dear instructor, i hope this message find you well, this is a question in Advance Accounting about consolidating the financial statements of two companies, thank you for your help

Homework Answers

Add Answer to:

dear instructor, i hope this message find you

well, this is a

question in Advance Accounting...

need help... please fix the errors as soon as possible. Thanks in advance! Pushdown Accounting Assume...

need help... please fix the errors as soon as possible. Thanks

in advance!

Pushdown Accounting Assume a parent company acquires its subsidiary by paying $1,200,000 for all of the outstanding voting shares of the investee. On the acquisition date, subsidiary's assets and liabilities have individual fair values that equal their book values, except for property equipment with a fair value greater than book value by $150,000 and license with a fair value greater than book value by $250,000. The parent...

need help... please fix the errors as soon as possible. Thanks

in advance!

Pushdown Accounting Assume a parent company acquires its subsidiary by paying $1,200,000 for all of the outstanding voting shares of the investee. On the acquisition date, subsidiary's assets and liabilities have individual fair values that equal their book values, except for property equipment with a fair value greater than book value by $150,000 and license with a fair value greater than book value by $250,000. The parent...

Required: 1. Prepare the con are the consolidation and equity accounting entries for the year eaded...

Required: 1. Prepare the con are the consolidation and equity accounting entries for the year eaded 31 December 20x5 with narratives and workings). m analytical checks on the following balances as at 31 December 2015 2 Perform analytics (a) Non-controlling interests and (b) Investment in associate. P6.8 Comprehensive problem set P Co acquired a 90% OW quired a 90% ownership interest in Y Co on 1 January 20x3. At the date of acquisition, the share Joy Co was $1,000,000, and...

Required: 1. Prepare the con are the consolidation and equity accounting entries for the year eaded 31 December 20x5 with narratives and workings). m analytical checks on the following balances as at 31 December 2015 2 Perform analytics (a) Non-controlling interests and (b) Investment in associate. P6.8 Comprehensive problem set P Co acquired a 90% OW quired a 90% ownership interest in Y Co on 1 January 20x3. At the date of acquisition, the share Joy Co was $1,000,000, and...

IFRS 3 outlines the accounting requirements for business combinations. Which of the following statements is correct?...

IFRS 3 outlines the accounting requirements for business combinations. Which of the following statements is correct? Multiple Choice The new entity method can only be used when cash is the sole consideration offered by the acquirer in a business combination. The only acceptable method of accounting for business combinations is the new entity method. Companies may choose between the new entity method and the acquisition method when accounting for business combinations. The only acceptable method of accounting for business combinations...

need help asap... please fix the errors asap Pushdown Accounting Assume a parent company acquires its...

need help asap... please fix the errors asap

Pushdown Accounting Assume a parent company acquires its subsidiary by paying $1,200,000 for all of the outstanding voting shares of the investee. On the acquisition date, subsidiary's assets and liabilities have individual fair values that equal their book values, except for property equipment with a fair value greater than book value by $150,000 and license with a fair value greater than book value by $250,000. The parent and subsidiary have the following...

need help asap... please fix the errors asap

Pushdown Accounting Assume a parent company acquires its subsidiary by paying $1,200,000 for all of the outstanding voting shares of the investee. On the acquisition date, subsidiary's assets and liabilities have individual fair values that equal their book values, except for property equipment with a fair value greater than book value by $150,000 and license with a fair value greater than book value by $250,000. The parent and subsidiary have the following...

tion Equity method ging 59.000 Shares of $30 per share, for e the consolidation LOZ luc...

tion Equity method ging 59.000 Shares of $30 per share, for e the consolidation LOZ luc Com shares of the first year. individual net values that equaled 00 (depreciation auisition date, allowing: PPE assets inte sot that has a fair value o 320,000 (amor c. Prepare the consolid d. Explain why the (ADJ) consolidating enllyn 48. Consolidation at the end of the first year subsequent to date of acquisition- Assume the parent company acquires its subsidiary on January 1, 2019....

tion Equity method ging 59.000 Shares of $30 per share, for e the consolidation LOZ luc Com shares of the first year. individual net values that equaled 00 (depreciation auisition date, allowing: PPE assets inte sot that has a fair value o 320,000 (amor c. Prepare the consolid d. Explain why the (ADJ) consolidating enllyn 48. Consolidation at the end of the first year subsequent to date of acquisition- Assume the parent company acquires its subsidiary on January 1, 2019....

Corporations on January 1, 2017, just before they entered into a business combination: 13 The following...

Corporations on January 1, 2017, just before they entered into a business combination: 13 The following Statement of Financial Position were prepared for Red and Blue So Problem 13-6 Blue Corporation Fair Value P 50,000 245,000 250,000 Items Cash and Receivables Inventory Buildings and Equipment Less: Accumulated Depreciation Total Assets Red Corporation Book Value Fair value Book Value P 300,000 P 300,000 P 50,000 400,000 600,000 100,000 800,000 870,000 300,000 ( 200,000) ( 150,000) P1,300,000 P1,770,000 P300,000 P545,000 P 100,000...

Corporations on January 1, 2017, just before they entered into a business combination: 13 The following Statement of Financial Position were prepared for Red and Blue So Problem 13-6 Blue Corporation Fair Value P 50,000 245,000 250,000 Items Cash and Receivables Inventory Buildings and Equipment Less: Accumulated Depreciation Total Assets Red Corporation Book Value Fair value Book Value P 300,000 P 300,000 P 50,000 400,000 600,000 100,000 800,000 870,000 300,000 ( 200,000) ( 150,000) P1,300,000 P1,770,000 P300,000 P545,000 P 100,000...

Parent Co paid $176,000 for 80% of the outstanding voting stock of Sub Co on January...

Parent Co paid $176,000 for 80% of the outstanding voting stock

of Sub Co on January 1, 2018, when Sub Co’s stockholders’ equity

consisted of $120,000 common stock and $60,000 retained earnings.

This implied that the total fair value of Sub co is $220,000

($176,000 / 80%). The company assigned the $40,000 excess fair

value to previously unrecorded patents with a 10-year useful

life.

Parent Co’s $36,800 income from Sub Co for 2018 consisted of 80%

of Sub Co’s $50,000...

Parent Co paid $176,000 for 80% of the outstanding voting stock

of Sub Co on January 1, 2018, when Sub Co’s stockholders’ equity

consisted of $120,000 common stock and $60,000 retained earnings.

This implied that the total fair value of Sub co is $220,000

($176,000 / 80%). The company assigned the $40,000 excess fair

value to previously unrecorded patents with a 10-year useful

life.

Parent Co’s $36,800 income from Sub Co for 2018 consisted of 80%

of Sub Co’s $50,000...

Question 2 Parent Ltd acquired 60% of the equity in Sub Ltd on 1 April 2014...

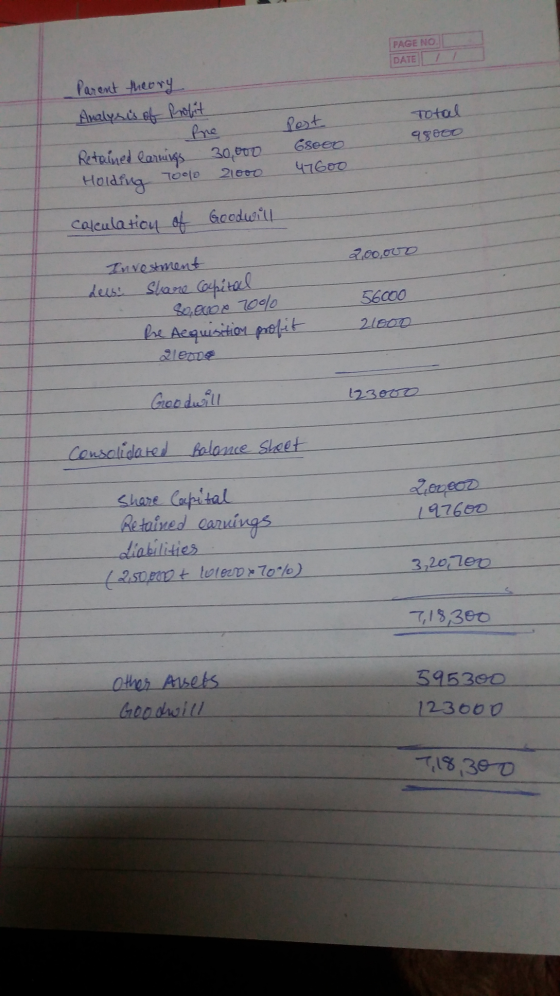

Question 2 Parent Ltd acquired 60% of the equity in Sub Ltd on 1 April 2014 for $1 200 000. At that date, the equity of Sub Ltd comprised share capital of $600 000 and retained earnings of $340 000 Because Sub Ltd used the cost model for its recognised property, plant, and equipment, it had several items whose book value was lower than fair value at the date of acquisition. The book values and the fair values of these...

Question 2 Parent Ltd acquired 60% of the equity in Sub Ltd on 1 April 2014 for $1 200 000. At that date, the equity of Sub Ltd comprised share capital of $600 000 and retained earnings of $340 000 Because Sub Ltd used the cost model for its recognised property, plant, and equipment, it had several items whose book value was lower than fair value at the date of acquisition. The book values and the fair values of these...

Prepare cosolidated fin. statement P acquired 75% of the shares in S on 1 January 2007...

Prepare cosolidated fin. statement

P acquired 75% of the shares in S on 1 January 2007 when S had retained earnings of $15,000. The market price of S's shares just before the date of acquisition was $1.60. P values non-controlling interest at fair value. Goodwill is not impaired. The statements of financial position of P and S at 31 December 20X7 were: 60,000 50,000 Property, plant and equipment Shares in S 68,000_ 128,000 50,000 52.000 35,000 180,000 85,000 100,000 50,000...

Prepare cosolidated fin. statement

P acquired 75% of the shares in S on 1 January 2007 when S had retained earnings of $15,000. The market price of S's shares just before the date of acquisition was $1.60. P values non-controlling interest at fair value. Goodwill is not impaired. The statements of financial position of P and S at 31 December 20X7 were: 60,000 50,000 Property, plant and equipment Shares in S 68,000_ 128,000 50,000 52.000 35,000 180,000 85,000 100,000 50,000...

On January 2, 20X7, Victory Co. acquired 60% of the shares of Sauce Ltd. by issuing...

On January 2, 20X7, Victory Co. acquired 60% of the shares of Sauce Ltd. by issuing shares valued at $1,200,000. On this date, Sauce’s building and machinery had estimated remaining useful lives of 10 years and 5 years respectively. Both Victory and Sauce use straight-line depreciation. The separate-entity statements of financial position for Victory and Sauce just prior to the acquisition are presented below. Statements of Financial Position As of January 1, 20X7 Victory Co. Sauce...

need help... please fix the errors as soon as possible. Thanks

in advance!

Pushdown Accounting Assume a parent company acquires its subsidiary by paying $1,200,000 for all of the outstanding voting shares of the investee. On the acquisition date, subsidiary's assets and liabilities have individual fair values that equal their book values, except for property equipment with a fair value greater than book value by $150,000 and license with a fair value greater than book value by $250,000. The parent...

need help... please fix the errors as soon as possible. Thanks

in advance!

Pushdown Accounting Assume a parent company acquires its subsidiary by paying $1,200,000 for all of the outstanding voting shares of the investee. On the acquisition date, subsidiary's assets and liabilities have individual fair values that equal their book values, except for property equipment with a fair value greater than book value by $150,000 and license with a fair value greater than book value by $250,000. The parent...

Required: 1. Prepare the con are the consolidation and equity accounting entries for the year eaded 31 December 20x5 with narratives and workings). m analytical checks on the following balances as at 31 December 2015 2 Perform analytics (a) Non-controlling interests and (b) Investment in associate. P6.8 Comprehensive problem set P Co acquired a 90% OW quired a 90% ownership interest in Y Co on 1 January 20x3. At the date of acquisition, the share Joy Co was $1,000,000, and...

Required: 1. Prepare the con are the consolidation and equity accounting entries for the year eaded 31 December 20x5 with narratives and workings). m analytical checks on the following balances as at 31 December 2015 2 Perform analytics (a) Non-controlling interests and (b) Investment in associate. P6.8 Comprehensive problem set P Co acquired a 90% OW quired a 90% ownership interest in Y Co on 1 January 20x3. At the date of acquisition, the share Joy Co was $1,000,000, and...

need help asap... please fix the errors asap

Pushdown Accounting Assume a parent company acquires its subsidiary by paying $1,200,000 for all of the outstanding voting shares of the investee. On the acquisition date, subsidiary's assets and liabilities have individual fair values that equal their book values, except for property equipment with a fair value greater than book value by $150,000 and license with a fair value greater than book value by $250,000. The parent and subsidiary have the following...

need help asap... please fix the errors asap

Pushdown Accounting Assume a parent company acquires its subsidiary by paying $1,200,000 for all of the outstanding voting shares of the investee. On the acquisition date, subsidiary's assets and liabilities have individual fair values that equal their book values, except for property equipment with a fair value greater than book value by $150,000 and license with a fair value greater than book value by $250,000. The parent and subsidiary have the following...

tion Equity method ging 59.000 Shares of $30 per share, for e the consolidation LOZ luc Com shares of the first year. individual net values that equaled 00 (depreciation auisition date, allowing: PPE assets inte sot that has a fair value o 320,000 (amor c. Prepare the consolid d. Explain why the (ADJ) consolidating enllyn 48. Consolidation at the end of the first year subsequent to date of acquisition- Assume the parent company acquires its subsidiary on January 1, 2019....

tion Equity method ging 59.000 Shares of $30 per share, for e the consolidation LOZ luc Com shares of the first year. individual net values that equaled 00 (depreciation auisition date, allowing: PPE assets inte sot that has a fair value o 320,000 (amor c. Prepare the consolid d. Explain why the (ADJ) consolidating enllyn 48. Consolidation at the end of the first year subsequent to date of acquisition- Assume the parent company acquires its subsidiary on January 1, 2019....

Corporations on January 1, 2017, just before they entered into a business combination: 13 The following Statement of Financial Position were prepared for Red and Blue So Problem 13-6 Blue Corporation Fair Value P 50,000 245,000 250,000 Items Cash and Receivables Inventory Buildings and Equipment Less: Accumulated Depreciation Total Assets Red Corporation Book Value Fair value Book Value P 300,000 P 300,000 P 50,000 400,000 600,000 100,000 800,000 870,000 300,000 ( 200,000) ( 150,000) P1,300,000 P1,770,000 P300,000 P545,000 P 100,000...

Corporations on January 1, 2017, just before they entered into a business combination: 13 The following Statement of Financial Position were prepared for Red and Blue So Problem 13-6 Blue Corporation Fair Value P 50,000 245,000 250,000 Items Cash and Receivables Inventory Buildings and Equipment Less: Accumulated Depreciation Total Assets Red Corporation Book Value Fair value Book Value P 300,000 P 300,000 P 50,000 400,000 600,000 100,000 800,000 870,000 300,000 ( 200,000) ( 150,000) P1,300,000 P1,770,000 P300,000 P545,000 P 100,000...

Parent Co paid $176,000 for 80% of the outstanding voting stock

of Sub Co on January 1, 2018, when Sub Co’s stockholders’ equity

consisted of $120,000 common stock and $60,000 retained earnings.

This implied that the total fair value of Sub co is $220,000

($176,000 / 80%). The company assigned the $40,000 excess fair

value to previously unrecorded patents with a 10-year useful

life.

Parent Co’s $36,800 income from Sub Co for 2018 consisted of 80%

of Sub Co’s $50,000...

Parent Co paid $176,000 for 80% of the outstanding voting stock

of Sub Co on January 1, 2018, when Sub Co’s stockholders’ equity

consisted of $120,000 common stock and $60,000 retained earnings.

This implied that the total fair value of Sub co is $220,000

($176,000 / 80%). The company assigned the $40,000 excess fair

value to previously unrecorded patents with a 10-year useful

life.

Parent Co’s $36,800 income from Sub Co for 2018 consisted of 80%

of Sub Co’s $50,000...

Question 2 Parent Ltd acquired 60% of the equity in Sub Ltd on 1 April 2014 for $1 200 000. At that date, the equity of Sub Ltd comprised share capital of $600 000 and retained earnings of $340 000 Because Sub Ltd used the cost model for its recognised property, plant, and equipment, it had several items whose book value was lower than fair value at the date of acquisition. The book values and the fair values of these...

Question 2 Parent Ltd acquired 60% of the equity in Sub Ltd on 1 April 2014 for $1 200 000. At that date, the equity of Sub Ltd comprised share capital of $600 000 and retained earnings of $340 000 Because Sub Ltd used the cost model for its recognised property, plant, and equipment, it had several items whose book value was lower than fair value at the date of acquisition. The book values and the fair values of these...

Prepare cosolidated fin. statement

P acquired 75% of the shares in S on 1 January 2007 when S had retained earnings of $15,000. The market price of S's shares just before the date of acquisition was $1.60. P values non-controlling interest at fair value. Goodwill is not impaired. The statements of financial position of P and S at 31 December 20X7 were: 60,000 50,000 Property, plant and equipment Shares in S 68,000_ 128,000 50,000 52.000 35,000 180,000 85,000 100,000 50,000...

Prepare cosolidated fin. statement

P acquired 75% of the shares in S on 1 January 2007 when S had retained earnings of $15,000. The market price of S's shares just before the date of acquisition was $1.60. P values non-controlling interest at fair value. Goodwill is not impaired. The statements of financial position of P and S at 31 December 20X7 were: 60,000 50,000 Property, plant and equipment Shares in S 68,000_ 128,000 50,000 52.000 35,000 180,000 85,000 100,000 50,000...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago