![Problem 5-17 Comprehensive Problem (LO2, LO3, LO4, LOS, LO7] Gold Nest Company of Hong Kong is a family-owned enterprise that](http://img.homeworklib.com/questions/1263e560-708b-11ea-8bca-1b2359575122.png?x-oss-process=image/resize,w_560)

Problem 5-17 Comprehensive

Problem [LO2, LO3, LO4, LO5, LO7]

Problem 5-17 Comprehensive

Problem [LO2, LO3, LO4, LO5, LO7]

Homework Answers

Predetermined manufacturing overhead rate = Budgeted manufacturing overhead/Total estimated direct labor cost = $330000/$200000 = 165% of direct labor cost

1.

| Transaction | General Journal | Debit | Credit |

| a. | Raw Materials | 275000 | |

| Accounts payable | 275000 | ||

| (To record raw materials purchased on account) | |||

| b. | Work in process | 220000 | |

| Manufacturing overheads | 60000 | ||

| Raw Materials | 280000 | ||

| (To record raw materials requisitioned) | |||

| c. | Work in process | 180000 | |

| Manufacturing overheads | 72000 | ||

| Sales commission expense | 63000 | ||

| Administrative salaries expense | 90000 | ||

| Cash | 405000 | ||

| (To record cost of employee services incurred) | |||

| d. | Manufacturing overheads | 60000 | |

| Rent expense | 15000 | ||

| Cash | 75000 | ||

| (To record rent incurred) | |||

| e. | Manufacturing overheads | 57000 | |

| Cash | 57000 | ||

| (To record utilities costs incurred) | |||

| f. | Advertising expense | 14000 | |

| Cash | 14000 | ||

| (To record advertising costs incurred) | |||

| g. | Manufacturing overheads | 88000 | |

| Depreciation expense | 12000 | ||

| Accumulated depreciation-equipment | 100000 | ||

| (To record depreciation on equipment) | |||

| h. | Work in process | 297000 | |

| Manufacturing overheads (165% x $180000) | 297000 | ||

| (To record manufacturing overhead applied to jobs) | |||

| i. | Finished goods | 675000 | |

| Work in process | 675000 | ||

| (To record cost of jobs completed) | |||

| j(1) | Accounts receivable | 1250000 | |

| Sales Revenue | 1250000 | ||

| (To record sales on account) | |||

| j(2) | Cost of goods sold | 700000 | |

| Finished goods | 700000 | ||

| (To record cost of goods sold) |

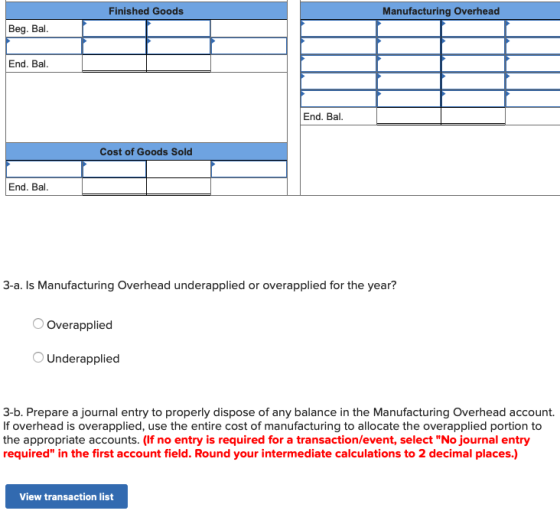

2.

| Raw Materials | |||

| Beg. Bal. | 25000 | 280000 | b. |

| a. | 275000 | ||

| End. Bal. | 20000 | ||

| Work in Process | |||

| Beg. Bal. | 10000 | 675000 | i. |

| b. | 220000 | ||

| c. | 180000 | ||

| h. | 297000 | ||

| End. Bal. | 32000 | ||

| Finished Goods | |||

| Beg. Bal. | 40000 | 700000 | j(2) |

| i. | 675000 | ||

| End. Bal. | 15000 | ||

| Manufacturing Overhead | |||

| b. | 60000 | 297000 | h. |

| c. | 72000 | ||

| d. | 60000 | ||

| e. | 57000 | ||

| g. | 88000 | ||

| End. Bal. | 40000 | ||

| Cost of Goods Sold | |||

| j(2) | 700000 | ||

| End. Bal. | 700000 | ||

3-a. Underapplied

Manufacturing overhead incurred $337000 - Manufacturing overhead applied $297000 = Overheads underapplied $40000

3-b.

| Event | General Journal | Debit | Credit |

| 1 | Cost of goods sold | 40000 | |

| Manufacturing overhead | 40000 | ||

| (To close manufacturing overhead to cost of goods sold) |

4.

| Gold Nest Company | ||

| Income Statement | ||

| For the Year Ended June 30 | ||

| Sales | 1250000 | |

| Cost of goods sold ($700000 + $40000) | 740000 | |

| Gross profit | 510000 | |

| Selling and administrative expenses: | ||

| Sales commission expense | 63000 | |

| Advertising expense | 14000 | |

| Administrative salaries expense | 90000 | |

| Rent expense | 15000 | |

| Depreciation expense | 12000 | 194000 |

| Net income | 316000 | |

Add Answer to:

Problem 5-17 Comprehensive

Problem [LO2, LO3, LO4, LO5, LO7]

Problem 5-17 Comprehensive Problem (LO2, LO3, LO4,...

Need help with checking Q1-4 and finishing Q5... Thanks Problem 5-30 Comprehensive Problem (LO3, LO4, LOS,...

Need help with checking Q1-4 and finishing Q5... Thanks

Problem 5-30 Comprehensive Problem (LO3, LO4, LOS, LO7) Mountain Manufacturing Company produces custom stamped metal parts for a variety of customers in Western Canada. During January, the company had two jobs in process. Job A was an order for 1,200 stamped parts and was started in December. Job Ahad $12,000 of manufacturing costs already accumulated on January 1. Job B was an order for 1,000 stamped parts and was started in...

Need help with checking Q1-4 and finishing Q5... Thanks

Problem 5-30 Comprehensive Problem (LO3, LO4, LOS, LO7) Mountain Manufacturing Company produces custom stamped metal parts for a variety of customers in Western Canada. During January, the company had two jobs in process. Job A was an order for 1,200 stamped parts and was started in December. Job Ahad $12,000 of manufacturing costs already accumulated on January 1. Job B was an order for 1,000 stamped parts and was started in...

Problem 6-15 Comprehensive Process Costing Problem (LO1, LO2, LO3, LO4, L05) Fryer's Choice produces a specially...

Problem 6-15 Comprehensive Process Costing Problem (LO1, LO2, LO3, LO4, L05) Fryer's Choice produces a specially blended vegetable oil widely used in restaurant deep fryers. The blending process creates a cooking oil that can be heated to a high temperature, but does not smoke or smell. The oil is produced in two departments: Blending and Bottling. Raw materials are introduced at various points in the Blending Department. The following incomplete Work in Process T-account is available for the Blending Department...

Problem 6-15 Comprehensive Process Costing Problem (LO1, LO2, LO3, LO4, L05) Fryer's Choice produces a specially blended vegetable oil widely used in restaurant deep fryers. The blending process creates a cooking oil that can be heated to a high temperature, but does not smoke or smell. The oil is produced in two departments: Blending and Bottling. Raw materials are introduced at various points in the Blending Department. The following incomplete Work in Process T-account is available for the Blending Department...

Problem 3-16 Comprehensive Problem [LO3-1, LO3-2, LO3-4] Gold Nest Company of Guandong, China, is a family-owned...

Problem 3-16 Comprehensive Problem [LO3-1, LO3-2, LO3-4] Gold Nest Company of Guandong, China, is a family-owned enterprise that makes birdcages for the South China market. The company sells its birdcages through an extensive network of street vendors who receive commissions on their sales The company uses a job-order costing system in which overhead is applied to jobs on the basis of direct labor cost. Its predetermined overhead rate is based on a cost formula that estimated $60,000 of manufacturing overhead...

Problem 3-16 Comprehensive Problem [LO3-1, LO3-2, LO3-4] Gold Nest Company of Guandong, China, is a family-owned enterprise that makes birdcages for the South China market. The company sells its birdcages through an extensive network of street vendors who receive commissions on their sales The company uses a job-order costing system in which overhead is applied to jobs on the basis of direct labor cost. Its predetermined overhead rate is based on a cost formula that estimated $60,000 of manufacturing overhead...

Problem 3-16 Comprehensive Problem (LO3-1, LO3-2, LO3-4) points Gold Nest Company of Guandong, China, is a...

Problem 3-16 Comprehensive Problem (LO3-1, LO3-2, LO3-4) points Gold Nest Company of Guandong, China, is a family-owned enterprise that makes birdcages for the South China market. The company sells its birdcages through an extensive network of street vendors who receive commissions on their sales The company uses a job-order costing system in which overhead is applied to jobs on the basis of direct labor cost. Its predetermined overhead rate is based on a cost formula that estimated $76,000 of manufacturing...

Problem 3-16 Comprehensive Problem (LO3-1, LO3-2, LO3-4) points Gold Nest Company of Guandong, China, is a family-owned enterprise that makes birdcages for the South China market. The company sells its birdcages through an extensive network of street vendors who receive commissions on their sales The company uses a job-order costing system in which overhead is applied to jobs on the basis of direct labor cost. Its predetermined overhead rate is based on a cost formula that estimated $76,000 of manufacturing...

Problem 5-18 Journal Entries; T-Accounts; Cost Flows [LO4, LO5, LO7] Ravsten Company uses a job-order costing system. On...

Problem 5-18 Journal Entries; T-Accounts; Cost Flows [LO4, LO5,

LO7]

Ravsten Company uses a job-order costing system. On January 1,

the beginning of the current year, the company’s inventory balances

were as follows:

Raw materials

$

20,000

Work in process

$

11,600

Finished goods

$

30,800

The company applies overhead cost to jobs on the basis of

machine-hours. For the current year, the company estimated that it

would work 36,800 machine-hours and incur $171,120 in manufacturing

overhead cost. The following...

Problem 5-18 Journal Entries; T-Accounts; Cost Flows [LO4, LO5,

LO7]

Ravsten Company uses a job-order costing system. On January 1,

the beginning of the current year, the company’s inventory balances

were as follows:

Raw materials

$

20,000

Work in process

$

11,600

Finished goods

$

30,800

The company applies overhead cost to jobs on the basis of

machine-hours. For the current year, the company estimated that it

would work 36,800 machine-hours and incur $171,120 in manufacturing

overhead cost. The following...

Problem 5-18 Journal Entries; T-Accounts; Cost Flows [LO4, LO5, LO7] Ravsten Company uses a job-order costing...

Problem 5-18 Journal Entries; T-Accounts; Cost Flows [LO4, LO5, LO7] Ravsten Company uses a job-order costing system. On January 1, the beginning of the current year, the company’s inventory balances were as follows: Raw materials $ 16,500 Work in process $ 10,200 Finished goods $ 30,100 The company applies overhead cost to jobs on the basis of machine-hours. For the current year, the company estimated that it would work 36,100 machine-hours and incur $155,230 in manufacturing overhead cost. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Need help with checking Q1-4 and finishing Q5... Thanks

Problem 5-30 Comprehensive Problem (LO3, LO4, LOS, LO7) Mountain Manufacturing Company produces custom stamped metal parts for a variety of customers in Western Canada. During January, the company had two jobs in process. Job A was an order for 1,200 stamped parts and was started in December. Job Ahad $12,000 of manufacturing costs already accumulated on January 1. Job B was an order for 1,000 stamped parts and was started in...

Need help with checking Q1-4 and finishing Q5... Thanks

Problem 5-30 Comprehensive Problem (LO3, LO4, LOS, LO7) Mountain Manufacturing Company produces custom stamped metal parts for a variety of customers in Western Canada. During January, the company had two jobs in process. Job A was an order for 1,200 stamped parts and was started in December. Job Ahad $12,000 of manufacturing costs already accumulated on January 1. Job B was an order for 1,000 stamped parts and was started in...

Problem 6-15 Comprehensive Process Costing Problem (LO1, LO2, LO3, LO4, L05) Fryer's Choice produces a specially blended vegetable oil widely used in restaurant deep fryers. The blending process creates a cooking oil that can be heated to a high temperature, but does not smoke or smell. The oil is produced in two departments: Blending and Bottling. Raw materials are introduced at various points in the Blending Department. The following incomplete Work in Process T-account is available for the Blending Department...

Problem 6-15 Comprehensive Process Costing Problem (LO1, LO2, LO3, LO4, L05) Fryer's Choice produces a specially blended vegetable oil widely used in restaurant deep fryers. The blending process creates a cooking oil that can be heated to a high temperature, but does not smoke or smell. The oil is produced in two departments: Blending and Bottling. Raw materials are introduced at various points in the Blending Department. The following incomplete Work in Process T-account is available for the Blending Department...

Problem 3-16 Comprehensive Problem [LO3-1, LO3-2, LO3-4] Gold Nest Company of Guandong, China, is a family-owned enterprise that makes birdcages for the South China market. The company sells its birdcages through an extensive network of street vendors who receive commissions on their sales The company uses a job-order costing system in which overhead is applied to jobs on the basis of direct labor cost. Its predetermined overhead rate is based on a cost formula that estimated $60,000 of manufacturing overhead...

Problem 3-16 Comprehensive Problem [LO3-1, LO3-2, LO3-4] Gold Nest Company of Guandong, China, is a family-owned enterprise that makes birdcages for the South China market. The company sells its birdcages through an extensive network of street vendors who receive commissions on their sales The company uses a job-order costing system in which overhead is applied to jobs on the basis of direct labor cost. Its predetermined overhead rate is based on a cost formula that estimated $60,000 of manufacturing overhead...

Problem 3-16 Comprehensive Problem (LO3-1, LO3-2, LO3-4) points Gold Nest Company of Guandong, China, is a family-owned enterprise that makes birdcages for the South China market. The company sells its birdcages through an extensive network of street vendors who receive commissions on their sales The company uses a job-order costing system in which overhead is applied to jobs on the basis of direct labor cost. Its predetermined overhead rate is based on a cost formula that estimated $76,000 of manufacturing...

Problem 3-16 Comprehensive Problem (LO3-1, LO3-2, LO3-4) points Gold Nest Company of Guandong, China, is a family-owned enterprise that makes birdcages for the South China market. The company sells its birdcages through an extensive network of street vendors who receive commissions on their sales The company uses a job-order costing system in which overhead is applied to jobs on the basis of direct labor cost. Its predetermined overhead rate is based on a cost formula that estimated $76,000 of manufacturing...

Problem 5-18 Journal Entries; T-Accounts; Cost Flows [LO4, LO5,

LO7]

Ravsten Company uses a job-order costing system. On January 1,

the beginning of the current year, the company’s inventory balances

were as follows:

Raw materials

$

20,000

Work in process

$

11,600

Finished goods

$

30,800

The company applies overhead cost to jobs on the basis of

machine-hours. For the current year, the company estimated that it

would work 36,800 machine-hours and incur $171,120 in manufacturing

overhead cost. The following...

Problem 5-18 Journal Entries; T-Accounts; Cost Flows [LO4, LO5,

LO7]

Ravsten Company uses a job-order costing system. On January 1,

the beginning of the current year, the company’s inventory balances

were as follows:

Raw materials

$

20,000

Work in process

$

11,600

Finished goods

$

30,800

The company applies overhead cost to jobs on the basis of

machine-hours. For the current year, the company estimated that it

would work 36,800 machine-hours and incur $171,120 in manufacturing

overhead cost. The following...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago