Journalize the following merchandise transactions. Refer to the Chart of Accounts for exact wording of account...

Journalize the following merchandise transactions. Refer to the Chart of Accounts for exact wording of account titles.

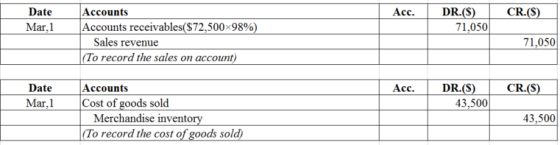

| Mar. | 1 | Sold merchandise on account, $72,500 with terms 2/10, n/30. The cost of the merchandise sold was $43,500. |

| 9 | Received payment less the discount. | |

| 13 | Issued a credit memo for returned merchandise that was sold for $2,300 terms n/30. The cost of the merchandise returned was $1,600. |

| CHART OF ACCOUNTS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| General Ledger | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Homework Answers

A. sold merchandise on account $72,500 with terms 2/10, n/30. The cost of merchandise sold

was $43,500.

B. Received payment less the discount.

72,500 - (72,500*.02) = 71,050

A) Accounts Receivable 71,050

Sales 71,050

Cost of Goods Sold 43,500

Inventory 43,500

B) Cash 71,050

Accounts Receivable 71,050

C) Customer Refunds payable 2300

Accounts Receivable 2300

(To record the sales return)

Merchandise Inventory: It is an asset to the Company. These are goods of the company which can be in forms of raw material, work in progress and finished goods. These goods were held by the company in day to day operations of the business.

Journal:

Journal entry is the first step in the accounting. It is recorded to keep accounting transaction in the chronological order, after recording the journal entries; ledger can be prepared and financial statements afterwards.

Meaning of term 2/10, n/30:

This term means that if the payment is made within 10 days, then 2% discount will be provided on the invoice value. If the payment is made within 30 days, then no discount will be provided. It means the seller has given 30 days’ credit period.

Net method:

Under net method, the sales are recorded at the net amount (after providing cash discount).

Working note:

Compute the sales value net of discounts as shown below:

Prepare the journal entry to record the sales as shown below:

Prepare the journal to record the receipt of payment.

Add Answer to:

Journalize the following merchandise transactions. Refer to the

Chart of Accounts for exact wording of account...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago