1. There is a put option for Euros with a strike price of $1.22 and a...

1. There is a put option for Euros with a strike price of $1.22 and a premium of $.06. There is another put option for Euros with a strike price of $1.16 and a premium of $0.03. You are slightly pessimistic about the Euro and decide to utilize a bear spread using these two put options.

a) Please draw the contingency graph and identify the maximum gain and loss as well as the breakeven point.

b) Assuming the resulting spot rate is $1.17 and each put option contract represents 50,000 Euros, what is the overall profit or loss?

Homework Answers

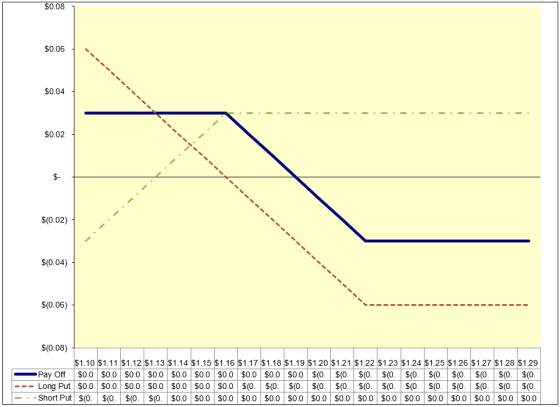

Below are the Snippets from the excel of the Bear Spread using Put option.

Bear Strategy: Buying A Put option at the higher strike price and selling a Put option at the lower Strike price. Creating a limited gain from the bearish trend of the market while also limiting the loss at the bullish trend of the market.

a) As can be seen from the pay-off matrix at the second image that,

Max. Profit= $0.03

Max. Loss= $0.03

And Break-even point is at = $1.19 of market rate

b) If the Market/Spot rate is at $1.17 then,

Cash-flow from buy-side put option:

= Max(0,(Strike Price - Spot Price)) - Put Price

= $1.22 - $1.17 - $0.06

= $0.05 - $0.06

= -$0.01

Cash-flow from sell-side put option:

= -Max(0,(Spot Price - Strike Price)) + Put Price

= -Max(0,($1.17 - $1.16)) + $0.03

= $0.00 + $0.03

= $0.03

Adding above both cash flows, Profit/Loss at spot price of $1.17= -$0.01 + $0.03 = $0.02

Add Answer to:

1. There is a put option for Euros

with a strike price of $1.22 and a...

23. (20 points) There is a call option for Euros with a strike price of $1.10...

23. (20 points) There is a call option for Euros with a strike price of $1.10 and a premium of $.06.T for Euros with a strike price of $1.18 and a You do not expect the Euro to fluctuate much at all. Therefore you decide to short both of these two options. premium of $0.04. The current spot rat is $1.15 per Euro. Please draw the final contingency graph (including break even, max loss, max gain). You may draw the...

23. (20 points) There is a call option for Euros with a strike price of $1.10 and a premium of $.06.T for Euros with a strike price of $1.18 and a You do not expect the Euro to fluctuate much at all. Therefore you decide to short both of these two options. premium of $0.04. The current spot rat is $1.15 per Euro. Please draw the final contingency graph (including break even, max loss, max gain). You may draw the...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

Henrik's Options. Assume Henrik writes a call option on euros with a strike price of $1.2500/euro...

Henrik's Options. Assume Henrik writes a call option on euros with a strike price of $1.2500/euro at a premium of 3.80cents per euro ($0.0380/euro) and with an expiration date three months from now. The option is for euro100 comma 000. Calculate Henrik's profit or loss should he exercise before maturity at a time when the euro is traded spot at strike prices beginning at $1.10/euro, rising to $1.34/euro in increments of $0.04. The profit or loss should Henrik exercise before...

Henrik's Options. Assume Henrik writes a call option on euros with a strike price of $1.2500/euro...

Henrik's Options. Assume Henrik writes a call option on euros with a strike price of $1.2500/euro at a premium of 3.80cents per euro ($0.0380/euro) and with an expiration date three months from now. The option is for euro100 comma 000. Calculate Henrik's profit or loss should he exercise before maturity at a time when the euro is traded spot at strike prices beginning at $1.10/euro, rising to $1.34/euro in increments of $0.04. The profit or loss should Henrik exercise before...

Warrior Industries buys a June call option on Euros (contract size is 500,000 euros) on March...

Warrior Industries buys a June call option on Euros (contract size is 500,000 euros) on March 1 that has a strike (exercise) price of $0.58. They pay a premium of $0.05 per euro, and the March 1 spot rate is $0.60. On the expiration date in June, the spot rate is $0.62. What is Warrior's profit (loss) on the option? Answer options: -$15,000 -$5,000 $5,000 $0

1. Suppose you buy a put option on a $100,000 worth of euros with an exercise...

1. Suppose you buy a put option on a $100,000 worth of euros with an exercise price of $1.10 per euro for a premium of $1500. If on expiration the spot exchange rate is $1.12 per euro, what is your net profit or loss?

1. A put option has a strike price of $4.78 and a premium of $0.01. At...

1. A put option has a strike price of $4.78 and a premium of $0.01. At expiration, the price of the underlying is $4.81. What is the breakeven price of the option? Ignoring the premium, what is the profit or loss to the option holder at expiration.

1. A put option has a strike price of $4.78 and a premium of $0.01. At expiration, the price of the underlying is $4.81. What is the breakeven price of the option? Ignoring the premium, what is the profit or loss to the option holder at expiration.

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price =...

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price = $1.10/€, Option contract size = €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium Spot exchange rate $1.00/€ $1.05/€ $1.10/€ $1.15/€ $1.20/€ $1.25/€ Long call option Exercise (N/Y) Holder’s net profit per unit Long put option Exercise (N/Y) Holder’s net profit per unit Net profit Net profit per unit (graph) Short currency straddle Call...

IBM sells a call option on euros (contract size is €600,000) at a premium of $0.02...

IBM sells a call option on euros (contract size is €600,000) at a premium of $0.02 per euro. If the exercise price is $1.44/€ and the spot price of the euro at date of expiration is $1.45/€, A. Will this option be exercised, that is, is in-the-money or out-of-the-money? Why? (2 points) B. What is IBM’s profit (or loss) on the call option? (3 points)

Consider a put option on a share of Apple Stock (current spot price = $175) with...

Consider a put option on a share of Apple Stock (current spot price = $175) with an expiration of March 15, 2019 and a strike of $170. One contract is for 50 shares and has a premium of $450.00. What is the breakeven point of this contract? If the spot price of Apple at maturity is $165, then what is the profit from one long contract?

23. (20 points) There is a call option for Euros with a strike price of $1.10 and a premium of $.06.T for Euros with a strike price of $1.18 and a You do not expect the Euro to fluctuate much at all. Therefore you decide to short both of these two options. premium of $0.04. The current spot rat is $1.15 per Euro. Please draw the final contingency graph (including break even, max loss, max gain). You may draw the...

23. (20 points) There is a call option for Euros with a strike price of $1.10 and a premium of $.06.T for Euros with a strike price of $1.18 and a You do not expect the Euro to fluctuate much at all. Therefore you decide to short both of these two options. premium of $0.04. The current spot rat is $1.15 per Euro. Please draw the final contingency graph (including break even, max loss, max gain). You may draw the...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

1. A put option has a strike price of $4.78 and a premium of $0.01. At expiration, the price of the underlying is $4.81. What is the breakeven price of the option? Ignoring the premium, what is the profit or loss to the option holder at expiration.

1. A put option has a strike price of $4.78 and a premium of $0.01. At expiration, the price of the underlying is $4.81. What is the breakeven price of the option? Ignoring the premium, what is the profit or loss to the option holder at expiration.

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago