Homework Answers

Compute Predetermined overhead rate = $350,000/1000 direct labor hours = $350

1.

Prepare journal entries as follows:

| Trn. No | Account Titles | Debit | Credit |

| a | Raw material inventory | $250,000 | |

| Accounts payable | $250,000 | ||

| b | Work in process inventory | $235,000 | |

| Raw material inventory | $235,000 | ||

| c | Manufacturing overhead | $62,100 | |

| Utility expenses | $6,900 | ||

| Accounts payable | $69,000 | ||

| d | Work in process inventory | $280,000 | |

| Manufacturing overhead | $100,000 | ||

| Salaries expenses | $160,000 | ||

| Wages payable | $540,000 | ||

| e | Manufacturing overhead | $64,000 | |

| Accounts payable | $64,000 | ||

| f | Advertisement expenses | $146,000 | |

| Accounts payable | $146,000 | ||

| g | Manufacturing overhead | $61,500 | |

| Depreciation expenses | $20,500 | ||

| Accumulated depreciation | $82,000 | ||

| h | Manufacturing overhead | $85,600 | |

| Rent expenses | $21,400 | ||

| Accounts payable | $107,000 | ||

| i | Work in process inventory ($350 × 1075 hours) | $376,250 | |

| Manufacturing overhead | $376,250 | ||

| j | Finished good inventory | $870,000 | |

| Work in process inventory | $870,000 | ||

| k | Accounts receivable | $1,700,000 | |

| Sale | $1,700,000 | ||

| COGS | $900,000 | ||

| Finished good inventory | $900,000 |

_____________________________________________________________________

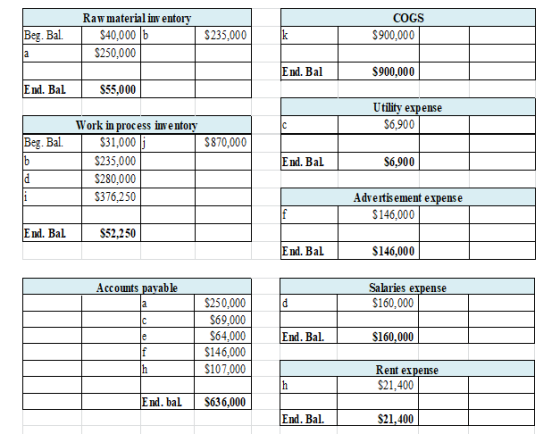

2.

Prepare t-accounts as follows:

_____________________________________________________________

3.

Prepare a schedule of Cost of goods manufactured as follows:

| Direct material: | |

| Raw material inventory: Beginning | $40,000 |

| Add: Purchase of raw material | $250,000 |

| Raw material available | $290,000 |

| Less: Raw material ending inventory | ($55,000) |

| Raw material used in production | $235,000 |

| Direct labor | $280,000 |

| Manufacturing overhead applied to WIP | $376,250 |

| Total manufacturing cost | $891,250 |

| Add: Beginning WIP inventory | $31,000 |

| Less: Ending WIP inventory | ($52,250) |

| Cost of Goods manufactured | $870,000 |

Add Answer to:

4a

4b and 5 not answered... thank you

signment Print View Page 1 Award: 5.00 points...

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is...

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000 of manufacturing overhead for an estimated location base of 1,000 direct labor-hours. The following transactions took place...

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000 of manufacturing overhead for an estimated location base of 1,000 direct labor-hours. The following transactions took place...

Homework- (someone answered but the excel was impossible to read)

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $370,500 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account, $270,000.Raw...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

cant get number # 2 to come out right and number 4a and #5. please help...thank...

cant get number # 2 to come out right and number 4a and #5.

please help...thank you

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000...

cant get number # 2 to come out right and number 4a and #5.

please help...thank you

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following...

Froya Fabrikker A/S of Bergen, Norway, is a small company thatmanufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $349,800 of manufacturing overhead for an

estimated allocation base of 1,060 direct labor-hours. The

following transactions took place during the year:Raw materials purchased on account, $230,000.Raw...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $349,800 of manufacturing overhead for an

estimated allocation base of 1,060 direct labor-hours. The

following transactions took place during the year:Raw materials purchased on account, $230,000.Raw...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $357,000 of manufacturing overhead for an estimated allocation base of 1,020 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the...

The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $342,000 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following transactions took place during the year: 1. Raw materials purchased on account, $210,000. 2. Raw materials used in production (all direct materials), $195,000. 3. Utility bills incurred on account, $61,000 (95% related to...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000 of manufacturing overhead for an estimated location base of 1,000 direct labor-hours. The following transactions took place...

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000 of manufacturing overhead for an estimated location base of 1,000 direct labor-hours. The following transactions took place...

cant get number # 2 to come out right and number 4a and #5.

please help...thank you

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000...

cant get number # 2 to come out right and number 4a and #5.

please help...thank you

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $349,800 of manufacturing overhead for an

estimated allocation base of 1,060 direct labor-hours. The

following transactions took place during the year:Raw materials purchased on account, $230,000.Raw...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $349,800 of manufacturing overhead for an

estimated allocation base of 1,060 direct labor-hours. The

following transactions took place during the year:Raw materials purchased on account, $230,000.Raw...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago