I have to do this in Excel. Please Provide the formulas step by

step and a screenshoot of output how it looks in the end.

Question is about the MARKET vs the CONTRACTUAL value of a loan,

BUT taking it in monthly terms.

Homework Answers

Given that

| Original Principal | 35000 |

| Loan term (Years) | 4 |

| Payments Per Year | 12 |

| Total number of Payments | 48 |

| Annual Interest Rate | 3.75% |

| Monthly Payment | 786.36 |

| Month | Payment | Interest | Principal | Balance |

| 0 | 35000 | |||

| 1 | 786.36 | 109.38 | 676.98 | 34323.02 |

| 2 | 786.36 | 107.26 | 679.10 | 33643.92 |

| 3 | 786.36 | 105.14 | 681.22 | 32962.70 |

| 4 | 786.36 | 103.01 | 683.35 | 32279.35 |

| 5 | 786.36 | 100.87 | 685.48 | 31593.87 |

| 6 | 786.36 | 98.73 | 687.63 | 30906.24 |

| 7 | 786.36 | 96.58 | 689.78 | 30216.46 |

| 8 | 786.36 | 94.43 | 691.93 | 29524.53 |

| 9 | 786.36 | 92.26 | 694.09 | 28830.44 |

| 10 | 786.36 | 90.10 | 696.26 | 28134.18 |

| 11 | 786.36 | 87.92 | 698.44 | 27435.74 |

| 12 | 786.36 | 85.74 | 700.62 | 26735.12 |

| 13 | 786.36 | 83.55 | 702.81 | 26032.31 |

| 14 | 786.36 | 81.35 | 705.01 | 25327.30 |

| 15 | 786.36 | 79.15 | 707.21 | 24620.09 |

| 16 | 786.36 | 76.94 | 709.42 | 23910.67 |

| 17 | 786.36 | 74.72 | 711.64 | 23199.04 |

| 18 | 786.36 | 72.50 | 713.86 | 22485.18 |

| 19 | 786.36 | 70.27 | 716.09 | 21769.08 |

| 20 | 786.36 | 68.03 | 718.33 | 21050.75 |

| 21 | 786.36 | 65.78 | 720.57 | 20330.18 |

| 22 | 786.36 | 63.53 | 722.83 | 19607.36 |

| 23 | 786.36 | 61.27 | 725.08 | 18882.27 |

| 24 | 786.36 | 59.01 | 727.35 | 18154.92 |

| 25 | 786.36 | 56.73 | 729.62 | 17425.30 |

| 26 | 786.36 | 54.45 | 731.90 | 16693.39 |

| 27 | 786.36 | 52.17 | 734.19 | 15959.20 |

| 28 | 786.36 | 49.87 | 736.48 | 15222.72 |

| 29 | 786.36 | 47.57 | 738.79 | 14483.93 |

| 30 | 786.36 | 45.26 | 741.10 | 13742.84 |

| 31 | 786.36 | 42.95 | 743.41 | 12999.43 |

| 32 | 786.36 | 40.62 | 745.73 | 12253.69 |

| 33 | 786.36 | 38.29 | 748.06 | 11505.63 |

| 34 | 786.36 | 35.96 | 750.40 | 10755.22 |

| 35 | 786.36 | 33.61 | 752.75 | 10002.48 |

| 36 | 786.36 | 31.26 | 755.10 | 9247.38 |

| 37 | 786.36 | 28.90 | 757.46 | 8489.92 |

| 38 | 786.36 | 26.53 | 759.83 | 7730.09 |

| 39 | 786.36 | 24.16 | 762.20 | 6967.89 |

| 40 | 786.36 | 21.77 | 764.58 | 6203.31 |

| 41 | 786.36 | 19.39 | 766.97 | 5436.34 |

| 42 | 786.36 | 16.99 | 769.37 | 4666.97 |

| 43 | 786.36 | 14.58 | 771.77 | 3895.19 |

| 44 | 786.36 | 12.17 | 774.18 | 3121.01 |

| 45 | 786.36 | 9.75 | 776.60 | 2344.40 |

| 46 | 786.36 | 7.33 | 779.03 | 1565.37 |

| 47 | 786.36 | 4.89 | 781.47 | 783.91 |

| 48 | 786.36 | 2.45 | 783.91 | 0.00 |

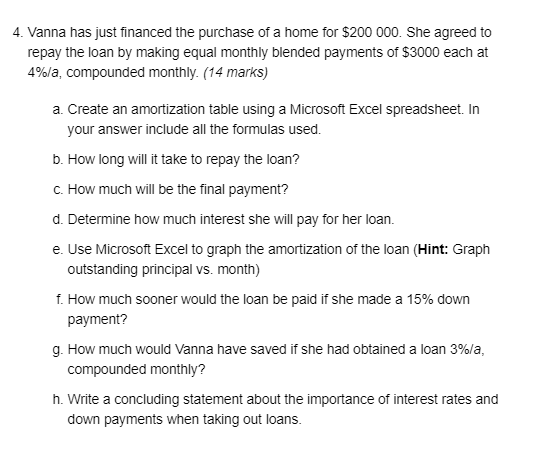

Here is the screenshot of my workings in excel.

![D12 IPMT($B$6/$B$4,B12,$B$5,-$F$11]) 2 Original Principal 3 Loan term (Years) 4 Payments Per Year 5 Total number of Payments 6 Annual Interest Rate 7 Payment 35000 12 48 3.75% 786.36 Month Payment Interest Principa alance 0 10 35000 676.98 34323.02 679.1033643.92 681.22 32962.70 683.35 32279.35 685.48 31593.87 687.63 30906.24 689.78 30216.46 691.93 29524.53 694.09 28830.44 696.26 28134.18 698.44 27435.74 700.62 26735.12 702.81 26032.31 705.0125327.30 707.21 24620.09 709.42 23910.67 1 786.36 109.38 12 13 14 15 16 17 18 19 20 21 2786.36 107 3 786.36105 4 786.36 5786.36 6 786.36 7 786.36 8786.36 9786.36 10 786.36 11786.36 12786.36 13786.36 14 786.36 15786.36 16786.36 103.01 100.87 98.73 96.58 94.43 92.26 90.10 87.92 85.74 83.55 81.35 79.15 76.94 23 24 25 26 27](http://img.homeworklib.com/questions/f23a6720-71a6-11ea-ad3d-bd555c2d0ef8.png?x-oss-process=image/resize,w_560)

For Calculating the monthly loan payment amount, use the formula

|

B6/B4 is the monthly interest rate ; B5 is the number of payments to be made as per the loan contract; -B2 is the loan amount. As we do not want negative figures and the PMT formula calculates 'the payments', the figures will show in negative if we don't use the 'minus'. |

For Calculating Interest payments,

| =IPMT($B$6/$B$4,B12,$B$5,-$F$11) |

This formula is used for interest payment calculations, where $B$6/$B$4 is the monthly interest rate (as we are copying the formula down, we need to freeze the constant cells, hence $ is used) ; B12 is the nth number of interest payment for which we calculate the interest payment (so, for first month, its B12, second month - B13, and so on. $B$5 is the total number of payments to be made as per loan contract. -$F$11 is again the loan amount. Please note that we are freezing this amount as the IPMT gives us the interest amount of the nth month. It doesn't want to know the last loan balance outstanding. |

Principal amount can be calculated simply by applying (Monthly payment - Interest) because whatever is remaining after the interest component is the principal component of the monthly payment.

So, Principal for first month = C12-D12

Or you can calculate Principal amount paid each month using the PPMT formula, similar to the IPMT formula as demonstrated above.

| =PPMT($B$6/$B$4,B12,$B$5,-$F$11) |

For the balance, the formula is again very simple. It is equal to Previous Balance minus Monthly Payment. So, for the first month, it is =F11-E12

After applying the formula for first month, you can safely copy it till the 48th month to get the loan repayment schedule.

______________________________________________________________________________

If you want to repurchase the loan at the 19th Month, you will have to make the payment of Balance outstanding at the 18th month plus the prepayment penalties, if the bank charges such penalties as per the loan contract. (ie. $22,485.18 + prepayment penalties)

Add Answer to:

I have to do this in Excel. Please Provide the formulas step by

step and a...

I have to do this in Excel. Please Provide the formulas step by step and a...

I have to do this in Excel. Please Provide the formulas step by

step and a screenshoot of output how it looks in the end.

Thank you.

Question is about the MARKET vs the CONTRACTUAL value of a loan

with refinancing, and cost of a loan and cost of refinancing in

terms of points. Has to be in monthly terms.

You want to buy a house of a million dollars, and the bank is giving you a loan with 1.5...

I have to do this in Excel. Please Provide the formulas step by

step and a screenshoot of output how it looks in the end.

Thank you.

Question is about the MARKET vs the CONTRACTUAL value of a loan

with refinancing, and cost of a loan and cost of refinancing in

terms of points. Has to be in monthly terms.

You want to buy a house of a million dollars, and the bank is giving you a loan with 1.5...

Attached is the excel. The solutions are already there. I just need the function formulas to...

Attached is the excel. The solutions are already there. I just

need the function formulas to put in the box to get that answer. If

you could just Put exactly what you put in the function box to get

these solutions ! Also answer the brief question at the bottom of

each question

?? Josh Cordova?-D AutoSave ! ? : Book2 Excel File Home Insert Draw Page LayoutFormulasData Review View Help Power Pvot Tell me what you want to do...

Attached is the excel. The solutions are already there. I just

need the function formulas to put in the box to get that answer. If

you could just Put exactly what you put in the function box to get

these solutions ! Also answer the brief question at the bottom of

each question

?? Josh Cordova?-D AutoSave ! ? : Book2 Excel File Home Insert Draw Page LayoutFormulasData Review View Help Power Pvot Tell me what you want to do...

Vanna has just financed the purchase of a home for $200 000. She agreed to repay the loan by making equal monthly blended payments of $3000 each at 4%/a, compounded monthly. (14 marks) Create an amortization table using a Microsoft Excel spreadsheet. In y

Vanna has just financed the purchase of a home for $200 000. She agreed to repay the loan by making equal monthly blended payments of $3000 each at 4%/a, compounded monthly. a. Create an amortization table using a Microsoft Excel spreadsheet. In your answer include all the formulas used.b.How long will it take to repay the loan?c. How much will be the final payment?d. Determine how much interest she will pay for her loan.e. Use Microsoft Excel to graph the amortization...

Vanna has just financed the purchase of a home for $200 000. She agreed to repay the loan by making equal monthly blended payments of $3000 each at 4%/a, compounded monthly. a. Create an amortization table using a Microsoft Excel spreadsheet. In your answer include all the formulas used.b.How long will it take to repay the loan?c. How much will be the final payment?d. Determine how much interest she will pay for her loan.e. Use Microsoft Excel to graph the amortization...

please no stupid indian excel answers, please explain step by step how to answer this with...

please no stupid indian excel answers, please explain

step by step how to answer this with explanations thank you and

again i remind no stupid indian who thinks they are the smartedt in

the world with financial calculqtors thank you

You are considering buying a new home. You will need to borrow 350,000 to purchase the home. A mortga t 9% (as an APR with monthly compounding). If you borrow the money from this mortgage company, your monthly payment wilkbe...

please no stupid indian excel answers, please explain

step by step how to answer this with explanations thank you and

again i remind no stupid indian who thinks they are the smartedt in

the world with financial calculqtors thank you

You are considering buying a new home. You will need to borrow 350,000 to purchase the home. A mortga t 9% (as an APR with monthly compounding). If you borrow the money from this mortgage company, your monthly payment wilkbe...

should be explain it on excel Solve all of the following problems with Excel. Please use formulas in excel to solve. (2) (10 pts) (a) Assume monthly car payments of $500 per month for 4 years and...

should be explain it on excel

Solve all of the following problems with Excel. Please use formulas in excel to solve. (2) (10 pts) (a) Assume monthly car payments of $500 per month for 4 years and an interest rate of 0.75% per month. 1. What initial principal will this repay? (b) Assume annual car payments of $6000 for 4 years and an interest rate of 9% per year. 1. What initial principal will this repay? (c) Assume monthly car...

should be explain it on excel

Solve all of the following problems with Excel. Please use formulas in excel to solve. (2) (10 pts) (a) Assume monthly car payments of $500 per month for 4 years and an interest rate of 0.75% per month. 1. What initial principal will this repay? (b) Assume annual car payments of $6000 for 4 years and an interest rate of 9% per year. 1. What initial principal will this repay? (c) Assume monthly car...

Show all excel formulas used Ex. 3 JIf a dealer offers you a car at $275...

Show all excel formulas used

Ex. 3 JIf a dealer offers you a car at $275 monthly payment for 5 years plus $5,000 down. If you can get a similar loan from a bank at APR of 12%, what is the price that you're paying? Down payment Monthly payment Loan period months APR No. of compounding times per year Monthly rate Present Value Book formula Excel function Ex. 4 If you take out an $10,000 car loan that call for...

Show all excel formulas used

Ex. 3 JIf a dealer offers you a car at $275 monthly payment for 5 years plus $5,000 down. If you can get a similar loan from a bank at APR of 12%, what is the price that you're paying? Down payment Monthly payment Loan period months APR No. of compounding times per year Monthly rate Present Value Book formula Excel function Ex. 4 If you take out an $10,000 car loan that call for...

PLEASE EXPLAIN HOW TO CREATE THE AMORTIZATION TABLE IN EXCEL! Mini-Project 1: Mortgage Loan Analysis (50...

PLEASE EXPLAIN HOW TO CREATE THE AMORTIZATION TABLE IN EXCEL! Mini-Project 1: Mortgage Loan Analysis (50 points): You plan to buy a house in December 2019. The sale price is $385,000. You need to pay 20% down payments and borrow additional 80% from Bank of America with a 25-year, 3.0% fixed-rate mortgage loan. You are expected to pay an equal MONTHLY payment starting from January 2020 for a total of 25 years. (1) Calculate your expected monthly mortgage payment. (2)...

Please show your work with the formulas written out. Please answer as if you can not...

Please show your work with the formulas written out. Please answer as if you can not use a calculator, or only use a four function calculator (because that is how I have to learn it). Do not just put down the calculator keystrokes I need to see every step and number to learn how to do it. 17. If you borrow $25000 and repay $800 monthly at a rate of 6%, how many months will it take to repay the...

Solve all of the following problems with Excel. Please use formulas in excel to solve. (2) (a) Assume monthly car payments of $500 per month for 4 years and an interest rate of 0.75% per month. 1. Wha...

Solve all of the following problems with Excel. Please use formulas in excel to solve. (2) (a) Assume monthly car payments of $500 per month for 4 years and an interest rate of 0.75% per month. 1. What initial principal will this repay? (b) Assume annual car payments of $6000 for 4 years and an interest rate of 9% per year. 1. What initial principal will this repay? (c) Assume monthly car payments of $500 per month for 4 years...

Please provide the formulas for excel as well Excel File Edit View Insert Format Tools Data...

Please provide the formulas

for excel as well

Excel File Edit View Insert Format Tools Data Window Hel ACFI 385 Excel Project Winter 2019(1) (2).xlsx 1 00% ▼ |Search in Sheet Home Layout Tables Charts SmartArt Formulas Data Review Edit Font Aignme Fill ▼ Verdana Wrap TextCeneral Good Conditional Check Cell Insert Delete Format Themes Aa 41 ; * O ( Analyze the following scenarios that will require you to compute either the present value, future value, and/or the a...

Please provide the formulas

for excel as well

Excel File Edit View Insert Format Tools Data Window Hel ACFI 385 Excel Project Winter 2019(1) (2).xlsx 1 00% ▼ |Search in Sheet Home Layout Tables Charts SmartArt Formulas Data Review Edit Font Aignme Fill ▼ Verdana Wrap TextCeneral Good Conditional Check Cell Insert Delete Format Themes Aa 41 ; * O ( Analyze the following scenarios that will require you to compute either the present value, future value, and/or the a...

I have to do this in Excel. Please Provide the formulas step by

step and a screenshoot of output how it looks in the end.

Thank you.

Question is about the MARKET vs the CONTRACTUAL value of a loan

with refinancing, and cost of a loan and cost of refinancing in

terms of points. Has to be in monthly terms.

You want to buy a house of a million dollars, and the bank is giving you a loan with 1.5...

I have to do this in Excel. Please Provide the formulas step by

step and a screenshoot of output how it looks in the end.

Thank you.

Question is about the MARKET vs the CONTRACTUAL value of a loan

with refinancing, and cost of a loan and cost of refinancing in

terms of points. Has to be in monthly terms.

You want to buy a house of a million dollars, and the bank is giving you a loan with 1.5...

Attached is the excel. The solutions are already there. I just

need the function formulas to put in the box to get that answer. If

you could just Put exactly what you put in the function box to get

these solutions ! Also answer the brief question at the bottom of

each question

?? Josh Cordova?-D AutoSave ! ? : Book2 Excel File Home Insert Draw Page LayoutFormulasData Review View Help Power Pvot Tell me what you want to do...

Attached is the excel. The solutions are already there. I just

need the function formulas to put in the box to get that answer. If

you could just Put exactly what you put in the function box to get

these solutions ! Also answer the brief question at the bottom of

each question

?? Josh Cordova?-D AutoSave ! ? : Book2 Excel File Home Insert Draw Page LayoutFormulasData Review View Help Power Pvot Tell me what you want to do...

please no stupid indian excel answers, please explain

step by step how to answer this with explanations thank you and

again i remind no stupid indian who thinks they are the smartedt in

the world with financial calculqtors thank you

You are considering buying a new home. You will need to borrow 350,000 to purchase the home. A mortga t 9% (as an APR with monthly compounding). If you borrow the money from this mortgage company, your monthly payment wilkbe...

please no stupid indian excel answers, please explain

step by step how to answer this with explanations thank you and

again i remind no stupid indian who thinks they are the smartedt in

the world with financial calculqtors thank you

You are considering buying a new home. You will need to borrow 350,000 to purchase the home. A mortga t 9% (as an APR with monthly compounding). If you borrow the money from this mortgage company, your monthly payment wilkbe...

should be explain it on excel

Solve all of the following problems with Excel. Please use formulas in excel to solve. (2) (10 pts) (a) Assume monthly car payments of $500 per month for 4 years and an interest rate of 0.75% per month. 1. What initial principal will this repay? (b) Assume annual car payments of $6000 for 4 years and an interest rate of 9% per year. 1. What initial principal will this repay? (c) Assume monthly car...

should be explain it on excel

Solve all of the following problems with Excel. Please use formulas in excel to solve. (2) (10 pts) (a) Assume monthly car payments of $500 per month for 4 years and an interest rate of 0.75% per month. 1. What initial principal will this repay? (b) Assume annual car payments of $6000 for 4 years and an interest rate of 9% per year. 1. What initial principal will this repay? (c) Assume monthly car...

Show all excel formulas used

Ex. 3 JIf a dealer offers you a car at $275 monthly payment for 5 years plus $5,000 down. If you can get a similar loan from a bank at APR of 12%, what is the price that you're paying? Down payment Monthly payment Loan period months APR No. of compounding times per year Monthly rate Present Value Book formula Excel function Ex. 4 If you take out an $10,000 car loan that call for...

Show all excel formulas used

Ex. 3 JIf a dealer offers you a car at $275 monthly payment for 5 years plus $5,000 down. If you can get a similar loan from a bank at APR of 12%, what is the price that you're paying? Down payment Monthly payment Loan period months APR No. of compounding times per year Monthly rate Present Value Book formula Excel function Ex. 4 If you take out an $10,000 car loan that call for...

Please provide the formulas

for excel as well

Excel File Edit View Insert Format Tools Data Window Hel ACFI 385 Excel Project Winter 2019(1) (2).xlsx 1 00% ▼ |Search in Sheet Home Layout Tables Charts SmartArt Formulas Data Review Edit Font Aignme Fill ▼ Verdana Wrap TextCeneral Good Conditional Check Cell Insert Delete Format Themes Aa 41 ; * O ( Analyze the following scenarios that will require you to compute either the present value, future value, and/or the a...

Please provide the formulas

for excel as well

Excel File Edit View Insert Format Tools Data Window Hel ACFI 385 Excel Project Winter 2019(1) (2).xlsx 1 00% ▼ |Search in Sheet Home Layout Tables Charts SmartArt Formulas Data Review Edit Font Aignme Fill ▼ Verdana Wrap TextCeneral Good Conditional Check Cell Insert Delete Format Themes Aa 41 ; * O ( Analyze the following scenarios that will require you to compute either the present value, future value, and/or the a...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago