Homework Answers

Add Answer to:

Q9. Capital management Third Bank has the following balance sheet (in millions), with the risk weights...

“Third Bank” has the following balance sheet (in millions of dollars) with the risk weights in...

“Third Bank” has the following balance sheet (in millions of dollars) with the risk weights in parentheses. ASSET cash (0%) $20 interbank deposit with aa rated banks (20%) $25 Standard residential mortgages non- insured with LVR of 85 % (50%) $70 Business loans to BB rated borrowers (100%) $70 Total $185 Liabilities a equity Deposit $175 Subordinated debt (5 years) (Tier 2 capital) $3 Cumulative perference shares (Tier 1) $5 Common Equity (Tier 1) $ 2 Total $185 In addition,...

"Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in...

"Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. Assets Liabilities and equ Cash (096 Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50% Business loans to BB rated borrowers (100%) Total assets 20 Deposits 175 25 Subordinated debt (5 years) 70 Cumulative preference shares 70 Common equity (Tier 1) 185 Total liabilities and equit Tier 2 capita er 1 185 In addition, the...

"Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. Assets Liabilities and equ Cash (096 Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50% Business loans to BB rated borrowers (100%) Total assets 20 Deposits 175 25 Subordinated debt (5 years) 70 Cumulative preference shares 70 Common equity (Tier 1) 185 Total liabilities and equit Tier 2 capita er 1 185 In addition, the...

SOLVENCY RISK AND BANK REGULATION QUESTION: SOLVENCY AND CAPITAL REGULATION QUESTION: SOLVENCY AND CAPITAL REGULATION Third...

SOLVENCY RISK AND BANK REGULATION QUESTION: SOLVENCY AND CAPITAL

REGULATION

QUESTION: SOLVENCY AND CAPITAL REGULATION Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses Assets Liabilities and equity Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets $20 Deposits $175 25Subordinated debt (5 years) 70 Cumulative preference shares 70 Common equity (Tier 1)...

SOLVENCY RISK AND BANK REGULATION QUESTION: SOLVENCY AND CAPITAL

REGULATION

QUESTION: SOLVENCY AND CAPITAL REGULATION Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses Assets Liabilities and equity Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets $20 Deposits $175 25Subordinated debt (5 years) 70 Cumulative preference shares 70 Common equity (Tier 1)...

*NOTE : iNFO Basel Accord in table at bottom of provided Question sheet. Thank you. QUESTION...

*NOTE : iNFO Basel Accord in table at bottom of provided

Question sheet. Thank you.

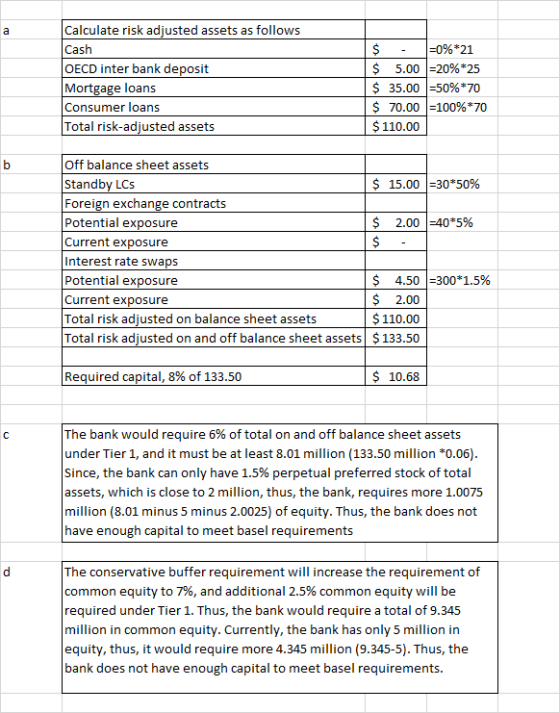

QUESTION 17: SOLVENCY AND CAPITAL REGULATION "Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. | $175 Assets Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets Liabilities and equity $20 Deposits Subordinated debt (5 years) (Tier 2...

*NOTE : iNFO Basel Accord in table at bottom of provided

Question sheet. Thank you.

QUESTION 17: SOLVENCY AND CAPITAL REGULATION "Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. | $175 Assets Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets Liabilities and equity $20 Deposits Subordinated debt (5 years) (Tier 2...

*NOTE : iNFO Basel Accord in table at bottom of provided Question sheet. Thank you. QUESTION...

*NOTE : iNFO Basel Accord in table at bottom of provided

Question sheet. Thank you.

QUESTION 17: SOLVENCY AND CAPITAL REGULATION "Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. | $175 Assets Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets Liabilities and equity $20 Deposits Subordinated debt (5 years) (Tier 2...

*NOTE : iNFO Basel Accord in table at bottom of provided

Question sheet. Thank you.

QUESTION 17: SOLVENCY AND CAPITAL REGULATION "Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. | $175 Assets Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets Liabilities and equity $20 Deposits Subordinated debt (5 years) (Tier 2...

Question C2 (a) Onshore Bank has $20 million in assets, with risk-adjusted assets of $10 million....

Question C2 (a) Onshore Bank has $20 million in assets, with risk-adjusted assets of $10 million. CET1 capital is $500,000, additional Tier I capital is $50,000 and Tier II capital is $400,000. Calculate the new (1) amount of risk-adjusted assets, (2) CET1 risk-based ratio, (3) Tier I risk-based capital ratio and (4) total risk-based capital ratio after considering the following transactions separately. (i) The bank issues $2 million of Certificate of Deposits (CDs) and uses the proceeds to finance single...

Question C2 (a) Onshore Bank has $20 million in assets, with risk-adjusted assets of $10 million. CET1 capital is $500,000, additional Tier I capital is $50,000 and Tier II capital is $400,000. Calculate the new (1) amount of risk-adjusted assets, (2) CET1 risk-based ratio, (3) Tier I risk-based capital ratio and (4) total risk-based capital ratio after considering the following transactions separately. (i) The bank issues $2 million of Certificate of Deposits (CDs) and uses the proceeds to finance single...

Onshore Bank has $28 million in assets, with risk-adjusted assets of $18 million. Core Equity Tier...

Onshore Bank has $28 million in assets, with risk-adjusted assets of $18 million. Core Equity Tier 1 (CET1) capital is $950,000, additional Tier I capital is $210,000, and Tier II capital is $416,000. The current value of the CET1 ratio is 5.28 percent, the Tier I ratio is 6.44 percent, and the total capital ratio is 8.76 percent. A. Calculate the new value of CET1, Tier I, and Total capital ratios for the following transactions: The bank issues $2.8 million...

Based on the following table, does the bank have sufficient Tier 1 capital according to the Basel III standards? Recal...

Based on the following table, does the bank have sufficient Tier 1 capital according to the Basel III standards? Recall: Tier 1 standard (including capital conservation buffer) is 8.5% and Tier 1+Tier 2 standard (including capital conservation buffer) is 10.5%. Risk-Weight Assets ($M) Risk-Weighted Category Assets ($M) 1500 20% 450 90 50% 1,000 100% 1,000 TOTAL Risk-Weighted Assets | 1,590 Capital (SM) 120 50 0% Tier 1 Tier 2 500 1,000 Yes Ο Νο Based on the following table, does...

Based on the following table, does the bank have sufficient Tier 1 capital according to the Basel III standards? Recall: Tier 1 standard (including capital conservation buffer) is 8.5% and Tier 1+Tier 2 standard (including capital conservation buffer) is 10.5%. Risk-Weight Assets ($M) Risk-Weighted Category Assets ($M) 1500 20% 450 90 50% 1,000 100% 1,000 TOTAL Risk-Weighted Assets | 1,590 Capital (SM) 120 50 0% Tier 1 Tier 2 500 1,000 Yes Ο Νο Based on the following table, does...

Sigma Bank has the following balance sheet in millions of dollars. assets liabilities current assets current...

Sigma Bank has the following balance sheet in millions of dollars. assets liabilities current assets current liabilities cash 21 repo agreements 265 petty cash 0.0001 commercial paper 35.9 marketable securities 8 wages payable 8.5 Long term corp bonds 40.5 interest payable 2.9 residential mortgages 31 taxes payable 4.1 commercial mortgages 3.8 federal funds loans 1.1 prepaid insurance 1.5 unearned revenues 1.5 total current assets 106 accrued income 2.0 total current liabilities 321 investments Sovereign bonds 10 long term liabilities Loans...

Based on the following information measure the capital adequacy of cosmopolite bank using the ris...

based on the following information measure the capital

adequacy of cosmopolite bank using the risk adjusted capital

standards. tier capitol is 60 million and tier II capitol is 15

million. also consider not, suggest several ways Management might

address the shortfall.

eC FINA4600 Capital Adequacy Problems taken from: Gardner and Mills 3d edition, Dryden Press, 1994) 1. Based on the following information, measure the capital adequacy of adjusted capital standards. Tier I capital is $60 million and Tier ll capital...

based on the following information measure the capital

adequacy of cosmopolite bank using the risk adjusted capital

standards. tier capitol is 60 million and tier II capitol is 15

million. also consider not, suggest several ways Management might

address the shortfall.

eC FINA4600 Capital Adequacy Problems taken from: Gardner and Mills 3d edition, Dryden Press, 1994) 1. Based on the following information, measure the capital adequacy of adjusted capital standards. Tier I capital is $60 million and Tier ll capital...

"Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. Assets Liabilities and equ Cash (096 Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50% Business loans to BB rated borrowers (100%) Total assets 20 Deposits 175 25 Subordinated debt (5 years) 70 Cumulative preference shares 70 Common equity (Tier 1) 185 Total liabilities and equit Tier 2 capita er 1 185 In addition, the...

"Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. Assets Liabilities and equ Cash (096 Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50% Business loans to BB rated borrowers (100%) Total assets 20 Deposits 175 25 Subordinated debt (5 years) 70 Cumulative preference shares 70 Common equity (Tier 1) 185 Total liabilities and equit Tier 2 capita er 1 185 In addition, the...

SOLVENCY RISK AND BANK REGULATION QUESTION: SOLVENCY AND CAPITAL

REGULATION

QUESTION: SOLVENCY AND CAPITAL REGULATION Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses Assets Liabilities and equity Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets $20 Deposits $175 25Subordinated debt (5 years) 70 Cumulative preference shares 70 Common equity (Tier 1)...

SOLVENCY RISK AND BANK REGULATION QUESTION: SOLVENCY AND CAPITAL

REGULATION

QUESTION: SOLVENCY AND CAPITAL REGULATION Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses Assets Liabilities and equity Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets $20 Deposits $175 25Subordinated debt (5 years) 70 Cumulative preference shares 70 Common equity (Tier 1)...

*NOTE : iNFO Basel Accord in table at bottom of provided

Question sheet. Thank you.

QUESTION 17: SOLVENCY AND CAPITAL REGULATION "Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. | $175 Assets Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets Liabilities and equity $20 Deposits Subordinated debt (5 years) (Tier 2...

*NOTE : iNFO Basel Accord in table at bottom of provided

Question sheet. Thank you.

QUESTION 17: SOLVENCY AND CAPITAL REGULATION "Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. | $175 Assets Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets Liabilities and equity $20 Deposits Subordinated debt (5 years) (Tier 2...

*NOTE : iNFO Basel Accord in table at bottom of provided

Question sheet. Thank you.

QUESTION 17: SOLVENCY AND CAPITAL REGULATION "Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. | $175 Assets Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets Liabilities and equity $20 Deposits Subordinated debt (5 years) (Tier 2...

*NOTE : iNFO Basel Accord in table at bottom of provided

Question sheet. Thank you.

QUESTION 17: SOLVENCY AND CAPITAL REGULATION "Third Bank" has the following balance sheet (in millions of dollars) with the risk weights in parentheses. | $175 Assets Cash (0%) Interbank deposits with AA rated banks (20%) Standard residential mortgages non- insured with LVR of 85% (50%) Business loans to BB rated borrowers (100%) Total assets Liabilities and equity $20 Deposits Subordinated debt (5 years) (Tier 2...

Question C2 (a) Onshore Bank has $20 million in assets, with risk-adjusted assets of $10 million. CET1 capital is $500,000, additional Tier I capital is $50,000 and Tier II capital is $400,000. Calculate the new (1) amount of risk-adjusted assets, (2) CET1 risk-based ratio, (3) Tier I risk-based capital ratio and (4) total risk-based capital ratio after considering the following transactions separately. (i) The bank issues $2 million of Certificate of Deposits (CDs) and uses the proceeds to finance single...

Question C2 (a) Onshore Bank has $20 million in assets, with risk-adjusted assets of $10 million. CET1 capital is $500,000, additional Tier I capital is $50,000 and Tier II capital is $400,000. Calculate the new (1) amount of risk-adjusted assets, (2) CET1 risk-based ratio, (3) Tier I risk-based capital ratio and (4) total risk-based capital ratio after considering the following transactions separately. (i) The bank issues $2 million of Certificate of Deposits (CDs) and uses the proceeds to finance single...

Based on the following table, does the bank have sufficient Tier 1 capital according to the Basel III standards? Recall: Tier 1 standard (including capital conservation buffer) is 8.5% and Tier 1+Tier 2 standard (including capital conservation buffer) is 10.5%. Risk-Weight Assets ($M) Risk-Weighted Category Assets ($M) 1500 20% 450 90 50% 1,000 100% 1,000 TOTAL Risk-Weighted Assets | 1,590 Capital (SM) 120 50 0% Tier 1 Tier 2 500 1,000 Yes Ο Νο Based on the following table, does...

Based on the following table, does the bank have sufficient Tier 1 capital according to the Basel III standards? Recall: Tier 1 standard (including capital conservation buffer) is 8.5% and Tier 1+Tier 2 standard (including capital conservation buffer) is 10.5%. Risk-Weight Assets ($M) Risk-Weighted Category Assets ($M) 1500 20% 450 90 50% 1,000 100% 1,000 TOTAL Risk-Weighted Assets | 1,590 Capital (SM) 120 50 0% Tier 1 Tier 2 500 1,000 Yes Ο Νο Based on the following table, does...

based on the following information measure the capital

adequacy of cosmopolite bank using the risk adjusted capital

standards. tier capitol is 60 million and tier II capitol is 15

million. also consider not, suggest several ways Management might

address the shortfall.

eC FINA4600 Capital Adequacy Problems taken from: Gardner and Mills 3d edition, Dryden Press, 1994) 1. Based on the following information, measure the capital adequacy of adjusted capital standards. Tier I capital is $60 million and Tier ll capital...

based on the following information measure the capital

adequacy of cosmopolite bank using the risk adjusted capital

standards. tier capitol is 60 million and tier II capitol is 15

million. also consider not, suggest several ways Management might

address the shortfall.

eC FINA4600 Capital Adequacy Problems taken from: Gardner and Mills 3d edition, Dryden Press, 1994) 1. Based on the following information, measure the capital adequacy of adjusted capital standards. Tier I capital is $60 million and Tier ll capital...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago