Homework Answers

Since the working requires lots of symbols and notation, I am producing a hand written solution.

The symbols used in the solution below are either the ones contained in the question or others having usual meaning in the subject of insurance.

Please see the solution below:

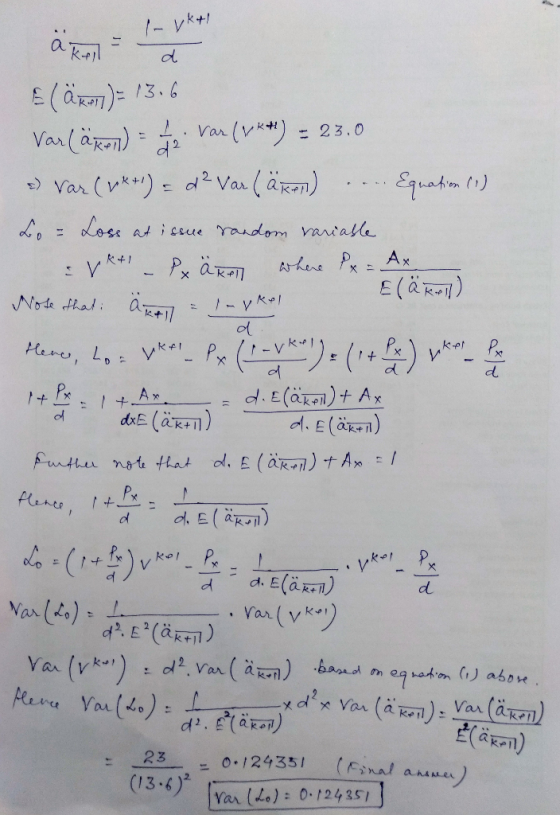

Final Answer is Var(L0) = 0.124351

Add Answer to:

Consider a fully discrete whole life insurance of 1 to (r) with the following details: K...

Let Lı denote the loss-at-time-zero random variable for a unit benefit fully continuous whole life insurance on (x) where it is assumed that the premium rate, π, is calculated using the equivalence p...

Let Lı denote the loss-at-time-zero random variable for a unit benefit fully continuous whole life insurance on (x) where it is assumed that the premium rate, π, is calculated using the equivalence principle. Let L2 denote the loss-at-time-zero random variable for the same insurance on (x) assuming that the premium rate, π2, is (4/3) . Find E(L2) and Var(L2) given the following: (c) δ-08. (a) Var(L1)-.5652, (b.) āz-5,

Let Lı denote the loss-at-time-zero random variable for a unit benefit fully...

Let Lı denote the loss-at-time-zero random variable for a unit benefit fully continuous whole life insurance on (x) where it is assumed that the premium rate, π, is calculated using the equivalence principle. Let L2 denote the loss-at-time-zero random variable for the same insurance on (x) assuming that the premium rate, π2, is (4/3) . Find E(L2) and Var(L2) given the following: (c) δ-08. (a) Var(L1)-.5652, (b.) āz-5,

Let Lı denote the loss-at-time-zero random variable for a unit benefit fully...

4. A fully discrete whole life insurance policy paying $50,000 at the end of the year...

4. A fully discrete whole life insurance policy paying $50,000 at the end of the year of death is issued to an individual age 36. The net premium reserve at the end of 10 years is $8,000. The net premium for this policy is $900 and the net premium for an identical policy issued to an individual age 46 is P. The effective annual interest rate of interest is 6%. Determine P.

4. A fully discrete whole life insurance policy paying $50,000 at the end of the year of death is issued to an individual age 36. The net premium reserve at the end of 10 years is $8,000. The net premium for this policy is $900 and the net premium for an identical policy issued to an individual age 46 is P. The effective annual interest rate of interest is 6%. Determine P.

2. For a special fully discrete 10-payment whole life insurance on (30) with level annual net...

2. For a special fully discrete 10-payment whole life insurance on (30) with level annual net premium P: (i) The death benefit is equal to 1000 plus the refund, without interest, of the net premiums paid. (ii) i = 0.04 (iii) A30 = 0.30 (iv) 30. 10 = 0.014 (v) (14)zo:707 = 0.048 (vi) ä30:101 - 8.5 Calculate P

2. For a special fully discrete 10-payment whole life insurance on (30) with level annual net premium P: (i) The death benefit is equal to 1000 plus the refund, without interest, of the net premiums paid. (ii) i = 0.04 (iii) A30 = 0.30 (iv) 30. 10 = 0.014 (v) (14)zo:707 = 0.048 (vi) ä30:101 - 8.5 Calculate P

Let X be a discrete random variable with the following PMF. Px(k) = 1/4 for k...

Let X be a discrete random variable with the following PMF. Px(k) = 1/4 for k = -2 1/8 for k = -1 1/8 for k = 0 1/4 for k = 1 1/4 for k = 2 0 otherwise Define a new random variable Y = (X + 1)2 a) Find E[X] and Var[X] b) Find the range of Y and write its PMF. c) Show that the PMF of Y is a valid PMF. d) Find P(Y ≤...

Let X be a discrete random variable with the following PMF 6 for k € {-10,-9,...

Let X be a discrete random variable with the following PMF 6 for k € {-10,-9, -, -1,0, 1, ... , 9, 10} Px(k) = otherwise The random variable Y = g(X) is defined as Y = g(x) = {x if X < 0 if 0 < X <5 otherwise Calculate E[X], E[Y], var(X), and var(Y) for the two variables X and Y

Let X be a discrete random variable with the following PMF 6 for k € {-10,-9, -, -1,0, 1, ... , 9, 10} Px(k) = otherwise The random variable Y = g(X) is defined as Y = g(x) = {x if X < 0 if 0 < X <5 otherwise Calculate E[X], E[Y], var(X), and var(Y) for the two variables X and Y

Problem 3 A discrete random variable Y takes values {k= 0, 1, 2, ...,} such that...

Problem 3 A discrete random variable Y takes values {k= 0, 1, 2, ...,} such that PLY Z k} = ()* for k 20. 1. Derive P[Y = k) for any k > 0. 2. Evaluate expectation, E[Y] = 3. Given E[Y(Y - 1)] = 15 , find variance of Y, Var[Y] =

Problem 3 A discrete random variable Y takes values {k= 0, 1, 2, ...,} such that PLY Z k} = ()* for k 20. 1. Derive P[Y = k) for any k > 0. 2. Evaluate expectation, E[Y] = 3. Given E[Y(Y - 1)] = 15 , find variance of Y, Var[Y] =

Consider a discrete random variable X that can assume three values 1, 2, and k with...

Consider a discrete random variable X that can assume three values 1, 2, and k with respective probabilities 0.2, 0.5, and 0.3. If E(X) = 2.7, what is the value of k? Select one: a. 3 b. 1 c. 4 d. 5 e. 2

5. Consider a 10-year annual premium endowment insurance with sum insured $200,000 issued to a life...

5. Consider a 10-year annual premium endowment insurance with sum insured $200,000 issued to a life aged 40, Assume initial expenses of 4% of the basic sum insured and 15% of the first premium,and renewal expenses of3% ofthe second and subsequent premiums. Assume that the death benefit is payable at the end of the year of death. (a) Write down an expression for the gross future loss random variable I4 (10 pts.) (b) Calculate the gross annual premium. (8 pts.)

5. Consider a 10-year annual premium endowment insurance with sum insured $200,000 issued to a life aged 40, Assume initial expenses of 4% of the basic sum insured and 15% of the first premium,and renewal expenses of3% ofthe second and subsequent premiums. Assume that the death benefit is payable at the end of the year of death. (a) Write down an expression for the gross future loss random variable I4 (10 pts.) (b) Calculate the gross annual premium. (8 pts.)

Consider a discrete random variable X with pmf x)-(1-p1 p. defined for x - 1, 2,...

Consider a discrete random variable X with pmf x)-(1-p1 p. defined for x - 1, 2, 3,..The moment generating function for this kind of random variable is M(t)Pe 1-(1-P)et. (a) What is E(X)? O p(1-P) 1-P (a) What is Var(x)? 1-p p2 p(1-P) O p(1-P) o -p

Consider a discrete random variable X with pmf x)-(1-p1 p. defined for x - 1, 2, 3,..The moment generating function for this kind of random variable is M(t)Pe 1-(1-P)et. (a) What is E(X)? O p(1-P) 1-P (a) What is Var(x)? 1-p p2 p(1-P) O p(1-P) o -p

1. Consider a discrete random variable, X, where the outcome of this random variable is determined...

1. Consider a discrete random variable, X, where the outcome of this random variable is determined by throwing a 6-sided die. X takes on integer values 1,2,…,6. The die is fair. That is, P(X=1)= P(X=2)=…= P(X=6). i. Draw the probability distribution function for this random variable. Carefully label the graph. ii. Draw the cumulative distribution function for X. iii. Calculate the following: P(X=4) P(X≠5) P(X=1 or X=6) P(X4) E(X) Var(X) sd(X) iv. Consider the random variable Y where the outcome...

Let Lı denote the loss-at-time-zero random variable for a unit benefit fully continuous whole life insurance on (x) where it is assumed that the premium rate, π, is calculated using the equivalence principle. Let L2 denote the loss-at-time-zero random variable for the same insurance on (x) assuming that the premium rate, π2, is (4/3) . Find E(L2) and Var(L2) given the following: (c) δ-08. (a) Var(L1)-.5652, (b.) āz-5,

Let Lı denote the loss-at-time-zero random variable for a unit benefit fully...

Let Lı denote the loss-at-time-zero random variable for a unit benefit fully continuous whole life insurance on (x) where it is assumed that the premium rate, π, is calculated using the equivalence principle. Let L2 denote the loss-at-time-zero random variable for the same insurance on (x) assuming that the premium rate, π2, is (4/3) . Find E(L2) and Var(L2) given the following: (c) δ-08. (a) Var(L1)-.5652, (b.) āz-5,

Let Lı denote the loss-at-time-zero random variable for a unit benefit fully...

4. A fully discrete whole life insurance policy paying $50,000 at the end of the year of death is issued to an individual age 36. The net premium reserve at the end of 10 years is $8,000. The net premium for this policy is $900 and the net premium for an identical policy issued to an individual age 46 is P. The effective annual interest rate of interest is 6%. Determine P.

4. A fully discrete whole life insurance policy paying $50,000 at the end of the year of death is issued to an individual age 36. The net premium reserve at the end of 10 years is $8,000. The net premium for this policy is $900 and the net premium for an identical policy issued to an individual age 46 is P. The effective annual interest rate of interest is 6%. Determine P.

2. For a special fully discrete 10-payment whole life insurance on (30) with level annual net premium P: (i) The death benefit is equal to 1000 plus the refund, without interest, of the net premiums paid. (ii) i = 0.04 (iii) A30 = 0.30 (iv) 30. 10 = 0.014 (v) (14)zo:707 = 0.048 (vi) ä30:101 - 8.5 Calculate P

2. For a special fully discrete 10-payment whole life insurance on (30) with level annual net premium P: (i) The death benefit is equal to 1000 plus the refund, without interest, of the net premiums paid. (ii) i = 0.04 (iii) A30 = 0.30 (iv) 30. 10 = 0.014 (v) (14)zo:707 = 0.048 (vi) ä30:101 - 8.5 Calculate P

Let X be a discrete random variable with the following PMF 6 for k € {-10,-9, -, -1,0, 1, ... , 9, 10} Px(k) = otherwise The random variable Y = g(X) is defined as Y = g(x) = {x if X < 0 if 0 < X <5 otherwise Calculate E[X], E[Y], var(X), and var(Y) for the two variables X and Y

Let X be a discrete random variable with the following PMF 6 for k € {-10,-9, -, -1,0, 1, ... , 9, 10} Px(k) = otherwise The random variable Y = g(X) is defined as Y = g(x) = {x if X < 0 if 0 < X <5 otherwise Calculate E[X], E[Y], var(X), and var(Y) for the two variables X and Y

Problem 3 A discrete random variable Y takes values {k= 0, 1, 2, ...,} such that PLY Z k} = ()* for k 20. 1. Derive P[Y = k) for any k > 0. 2. Evaluate expectation, E[Y] = 3. Given E[Y(Y - 1)] = 15 , find variance of Y, Var[Y] =

Problem 3 A discrete random variable Y takes values {k= 0, 1, 2, ...,} such that PLY Z k} = ()* for k 20. 1. Derive P[Y = k) for any k > 0. 2. Evaluate expectation, E[Y] = 3. Given E[Y(Y - 1)] = 15 , find variance of Y, Var[Y] =

5. Consider a 10-year annual premium endowment insurance with sum insured $200,000 issued to a life aged 40, Assume initial expenses of 4% of the basic sum insured and 15% of the first premium,and renewal expenses of3% ofthe second and subsequent premiums. Assume that the death benefit is payable at the end of the year of death. (a) Write down an expression for the gross future loss random variable I4 (10 pts.) (b) Calculate the gross annual premium. (8 pts.)

5. Consider a 10-year annual premium endowment insurance with sum insured $200,000 issued to a life aged 40, Assume initial expenses of 4% of the basic sum insured and 15% of the first premium,and renewal expenses of3% ofthe second and subsequent premiums. Assume that the death benefit is payable at the end of the year of death. (a) Write down an expression for the gross future loss random variable I4 (10 pts.) (b) Calculate the gross annual premium. (8 pts.)

Consider a discrete random variable X with pmf x)-(1-p1 p. defined for x - 1, 2, 3,..The moment generating function for this kind of random variable is M(t)Pe 1-(1-P)et. (a) What is E(X)? O p(1-P) 1-P (a) What is Var(x)? 1-p p2 p(1-P) O p(1-P) o -p

Consider a discrete random variable X with pmf x)-(1-p1 p. defined for x - 1, 2, 3,..The moment generating function for this kind of random variable is M(t)Pe 1-(1-P)et. (a) What is E(X)? O p(1-P) 1-P (a) What is Var(x)? 1-p p2 p(1-P) O p(1-P) o -p

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago