2019 Dobbs Company had net income of $150,000 and paid a cash dividend of $60,000. (Dobbs Company paid $60,000 cash dividend to all of its shareholders.) 12. Based on the information regarding Goebel's investment in Dobbs Company: Fair Value 12/31/18 12/31/19 $350,000 $365,000 Cost $350,000 Equity investment If the Fair Value Adjustment has a debit balance of $8,000, what amount of unrealized...

Situation 1: Goebel Company acquired a 20% interest in Dobbs Company on December 31, 2018 for $350,000. During 2019 Dobbs Company had net income of $150,000 and paid a cash dividend of $60,000. (Dobbs Company paid $60,000 cash dividend to all of its shareholders.) 12. Based on the information regarding Goebel's investment in Dobbs Company: Fair Value 12/31/18 12/31/19 $350,000 $365,000 Cost $350,000 Equity investment If the Fair Value Adjustment has a debit balance of $8,000, what amount of unrealized...

On December 31, 2018, Marsh Company held Xenon Company bonds in

its portfolio of available-for-sale securities. The bonds have a

par value of $14,000, carry a 10% annual interest rate, mature in

2025, and had originally been purchased at par. The market value of

the bonds at December 31, 2018 was $12,000. The December 31, 2018,

balance sheet showed the following:

Marsh Company

Partial Balance Sheet

December 31, 2018

1

Assets

2

Investment in Available-for-Sale Securities

$14,000.00

3

Less: Allowance...

On December 31, 2018, Marsh Company held Xenon Company bonds in

its portfolio of available-for-sale securities. The bonds have a

par value of $14,000, carry a 10% annual interest rate, mature in

2025, and had originally been purchased at par. The market value of

the bonds at December 31, 2018 was $12,000. The December 31, 2018,

balance sheet showed the following:

Marsh Company

Partial Balance Sheet

December 31, 2018

1

Assets

2

Investment in Available-for-Sale Securities

$14,000.00

3

Less: Allowance...

exercise 16-06

in its first year of operations Sheridan corporation purchased as a

long term investment available for sale debt securities costing

$68,500. December 21,2020 the fair value of the securities is $

63,650

We were unable to transcribe this imageList of Accounts CLOSE Brief Exercise 16-06 Debt Investments Dividend Revenue Fair Value Adjustment-Available-for-Sale Fair Value Adjustment-Stock Fair Value Adjustment-Trading Gain on Sale of Debt Investments Gain on Sale of Stock Investments Interest Receivable Interest Revenue Loss on Sale of...

exercise 16-06

in its first year of operations Sheridan corporation purchased as a

long term investment available for sale debt securities costing

$68,500. December 21,2020 the fair value of the securities is $

63,650

We were unable to transcribe this imageList of Accounts CLOSE Brief Exercise 16-06 Debt Investments Dividend Revenue Fair Value Adjustment-Available-for-Sale Fair Value Adjustment-Stock Fair Value Adjustment-Trading Gain on Sale of Debt Investments Gain on Sale of Stock Investments Interest Receivable Interest Revenue Loss on Sale of...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago