On January 1, 2021, Bradley Recreational Products issued

$120,000, 8%, four-year bonds. Interest is paid semiannually on

June 30 and December 31. The bonds were issued at $112,244 to yield

an annual return of 10%. (FV of $1, PV of $1, FVA of $1, PVA of $1,

FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from

the tables provided.)

Required:

1. Prepare an amortization schedule that determines

interest at the effective interest rate.

2. Prepare an amortization schedule by the

straight-line method.

3. Prepare the journal entries to record interest

expense on June 30, 2023, by each of the two approaches.

5. Assuming the market rate is still 10%, what

price would a second investor pay the first investor on June 30,

2023, for $12,000 of the bonds?

Homework Answers

Requirement 1:

Effective interest method:

|

Payment Number |

Cash Payment |

Effective Interest |

Increase in Balance |

Carrying Value |

| $112,244 | ||||

| 1 | $4,800 | $5,612 | $812 | $113,056 |

| 2 | $4,800 | $5,653 | $853 | $113,909 |

| 3 | $4,800 | $5,695 | $895 | $114,804 |

| 4 | $4,800 | $5,740 | $940 | $115,745 |

| 5 | $4,800 | $5,787 | $987 | $116,732 |

| 6 | $4,800 | $5,837 | $1,037 | $117,769 |

| 7 | $4,800 | $5,888 | $1,088 | $118,857 |

| 8 | $4,800 | $5,943 | $1,143 | $120,000 |

| Totals | $38,400 | $46,156 | $7,756 |

Cash payment = $120,000 x 4% = $4,800

Effective interest = Preceding carrying value x 5%

Increase in balance = Effective interest - Cash payment

Carrying value = Preceding carrying value + Increase in balance

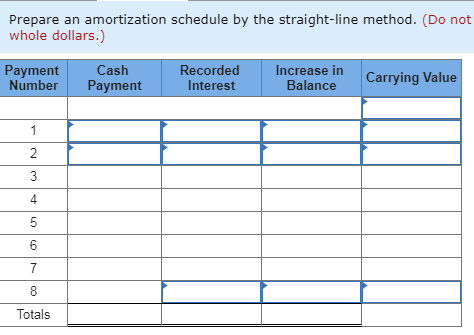

Requirement 2:

Straight-line

|

Payment Number |

Cash Payment |

Recorded Interest |

Increase in Balance |

Carrying Value |

| $112,244 | ||||

| 1 | $4,800 | $5,770 | $969.50 | $113,214 |

| 2 | $4,800 | $5,770 | $969.50 | $114,183 |

| 3 | $4,800 | $5,770 | $969.50 | $115,153 |

| 4 | $4,800 | $5,770 | $969.50 | $116,122 |

| 5 | $4,800 | $5,770 | $969.50 | $117,092 |

| 6 | $4,800 | $5,770 | $969.50 | $118,061 |

| 7 | $4,800 | $5,770 | $969.50 | $119,031 |

| 8 | $4,800 | $5,770 | $969.50 | $120,000 |

| Totals | $38,400 | $46,156 | $7,756 |

Cash payment = $120,000 x 4% = $5,600

Increase in balance = [$120,000-$112,244] ÷ 8 payments = $969.50

Effective interest = Cash payment + Increase in balance

Carrying value = Preceding carrying value + Increase in balance

Requirement 3:

Effective-interest

| Date | Account title and Explanation | Debit | Credit |

| June 30,2023 | Interest expense | $5,787 | |

| Discount on bonds payable | $987 | ||

| Cash | $4,800 | ||

| [To record payment of interest] |

Requirement 4:

| Date | Account title and Explanation | Debit | Credit |

| June 30,2023 | Interest expense | $5,770 | |

| Discount on bonds payable | $970 | ||

| Cash | $4,800 | ||

| [To record payment of interest] |

Requirement 5:

Carrying value of $120,00 on June 30,2023 is $116,732

So, Carrying value of $12,000 on June 30,2023 is $11,673

Thus, price of the bonds of $12,000 on June 30,2023 is $11,673

Add Answer to:

On January 1, 2021, Bradley Recreational Products issued

$120,000, 8%, four-year bonds. Interest is paid semiannually...

On January 1, 2021, Bradley Recreational Products issued $140,000, 8%, four-year bonds. Interest is paid semiannually...

On January 1, 2021, Bradley Recreational Products issued $140,000, 8%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $130,952 to yield an annual return of 10%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2. Prepare an amortization schedule...

On January 1, 2021, Bradley Recreational Products issued $140,000, 8%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $130,952 to yield an annual return of 10%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2. Prepare an amortization schedule...

On January 1, 2021, Bradley Recreational Products issued $150,000, 9%, four-year bonds. Interest is paid semiannually...

On January 1, 2021, Bradley Recreational Products issued $150,000, 9%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $145,153 to yield an annual return of 10%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2. Prepare an amortization schedule...

On January 1, 2021, Bradley Recreational Products issued $150,000, 9%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $145,153 to yield an annual return of 10%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2. Prepare an amortization schedule...

2 Check my won On January 1, 2021, Bradley Recreational Products issued $150,000, 9%, four-year bonds....

2

Check my won On January 1, 2021, Bradley Recreational Products issued $150,000, 9%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $145,153 to yield an annual return of 10%, (FY of $1. PV of S. EVA of $1. PVA of $1. FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2....

2

Check my won On January 1, 2021, Bradley Recreational Products issued $150,000, 9%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $145,153 to yield an annual return of 10%, (FY of $1. PV of S. EVA of $1. PVA of $1. FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2....

On January 1, 2021, Bradley Recreational Products issued $120,000, 9%, four-year bonds. Interest is paid semiannually...

On January 1, 2021, Bradley Recreational Products issued $120,000, 9%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $116,122 to yield an annual return of 10%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2. Prepare an amortization schedule...

On January 1, 2018, Bradley Recreational Products issued $100,000, 12%, four-year bonds. Interest is paid semiannually...

On January 1, 2018, Bradley Recreational Products issued $100,000, 12%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $94,029 to yield an annual return of 14%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2. Prepare an amortization schedule...

On January 1, 2018, Bradley Recreational Products issued $100,000, 11%, four-year bonds. Interest is paid semiannually...

On January 1, 2018, Bradley Recreational Products issued $100,000, 11%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $96,895 to yield an annual return of 12%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2. Prepare an amortization schedule by...

On January 1, 2021, Fowl Products issued $77 million of 7%, 10-year convertible bonds at a...

On January 1, 2021, Fowl Products issued $77 million of 7%, 10-year convertible bonds at a net price of $78.3 million. Fowl recently issued similar, but nonconvertible, bonds at 97 (that is, 97% of face amount). The bonds pay interest on June 30 and December 31 Each $1,000 bond is convertible into 25 shares of Fowl's no par common stock. Fowl records interest by the straight-line method. On June 1, 2023, Fowl notified bondholders of its intent to call the...

On January 1, 2021, Fowl Products issued $77 million of 7%, 10-year convertible bonds at a net price of $78.3 million. Fowl recently issued similar, but nonconvertible, bonds at 97 (that is, 97% of face amount). The bonds pay interest on June 30 and December 31 Each $1,000 bond is convertible into 25 shares of Fowl's no par common stock. Fowl records interest by the straight-line method. On June 1, 2023, Fowl notified bondholders of its intent to call the...

On January 1, 2021, Madison Products issued $40.7 million of 10%, 10 year convertible bonds at...

On January 1, 2021, Madison Products issued $40.7 million of 10%, 10 year convertible bonds at a net price of $41.57 million Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight-line method On June 1, 2023, Madison notified bondholders of its intent to call...

On January 1, 2021, Madison Products issued $40.7 million of 10%, 10 year convertible bonds at a net price of $41.57 million Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight-line method On June 1, 2023, Madison notified bondholders of its intent to call...

On January 1, 2021, Madison Products issued $41.9 million of 8%, 10-year convertible bonds at a...

On January 1, 2021, Madison Products issued $41.9 million of 8%, 10-year convertible bonds at a net price of $42.89 million. Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight-line method. On June 1, 2023, Madison notified bondholders of its intent to call the...

On January 1, 2021, Madison Products issued $41.9 million of 8%, 10-year convertible bonds at a net price of $42.89 million. Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight-line method. On June 1, 2023, Madison notified bondholders of its intent to call the...

On January 1, 2021, Madison Products issued $41.7 million of 6%, 10-year convertible bonds at a...

On January 1, 2021, Madison Products issued $41.7 million of 6%, 10-year convertible bonds at a net price of $42.67 million. Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight line method On June 1 2023. Madison notified bondholders of its intent to call...

On January 1, 2021, Madison Products issued $41.7 million of 6%, 10-year convertible bonds at a net price of $42.67 million. Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight line method On June 1 2023. Madison notified bondholders of its intent to call...

On January 1, 2021, Bradley Recreational Products issued $140,000, 8%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $130,952 to yield an annual return of 10%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2. Prepare an amortization schedule...

On January 1, 2021, Bradley Recreational Products issued $140,000, 8%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $130,952 to yield an annual return of 10%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2. Prepare an amortization schedule...

On January 1, 2021, Bradley Recreational Products issued $150,000, 9%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $145,153 to yield an annual return of 10%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2. Prepare an amortization schedule...

On January 1, 2021, Bradley Recreational Products issued $150,000, 9%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $145,153 to yield an annual return of 10%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2. Prepare an amortization schedule...

2

Check my won On January 1, 2021, Bradley Recreational Products issued $150,000, 9%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $145,153 to yield an annual return of 10%, (FY of $1. PV of S. EVA of $1. PVA of $1. FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2....

2

Check my won On January 1, 2021, Bradley Recreational Products issued $150,000, 9%, four-year bonds. Interest is paid semiannually on June 30 and December 31. The bonds were issued at $145,153 to yield an annual return of 10%, (FY of $1. PV of S. EVA of $1. PVA of $1. FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare an amortization schedule that determines interest at the effective interest rate. 2....

On January 1, 2021, Fowl Products issued $77 million of 7%, 10-year convertible bonds at a net price of $78.3 million. Fowl recently issued similar, but nonconvertible, bonds at 97 (that is, 97% of face amount). The bonds pay interest on June 30 and December 31 Each $1,000 bond is convertible into 25 shares of Fowl's no par common stock. Fowl records interest by the straight-line method. On June 1, 2023, Fowl notified bondholders of its intent to call the...

On January 1, 2021, Fowl Products issued $77 million of 7%, 10-year convertible bonds at a net price of $78.3 million. Fowl recently issued similar, but nonconvertible, bonds at 97 (that is, 97% of face amount). The bonds pay interest on June 30 and December 31 Each $1,000 bond is convertible into 25 shares of Fowl's no par common stock. Fowl records interest by the straight-line method. On June 1, 2023, Fowl notified bondholders of its intent to call the...

On January 1, 2021, Madison Products issued $40.7 million of 10%, 10 year convertible bonds at a net price of $41.57 million Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight-line method On June 1, 2023, Madison notified bondholders of its intent to call...

On January 1, 2021, Madison Products issued $40.7 million of 10%, 10 year convertible bonds at a net price of $41.57 million Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight-line method On June 1, 2023, Madison notified bondholders of its intent to call...

On January 1, 2021, Madison Products issued $41.9 million of 8%, 10-year convertible bonds at a net price of $42.89 million. Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight-line method. On June 1, 2023, Madison notified bondholders of its intent to call the...

On January 1, 2021, Madison Products issued $41.9 million of 8%, 10-year convertible bonds at a net price of $42.89 million. Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight-line method. On June 1, 2023, Madison notified bondholders of its intent to call the...

On January 1, 2021, Madison Products issued $41.7 million of 6%, 10-year convertible bonds at a net price of $42.67 million. Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight line method On June 1 2023. Madison notified bondholders of its intent to call...

On January 1, 2021, Madison Products issued $41.7 million of 6%, 10-year convertible bonds at a net price of $42.67 million. Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is convertible into 30 shares of Madison's no par common stock. Madison records interest by the straight line method On June 1 2023. Madison notified bondholders of its intent to call...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago