Homework Answers

Add Answer to:

Assume that security returns are generated by the single-index model, Ri-ai + BiR + where R...

Assume that security returns are generated by the single-index model, Ri - Qi + BiRM +...

Assume that security returns are generated by the single-index model, Ri - Qi + BiRM + ei where R is the excess return for security i and Ry is the market's excess return. The risk-free rate is 2%. Suppose also that there are three securities A, B, and C, characterized by the following data: Security Bi A 0. 6 B 0.9 C 1.2 E(Ri) (ei) 7 % 16% 107 13 10 a. If Om = 10%, calculate the variance of...

Assume that security returns are generated by the single-index model, Ri - Qi + BiRM + ei where R is the excess return for security i and Ry is the market's excess return. The risk-free rate is 2%. Suppose also that there are three securities A, B, and C, characterized by the following data: Security Bi A 0. 6 B 0.9 C 1.2 E(Ri) (ei) 7 % 16% 107 13 10 a. If Om = 10%, calculate the variance of...

7. Assume that security returns are generated by the single-index model, Ri = αi + βiRM...

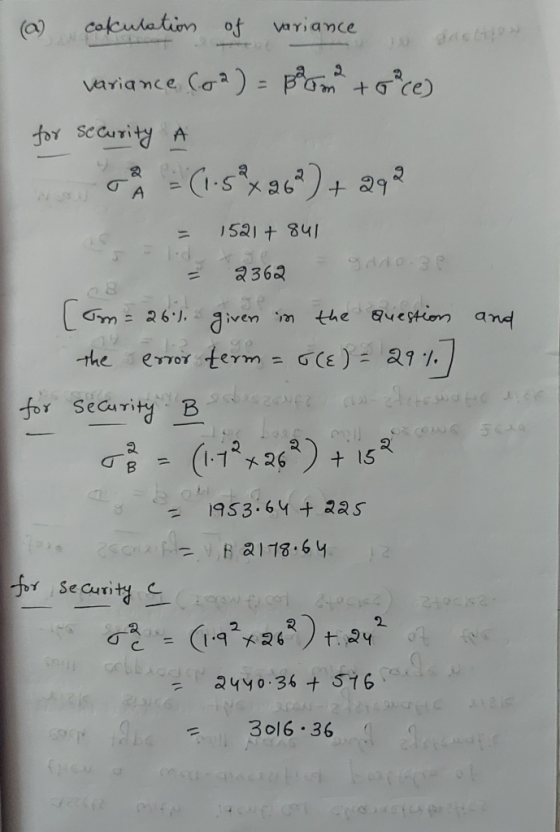

7. Assume that security returns are generated by the single-index model, Ri = αi + βiRM + ei where Ri is the excess return for security i and RM is the market’s excess return. The risk-free rate is 3%. Suppose also that there are three securities A, B, and C, characterized by the following data: Security βi E(Ri) σ(ei) A 0.9 8% 17% B 1.3 12 8 C 1.7 16 11 a. If σM = 12%, calculate the...

10. Assume that security returns are generated by the single-index model, Ri = αi + βiRM...

10. Assume that security returns are generated by the single-index model, Ri = αi + βiRM + ei where Ri is the excess return for security i and RM is the market’s excess return. The risk-free rate is 2%. Suppose also that there are three securities A, B, and C, characterized by the following data: Security βi E(Ri) σ(ei) A 0.8 10% 25% B 1.0 12 10 C 1.2 14 20 a. If σM = 20%,...

Assume that security returns are generated by the single index R; - a1 + RM +...

Assume that security returns are generated by the single index R; - a1 + RM + ei return where R is the excess return for security / and Ry is the three securities A, B, and C, characterized by the following data The risk-free rate is 4%. Suppose also that there are Security Bi E(R) olej) A 0.8 15 24% B 1.1 18 15 C 1.4 21 18 a. If om = 20%, calculate the variance ces Variance Security A...

Assume that security returns are generated by the single index R; - a1 + RM + ei return where R is the excess return for security / and Ry is the three securities A, B, and C, characterized by the following data The risk-free rate is 4%. Suppose also that there are Security Bi E(R) olej) A 0.8 15 24% B 1.1 18 15 C 1.4 21 18 a. If om = 20%, calculate the variance ces Variance Security A...

Assume security returns are generated by the single-index model. R 1 =a 1 + beta 2...

Assume security returns are generated by the single-index

model. R 1 =a 1 + beta 2 R M +e 1 where R 1 is the excess return

for security and R N market’s excess returnThe risk-free rate is 4%

Suppose also that there are three securities A8and characterized by

the following data!

Saved Assume that security returns are generated by the single-index model R; - ei + BiRM + ej where is the excess return for security i and Ry...

Assume security returns are generated by the single-index

model. R 1 =a 1 + beta 2 R M +e 1 where R 1 is the excess return

for security and R N market’s excess returnThe risk-free rate is 4%

Suppose also that there are three securities A8and characterized by

the following data!

Saved Assume that security returns are generated by the single-index model R; - ei + BiRM + ej where is the excess return for security i and Ry...

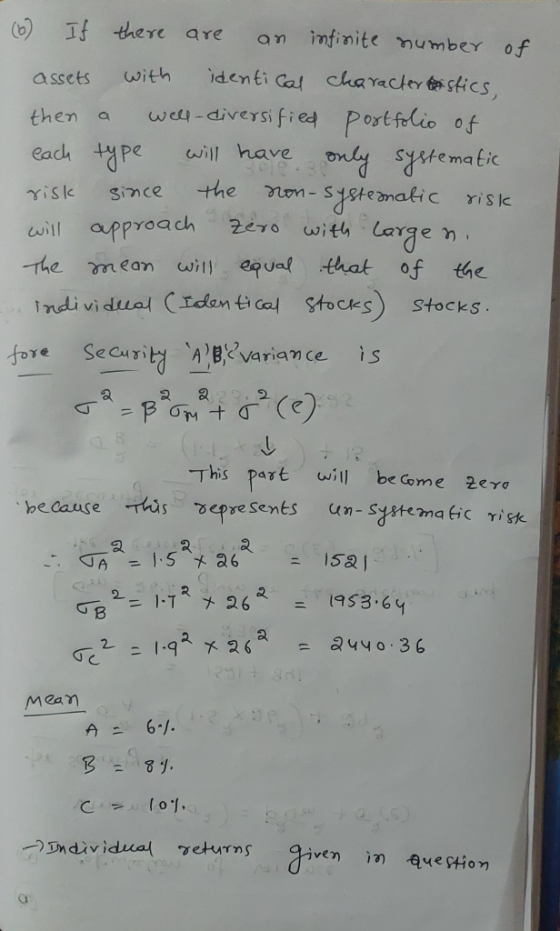

b. Now assume that there are an infinite number of assets with return characteristics identical to...

b. Now assume that there are an infinite number

of assets with return characteristics identical to those of

A, B, and C, respectively. What will be

the mean and variance of excess returns for securities A,

B, and C? (Enter the

variance answers as a percent squared and mean as a percentage. Do

not round intermediate calculations. Round your answers to the

nearest whole number.)

Problem 10-8 Assume that security returns are generated by the single index model R -...

b. Now assume that there are an infinite number

of assets with return characteristics identical to those of

A, B, and C, respectively. What will be

the mean and variance of excess returns for securities A,

B, and C? (Enter the

variance answers as a percent squared and mean as a percentage. Do

not round intermediate calculations. Round your answers to the

nearest whole number.)

Problem 10-8 Assume that security returns are generated by the single index model R -...

Assume that the returns on individual securities are generated by the following two-factor model:...

Assume that the returns on individual securities are generated by the following two-factor model: Rit=E(Rit)+βijF1t+βi2F2tRit=E(Rit)+βijF1t+βi2F2t Here: Rit is the return on Security i at Time t. F1t and F2t are market factors with zero expectation and zero covariance. In addition, assume that there is a capital market for four securities, and the capital market for these four assets is perfect in the sense that there are no transaction costs and short sales (i.e., negative positions) are permitted. The characteristics of...

Assume that the returns on individual securities are generated by the following two-factor model: E(Rit)Bj Fıt...

Assume that the returns on individual securities are generated by the following two-factor model: E(Rit)Bj Fıt + BgFu Rit Here: Rr is the return on Security i at Time t F and F are market factors with zero expectation and zero covariance. In addition, assume that there is a capital market for four securities, and the capital market for these four assets is perfect in the sense that there are no transaction costs and short sales (i., negative positions) are...

Assume that the returns on individual securities are generated by the following two-factor model: E(Rit)Bj Fıt + BgFu Rit Here: Rr is the return on Security i at Time t F and F are market factors with zero expectation and zero covariance. In addition, assume that there is a capital market for four securities, and the capital market for these four assets is perfect in the sense that there are no transaction costs and short sales (i., negative positions) are...

Assume that security returns are generated by the single-index model, Ri - Qi + BiRM + ei where R is the excess return for security i and Ry is the market's excess return. The risk-free rate is 2%. Suppose also that there are three securities A, B, and C, characterized by the following data: Security Bi A 0. 6 B 0.9 C 1.2 E(Ri) (ei) 7 % 16% 107 13 10 a. If Om = 10%, calculate the variance of...

Assume that security returns are generated by the single-index model, Ri - Qi + BiRM + ei where R is the excess return for security i and Ry is the market's excess return. The risk-free rate is 2%. Suppose also that there are three securities A, B, and C, characterized by the following data: Security Bi A 0. 6 B 0.9 C 1.2 E(Ri) (ei) 7 % 16% 107 13 10 a. If Om = 10%, calculate the variance of...

Assume that security returns are generated by the single index R; - a1 + RM + ei return where R is the excess return for security / and Ry is the three securities A, B, and C, characterized by the following data The risk-free rate is 4%. Suppose also that there are Security Bi E(R) olej) A 0.8 15 24% B 1.1 18 15 C 1.4 21 18 a. If om = 20%, calculate the variance ces Variance Security A...

Assume that security returns are generated by the single index R; - a1 + RM + ei return where R is the excess return for security / and Ry is the three securities A, B, and C, characterized by the following data The risk-free rate is 4%. Suppose also that there are Security Bi E(R) olej) A 0.8 15 24% B 1.1 18 15 C 1.4 21 18 a. If om = 20%, calculate the variance ces Variance Security A...

Assume security returns are generated by the single-index

model. R 1 =a 1 + beta 2 R M +e 1 where R 1 is the excess return

for security and R N market’s excess returnThe risk-free rate is 4%

Suppose also that there are three securities A8and characterized by

the following data!

Saved Assume that security returns are generated by the single-index model R; - ei + BiRM + ej where is the excess return for security i and Ry...

Assume security returns are generated by the single-index

model. R 1 =a 1 + beta 2 R M +e 1 where R 1 is the excess return

for security and R N market’s excess returnThe risk-free rate is 4%

Suppose also that there are three securities A8and characterized by

the following data!

Saved Assume that security returns are generated by the single-index model R; - ei + BiRM + ej where is the excess return for security i and Ry...

b. Now assume that there are an infinite number

of assets with return characteristics identical to those of

A, B, and C, respectively. What will be

the mean and variance of excess returns for securities A,

B, and C? (Enter the

variance answers as a percent squared and mean as a percentage. Do

not round intermediate calculations. Round your answers to the

nearest whole number.)

Problem 10-8 Assume that security returns are generated by the single index model R -...

b. Now assume that there are an infinite number

of assets with return characteristics identical to those of

A, B, and C, respectively. What will be

the mean and variance of excess returns for securities A,

B, and C? (Enter the

variance answers as a percent squared and mean as a percentage. Do

not round intermediate calculations. Round your answers to the

nearest whole number.)

Problem 10-8 Assume that security returns are generated by the single index model R -...

Assume that the returns on individual securities are generated by the following two-factor model: E(Rit)Bj Fıt + BgFu Rit Here: Rr is the return on Security i at Time t F and F are market factors with zero expectation and zero covariance. In addition, assume that there is a capital market for four securities, and the capital market for these four assets is perfect in the sense that there are no transaction costs and short sales (i., negative positions) are...

Assume that the returns on individual securities are generated by the following two-factor model: E(Rit)Bj Fıt + BgFu Rit Here: Rr is the return on Security i at Time t F and F are market factors with zero expectation and zero covariance. In addition, assume that there is a capital market for four securities, and the capital market for these four assets is perfect in the sense that there are no transaction costs and short sales (i., negative positions) are...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 1 year ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 1 year ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 1 year ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 1 year ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 1 year ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 1 year ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 1 year ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 1 year ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 1 year ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 1 year ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 1 year ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 1 year ago