How do you calculate the sample mean excess return of the risk free rate ? (possibly...

How do you calculate the sample mean excess return of the risk free rate ? (possibly with excel)

Homework Answers

Step :- 1

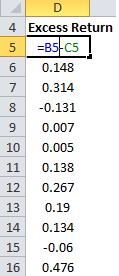

First of all enter the data of the rerunron the security over the years in column.

Step :- 2

Then in next column enter the risk free interest rate data.

Step :- 3

Then in the next column, subtract the risk free returns from the returns on our security. This will called Excess Return.

Step :- 4

- Now let's calculat the excess return. In the above sheet it will be calculate by the =AVERAGE (D15:D16).

- calculate the standard deviations of the Excess Return. For above example it will be =STDEV(D5:D16)

- Finally calculate the sharpe's ratio by the dividing the average excess return by the standard deviations of the same. In our example the formula will be =D18/D19

Thanks for posting.....

i hope my efforts will be fruitful to you...?

Add Answer to:

How do you calculate the sample mean excess return of the risk

free rate ? (possibly...

CAPM: The risk-free rate is 2%, Beta=1.6 and return to the market is 5% Calculate excess...

CAPM: The risk-free rate is 2%, Beta=1.6 and return to the market is 5% Calculate excess return to the market Calculate the required return on equity What does a lower number mean vs a higher return on equity? No spreadsheet, worked out

Suppose that the average excess return on stocks is 12.00% and that the risk-free interest rate...

Suppose that the average excess return on stocks is 12.00% and that the risk-free interest rate is 3.00%. Compute expected returns to stocks with each of the following beta coefficients using the capital asset pricing model (CAPM): Hint: Do not forget to enter the minus sign if the value of the return to stock is negative.) Return to Stocks (%) 0.7 0.2 1.0 2.0 Based on the CAPM and your calculations for the return to stocks, what does it mean...

Suppose that the average excess return on stocks is 12.00% and that the risk-free interest rate is 3.00%. Compute expected returns to stocks with each of the following beta coefficients using the capital asset pricing model (CAPM): Hint: Do not forget to enter the minus sign if the value of the return to stock is negative.) Return to Stocks (%) 0.7 0.2 1.0 2.0 Based on the CAPM and your calculations for the return to stocks, what does it mean...

The risk-free rate is 3% and you believe that the S&P 500's excess return will be...

The risk-free rate is 3% and you believe that the S&P 500's excess return will be 10.6% over the next year. If you invest in a stock with a beta of 1.1 (and a standard deviation of 30%), what is your best guess as to its expected excess return over the next year? The expected excess return over the next year is? (Round to two decimal places.)

A corporate bond has an expected, total (not excess) return of 5%. The risk-free rate is...

A corporate bond has an expected, total (not excess) return of 5%. The risk-free rate is 2% and the expected market return (total, not excess) is 10%. Which of the following is closest to the beta of the corporate bond?

The risk free rate is 7%, the return in the market is 10%, and the beta...

The risk free rate is 7%, the return in the market is 10%, and the beta is 1.30. What return must you receive to be satisfied that you are being fairly ]for the risk of the firm? Using excel to solve

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate...

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 7%, and the market’s average return was 14%. Performance

is measured using an index model regression on excess returns.

Consider the two excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 7%, and the market's average return was 14%. Performance is measured using an index model regression on excess returns Stock A...

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 7%, and the market’s average return was 14%. Performance

is measured using an index model regression on excess returns.

Consider the two excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 7%, and the market's average return was 14%. Performance is measured using an index model regression on excess returns Stock A...

Given that the risk-free rate is 5%, the expected return on the market portfolio is 20%,...

Given that the risk-free rate is 5%, the expected return on the market portfolio is 20%, and the standard deviation of returns to the market portfolio is 20%, answer the following questions: c. Now suppose that you want to have a portfolio, which pays 25% expected return. What is the weight in the risk free asset and in the market portfolio? d. What do these weights mean: What are you doing with the risk free asset and what are you...

TOISRULIUSS. Expected Return = Risk free Rate + beta (expected market return - risk free rate)...

TOISRULIUSS. Expected Return = Risk free Rate + beta (expected market return - risk free rate) .04 +0.80.09 - .04) = .08 = 8.0% 3. Suppose the MiniCD Corporation's common stock has a return of 12%. Assume the risk- free rate is 4%, the expected market return is 9%, and no unsystematic influence affected Mini's return. The beta for MiniCD is:

TOISRULIUSS. Expected Return = Risk free Rate + beta (expected market return - risk free rate) .04 +0.80.09 - .04) = .08 = 8.0% 3. Suppose the MiniCD Corporation's common stock has a return of 12%. Assume the risk- free rate is 4%, the expected market return is 9%, and no unsystematic influence affected Mini's return. The beta for MiniCD is:

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate...

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 7%, and the market’s average return was 14%. Performance is measured using an index model regression on excess returns. Stock A Stock B Index model regression estimates 1% + 1.2(rM − rf) 2% + 0.8(rM − rf) R-square 0.635 0.466 Residual standard deviation, σ(e) 11.3% 20.1% Standard deviation of excess returns 22.6% 26.9% a. Calculate the following statistics for each...

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate...

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 5%, and the market’s average return was 12%. Performance is measured using an index model regression on excess returns. Stock A Stock B Index model regression estimates 1% + 1.2(rM − rf) 2% + 0.8(rM − rf) R-square 0.599 0.448 Residual standard deviation, σ(e) 10.7% 19.5% Standard deviation of excess returns 22% 25.7% a. Calculate the following statistics for each...

Suppose that the average excess return on stocks is 12.00% and that the risk-free interest rate is 3.00%. Compute expected returns to stocks with each of the following beta coefficients using the capital asset pricing model (CAPM): Hint: Do not forget to enter the minus sign if the value of the return to stock is negative.) Return to Stocks (%) 0.7 0.2 1.0 2.0 Based on the CAPM and your calculations for the return to stocks, what does it mean...

Suppose that the average excess return on stocks is 12.00% and that the risk-free interest rate is 3.00%. Compute expected returns to stocks with each of the following beta coefficients using the capital asset pricing model (CAPM): Hint: Do not forget to enter the minus sign if the value of the return to stock is negative.) Return to Stocks (%) 0.7 0.2 1.0 2.0 Based on the CAPM and your calculations for the return to stocks, what does it mean...

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 7%, and the market’s average return was 14%. Performance

is measured using an index model regression on excess returns.

Consider the two excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 7%, and the market's average return was 14%. Performance is measured using an index model regression on excess returns Stock A...

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 7%, and the market’s average return was 14%. Performance

is measured using an index model regression on excess returns.

Consider the two excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 7%, and the market's average return was 14%. Performance is measured using an index model regression on excess returns Stock A...

TOISRULIUSS. Expected Return = Risk free Rate + beta (expected market return - risk free rate) .04 +0.80.09 - .04) = .08 = 8.0% 3. Suppose the MiniCD Corporation's common stock has a return of 12%. Assume the risk- free rate is 4%, the expected market return is 9%, and no unsystematic influence affected Mini's return. The beta for MiniCD is:

TOISRULIUSS. Expected Return = Risk free Rate + beta (expected market return - risk free rate) .04 +0.80.09 - .04) = .08 = 8.0% 3. Suppose the MiniCD Corporation's common stock has a return of 12%. Assume the risk- free rate is 4%, the expected market return is 9%, and no unsystematic influence affected Mini's return. The beta for MiniCD is:

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago