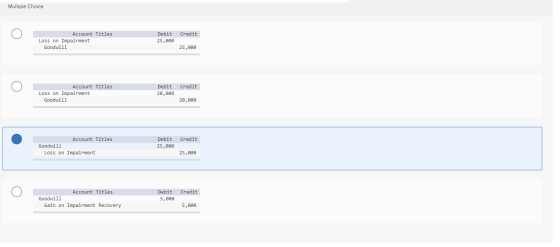

On January 1, Year 1, East Company purchased $60,000 of

goodwill. On December 31, Year 4 East determined that the goodwill

suffered a $25,000 permanent impairment. However, on December 31,

Year 6 East estimated that it had recovered $5,000 of the

impairment that had previously been considered to be a permanent

impairment. Which of the following journal entries was required to

recognize the impairment?

Homework Answers

ANSWER:

OPTION:

| Account titles | debit | credit |

|---|---|---|

|

Loss on impairment Goodwill |

$25000 . |

. $25000 |

EXPLANATION:

The above journal entry shall be passed which recognizes the permanent loss on account of impairment. The reversal of impairment on account of recovery is not allowed.

Add Answer to:

On January 1, Year 1, East Company purchased $60,000 of

goodwill. On December 31, Year 4...

On January 1, Year 1, East Company purchased $60,000 of goodwill. On December 31, Year 4...

On January 1, Year 1, East Company purchased $60,000 of goodwill. On December 31, Year 4 East determined that the goodwill suffered a $25,000 permanent impairment. However, on December 31, Year 6 East estimated that it had recovered $5,000 of the impairment that had previously been considered to be a permanent impairment. Which of the following journal entries was required to recognize the impairment. Account Titles Debit Credit Loss on Impairment 25,000 Goodwill 25,000 Account Titles Debit Credit Loss on...

Sheridan Company has the following investments as of December 31, 2020: Investments in common stock of...

Sheridan Company has the following investments as of December 31, 2020: Investments in common stock of Laser Company Investment in debt securities of FourSquare Company $1,630,000 $3,240,000 In both investments, the carrying value and the fair value of these two investments are the same at December 31, 2020. Sheridan's stock investments does not result in significant influence on the operations of Laser Company. Sheridan's debt investment is considered held-to-maturity. At December 31, 2021, the shares in Laser Company are valued...

Sheridan Company has the following investments as of December 31, 2020: Investments in common stock of Laser Company Investment in debt securities of FourSquare Company $1,630,000 $3,240,000 In both investments, the carrying value and the fair value of these two investments are the same at December 31, 2020. Sheridan's stock investments does not result in significant influence on the operations of Laser Company. Sheridan's debt investment is considered held-to-maturity. At December 31, 2021, the shares in Laser Company are valued...

At the end of its reporting year (December 31, 2017), Acme Inc. reports a $60,000 patent...

At the end of its reporting year (December 31, 2017), Acme Inc. reports a $60,000 patent with estimated remaining useful life of 10 years. Before closing its books, the company identifies a $20,000 impairment in the patent. For IFRS, Acme Inc. does not revalue its intangible assets. a. How will the impairment loss be recorded using US GAAP and for IFRS? b. Assume that at the end of 2018, Acme Inc. determines the company has recovered $12,000 of the patent...

Sheffield Company uses special strapping equipment in its packaging business. The equipment was purchased in January...

Sheffield Company uses special strapping equipment in its packaging business. The equipment was purchased in January 2019 for $11,700,000 and had an estimated useful life of 8 years with no salvage value. At December 31, 2020, new technology was introduced that would accelerate the obsolescence of Sheffield’s equipment. Sheffield’s controller estimates that expected future net cash flows on the equipment will be $7,371,000 and that the fair value of the equipment is $6,552,000. Sheffield intends to continue using the equipment,...

On January 1, 2017, Cullumber Company had a balance of $359,500 of goodwill on its balance...

On January 1, 2017, Cullumber Company had a balance of $359,500

of goodwill on its balance sheet that resulted from the purchase of

a small business in a prior year. The goodwill had an indefinite

life. During 2017, the company had the following additional

transactions.

Jan.

2

Purchased a patent (7-year life) $313,950.

July

1

Acquired a 8-year franchise; expiration date July 1, 2,025,

$583,200.

Sept.

1

Research and development costs $176,500.

Make an entry as of December 31, 2017,...

On January 1, 2017, Cullumber Company had a balance of $359,500

of goodwill on its balance sheet that resulted from the purchase of

a small business in a prior year. The goodwill had an indefinite

life. During 2017, the company had the following additional

transactions.

Jan.

2

Purchased a patent (7-year life) $313,950.

July

1

Acquired a 8-year franchise; expiration date July 1, 2,025,

$583,200.

Sept.

1

Research and development costs $176,500.

Make an entry as of December 31, 2017,...

On January 1, 2017, Blossam Company had a balance of $38.000 at goodwill on its balance...

On January 1, 2017, Blossam Company had a balance of $38.000 at goodwill on its balance sheet that resulted from the purchase of a small business in a priorynar. The goodwill had an indefinitelt. During 2017, the company had the following additional transact Jan. 2 Purchased a patent 15 year life $204.550. July 1 Acquired a 9-year franchise: expiration date July 12.026, $626.400. Sept. 1 Roscarch and development costs $182,500. no entry is required, select "No Entry for the Prepare...

On January 1, 2017, Blossam Company had a balance of $38.000 at goodwill on its balance sheet that resulted from the purchase of a small business in a priorynar. The goodwill had an indefinitelt. During 2017, the company had the following additional transact Jan. 2 Purchased a patent 15 year life $204.550. July 1 Acquired a 9-year franchise: expiration date July 12.026, $626.400. Sept. 1 Roscarch and development costs $182,500. no entry is required, select "No Entry for the Prepare...

Presented below is information related to equipment owned by Whispering Company at December 31, 2020. Cost...

Presented below is information related to equipment owned by Whispering Company at December 31, 2020. Cost (residual value $0) Accumulated depreciation to date Value-in-use Fair value less cost of disposal $8,924,900 995,900 5.510,000 4,395,380 Assume that Whispering will continue to use this asset in the future. As of December 31, 2020, the equipment has a remaining useful life of 8 years. Whispering uses straight-line depreciation. la) Your answer is correct. Prepare the journal entry (if any) to record the impairment...

Presented below is information related to equipment owned by Whispering Company at December 31, 2020. Cost (residual value $0) Accumulated depreciation to date Value-in-use Fair value less cost of disposal $8,924,900 995,900 5.510,000 4,395,380 Assume that Whispering will continue to use this asset in the future. As of December 31, 2020, the equipment has a remaining useful life of 8 years. Whispering uses straight-line depreciation. la) Your answer is correct. Prepare the journal entry (if any) to record the impairment...

Exercise 11-16 Presented below is information related to equipment owned by Windsor Company at December 31,...

Exercise 11-16 Presented below is information related to equipment owned by Windsor Company at December 31, 2020. Cost $9,720,000 Accumulated depreciation to date 1,080,000 Expected future net cash flows 7,560,000 Fair value 5,184,000 Assume that Windsor will continue to use this asset in the future. As of December 31, 2020, the equipment has a remaining useful life of 5 years. Your answer is partially correct. Try again. Prepare the journal entry (if any) to record the impairment of the asset...

Exercise 11-16 Presented below is information related to equipment owned by Windsor Company at December 31, 2020. Cost $9,720,000 Accumulated depreciation to date 1,080,000 Expected future net cash flows 7,560,000 Fair value 5,184,000 Assume that Windsor will continue to use this asset in the future. As of December 31, 2020, the equipment has a remaining useful life of 5 years. Your answer is partially correct. Try again. Prepare the journal entry (if any) to record the impairment of the asset...

On January 1, Year 1 Residence Company issued bonds with a $50,000 face value. The bonds...

On January 1, Year 1 Residence Company issued bonds with a $50,000 face value. The bonds were issued at 104 resulting in a 4% premium. They had a 20 year term and a stated rate of interest of 7% payable in cash on December 31 of each year. The company amortizes the premium on a straight-line basis. Assuming a straight line amortization of the premium, the journal entry necessary to recognize interest expense on the December 31, Year 1 is...

On January 1, Year 1 Residence Company issued bonds with a $50,000 face value. The bonds were issued at 104 resulting in a 4% premium. They had a 20 year term and a stated rate of interest of 7% payable in cash on December 31 of each year. The company amortizes the premium on a straight-line basis. Assuming a straight line amortization of the premium, the journal entry necessary to recognize interest expense on the December 31, Year 1 is...

What is the Supplies account balance at December 31 (Solve for x)? Supplies Available - January...

What is the Supplies account balance at December 31 (Solve for x)? Supplies Available - January 1 5,000 Supplies Purchased during the year 25,000 Total Supplies Available 30,000 Supplies Available - December 31 X Supplies Expense for the year 20,000 a. A debit balance of 50,000 b. A credit balance of 50,000 C. A debit balance of 10,000 d. A credit balance of 10,000

What is the Supplies account balance at December 31 (Solve for x)? Supplies Available - January 1 5,000 Supplies Purchased during the year 25,000 Total Supplies Available 30,000 Supplies Available - December 31 X Supplies Expense for the year 20,000 a. A debit balance of 50,000 b. A credit balance of 50,000 C. A debit balance of 10,000 d. A credit balance of 10,000

Sheridan Company has the following investments as of December 31, 2020: Investments in common stock of Laser Company Investment in debt securities of FourSquare Company $1,630,000 $3,240,000 In both investments, the carrying value and the fair value of these two investments are the same at December 31, 2020. Sheridan's stock investments does not result in significant influence on the operations of Laser Company. Sheridan's debt investment is considered held-to-maturity. At December 31, 2021, the shares in Laser Company are valued...

Sheridan Company has the following investments as of December 31, 2020: Investments in common stock of Laser Company Investment in debt securities of FourSquare Company $1,630,000 $3,240,000 In both investments, the carrying value and the fair value of these two investments are the same at December 31, 2020. Sheridan's stock investments does not result in significant influence on the operations of Laser Company. Sheridan's debt investment is considered held-to-maturity. At December 31, 2021, the shares in Laser Company are valued...

On January 1, 2017, Cullumber Company had a balance of $359,500

of goodwill on its balance sheet that resulted from the purchase of

a small business in a prior year. The goodwill had an indefinite

life. During 2017, the company had the following additional

transactions.

Jan.

2

Purchased a patent (7-year life) $313,950.

July

1

Acquired a 8-year franchise; expiration date July 1, 2,025,

$583,200.

Sept.

1

Research and development costs $176,500.

Make an entry as of December 31, 2017,...

On January 1, 2017, Cullumber Company had a balance of $359,500

of goodwill on its balance sheet that resulted from the purchase of

a small business in a prior year. The goodwill had an indefinite

life. During 2017, the company had the following additional

transactions.

Jan.

2

Purchased a patent (7-year life) $313,950.

July

1

Acquired a 8-year franchise; expiration date July 1, 2,025,

$583,200.

Sept.

1

Research and development costs $176,500.

Make an entry as of December 31, 2017,...

On January 1, 2017, Blossam Company had a balance of $38.000 at goodwill on its balance sheet that resulted from the purchase of a small business in a priorynar. The goodwill had an indefinitelt. During 2017, the company had the following additional transact Jan. 2 Purchased a patent 15 year life $204.550. July 1 Acquired a 9-year franchise: expiration date July 12.026, $626.400. Sept. 1 Roscarch and development costs $182,500. no entry is required, select "No Entry for the Prepare...

On January 1, 2017, Blossam Company had a balance of $38.000 at goodwill on its balance sheet that resulted from the purchase of a small business in a priorynar. The goodwill had an indefinitelt. During 2017, the company had the following additional transact Jan. 2 Purchased a patent 15 year life $204.550. July 1 Acquired a 9-year franchise: expiration date July 12.026, $626.400. Sept. 1 Roscarch and development costs $182,500. no entry is required, select "No Entry for the Prepare...

Presented below is information related to equipment owned by Whispering Company at December 31, 2020. Cost (residual value $0) Accumulated depreciation to date Value-in-use Fair value less cost of disposal $8,924,900 995,900 5.510,000 4,395,380 Assume that Whispering will continue to use this asset in the future. As of December 31, 2020, the equipment has a remaining useful life of 8 years. Whispering uses straight-line depreciation. la) Your answer is correct. Prepare the journal entry (if any) to record the impairment...

Presented below is information related to equipment owned by Whispering Company at December 31, 2020. Cost (residual value $0) Accumulated depreciation to date Value-in-use Fair value less cost of disposal $8,924,900 995,900 5.510,000 4,395,380 Assume that Whispering will continue to use this asset in the future. As of December 31, 2020, the equipment has a remaining useful life of 8 years. Whispering uses straight-line depreciation. la) Your answer is correct. Prepare the journal entry (if any) to record the impairment...

Exercise 11-16 Presented below is information related to equipment owned by Windsor Company at December 31, 2020. Cost $9,720,000 Accumulated depreciation to date 1,080,000 Expected future net cash flows 7,560,000 Fair value 5,184,000 Assume that Windsor will continue to use this asset in the future. As of December 31, 2020, the equipment has a remaining useful life of 5 years. Your answer is partially correct. Try again. Prepare the journal entry (if any) to record the impairment of the asset...

Exercise 11-16 Presented below is information related to equipment owned by Windsor Company at December 31, 2020. Cost $9,720,000 Accumulated depreciation to date 1,080,000 Expected future net cash flows 7,560,000 Fair value 5,184,000 Assume that Windsor will continue to use this asset in the future. As of December 31, 2020, the equipment has a remaining useful life of 5 years. Your answer is partially correct. Try again. Prepare the journal entry (if any) to record the impairment of the asset...

On January 1, Year 1 Residence Company issued bonds with a $50,000 face value. The bonds were issued at 104 resulting in a 4% premium. They had a 20 year term and a stated rate of interest of 7% payable in cash on December 31 of each year. The company amortizes the premium on a straight-line basis. Assuming a straight line amortization of the premium, the journal entry necessary to recognize interest expense on the December 31, Year 1 is...

On January 1, Year 1 Residence Company issued bonds with a $50,000 face value. The bonds were issued at 104 resulting in a 4% premium. They had a 20 year term and a stated rate of interest of 7% payable in cash on December 31 of each year. The company amortizes the premium on a straight-line basis. Assuming a straight line amortization of the premium, the journal entry necessary to recognize interest expense on the December 31, Year 1 is...

What is the Supplies account balance at December 31 (Solve for x)? Supplies Available - January 1 5,000 Supplies Purchased during the year 25,000 Total Supplies Available 30,000 Supplies Available - December 31 X Supplies Expense for the year 20,000 a. A debit balance of 50,000 b. A credit balance of 50,000 C. A debit balance of 10,000 d. A credit balance of 10,000

What is the Supplies account balance at December 31 (Solve for x)? Supplies Available - January 1 5,000 Supplies Purchased during the year 25,000 Total Supplies Available 30,000 Supplies Available - December 31 X Supplies Expense for the year 20,000 a. A debit balance of 50,000 b. A credit balance of 50,000 C. A debit balance of 10,000 d. A credit balance of 10,000

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago