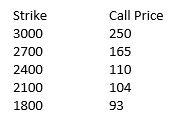

Consider a 1-year put option on the SP500 index. Suppose the current index is 3000, the 1-year risk free rate is 1% and the dividend yield is 2%. Suppose the observed put prices for different strikes are as follows:

Find the implied volatility for each strike.

Homework Answers

Add Answer to:

Consider a 1-year put option on the SP500 index. Suppose the

current index is 3000, the...

Consider the gamma of a European call option with 1-year maturity on the S&P500 index. The...

Consider the gamma of a European call option with 1-year maturity on the S&P500 index. The option has a strike of 2300, the dividend yield on the S&P500 index is 2%, and its volatility is 15%. Further assume the riskless interest rate is 5%. (a) Plot the gamma of the option as a function of the underlying asset price. (b) For what values of the S&P500 index is the option’s gamma the highest when the call approaches expiration?

Problem 7 Using the information in the table below, derive your best estimate of the price of the put option, if at...

Problem 7 Using the information in the table below, derive your best estimate of the price of the put option, if at the same time the index level increases from 250 to 255, and the volatility increases from 10% to 14%. Assume that the changes happen instantaneously after the computation of the price and sensitivities given in the table below (no time decay). Underlying Type: Index Index Level: Volatility (% per year): Risk-Free Rate (% per year): Dividend Yield (%...

Problem 7 Using the information in the table below, derive your best estimate of the price of the put option, if at the same time the index level increases from 250 to 255, and the volatility increases from 10% to 14%. Assume that the changes happen instantaneously after the computation of the price and sensitivities given in the table below (no time decay). Underlying Type: Index Index Level: Volatility (% per year): Risk-Free Rate (% per year): Dividend Yield (%...

Consider a European put option on a non-dividend-paying stock. The current stock price is $69, the...

Consider a European put option on a non-dividend-paying stock. The current stock price is $69, the strike price is $70, the risk-free interest rate is 5% per annum, the volatility is 35% per annum and the time to maturity is 6 months. a. Use the Black-Scholes model to calculate the put price. b. Calculate the corresponding call option using the put-call parity relation. Use the Option Calculator Spreadsheet to verify your result.

Problem 1. 1. Calculate the price of a six-month European put option on a non-dividend-paying stock...

Problem 1. 1. Calculate the price of a six-month European put option on a non-dividend-paying stock with an exercise price of $90 when the current stock price is $100, the annualized riskless rate of interest is 3%, and the volatility is 40% per year. 2. Calculate the price of a six-month European call option with an exercise price on this same stock a non-dividend-paying stock with an exercise price of $90. Problem 2. Re-calculate the put and call option prices...

NEED HELP 1. The current stock price is $50. Consider a call and a put option...

NEED HELP

1. The current stock price is $50. Consider a call and a put option on this stock with 1 year to maturity. If the interest rate is 8% per annum continuously compounded, at what strike price would the prices of the call and put options be the same? A. $43.18 B. $46.15 C. $54.16 D. $57.33 E. $60.12

NEED HELP

1. The current stock price is $50. Consider a call and a put option on this stock with 1 year to maturity. If the interest rate is 8% per annum continuously compounded, at what strike price would the prices of the call and put options be the same? A. $43.18 B. $46.15 C. $54.16 D. $57.33 E. $60.12

Consider delta and gamma hedging a short call option, using the underlying and a put with...

Consider delta and gamma hedging a short call option, using the underlying and a put with the same strike and maturity as the call. Calculate the position in the underlying and the put that you should take. Will you ever need to adjust this hedge? Relate your result to put-call parity. Asset price S0 50 Exercise price K 40 Interest rate r 0.05 Volatility sigma 0.3 Dividend yield q 0.02 Time to maturity T 2 Expected return mu 0.12 Number...

1. Consider the following information about a European call option on stock ABC: . The strike...

1. Consider the following information about a European call option on stock ABC: . The strike price is S100 The current stock price is $110 The time to expiration is one year The annual continuously-compounded risk-free rate is 5% ·The continuous dividend yield is 3.5% Volatility is 30% . The length of period is 4 months. Find the risk-neutral probability p*. Hint: 45.68%

1. Consider the following information about a European call option on stock ABC: . The strike price is S100 The current stock price is $110 The time to expiration is one year The annual continuously-compounded risk-free rate is 5% ·The continuous dividend yield is 3.5% Volatility is 30% . The length of period is 4 months. Find the risk-neutral probability p*. Hint: 45.68%

1. [3 points] Assume that the current stock price is 30, the stock pays dividend continuously...

1. [3 points] Assume that the current stock price is 30, the stock pays dividend continuously at a rate proportional to its price with yield 4%, and the volatility of stock is 18%. Suppose a one-year, 32-strike European call option and put option have prices 1.8779 and 2.3000. Jack sold 25 units of this cal option at time 0 and immediately used the delta hedge. After 3 months, the stock price becomes 35 and the call option price becomes 4.6345....

1. [3 points] Assume that the current stock price is 30, the stock pays dividend continuously at a rate proportional to its price with yield 4%, and the volatility of stock is 18%. Suppose a one-year, 32-strike European call option and put option have prices 1.8779 and 2.3000. Jack sold 25 units of this cal option at time 0 and immediately used the delta hedge. After 3 months, the stock price becomes 35 and the call option price becomes 4.6345....

A 1-year European put option on a stock with strike price of $50 is quoted as...

A 1-year European put option on a stock with strike price of $50 is quoted as $7; a 1-year European call option on the same stock with strike price $30 is quoted as $5. Suppose you long one put and short one call (one option is on 100 share). a) Draw the payoff diagram for your put position and call position. (5 points) b) After 1-year, stock price turns out to be $45. What is your total payoff? What is...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Problem 7 Using the information in the table below, derive your best estimate of the price of the put option, if at the same time the index level increases from 250 to 255, and the volatility increases from 10% to 14%. Assume that the changes happen instantaneously after the computation of the price and sensitivities given in the table below (no time decay). Underlying Type: Index Index Level: Volatility (% per year): Risk-Free Rate (% per year): Dividend Yield (%...

Problem 7 Using the information in the table below, derive your best estimate of the price of the put option, if at the same time the index level increases from 250 to 255, and the volatility increases from 10% to 14%. Assume that the changes happen instantaneously after the computation of the price and sensitivities given in the table below (no time decay). Underlying Type: Index Index Level: Volatility (% per year): Risk-Free Rate (% per year): Dividend Yield (%...

NEED HELP

1. The current stock price is $50. Consider a call and a put option on this stock with 1 year to maturity. If the interest rate is 8% per annum continuously compounded, at what strike price would the prices of the call and put options be the same? A. $43.18 B. $46.15 C. $54.16 D. $57.33 E. $60.12

NEED HELP

1. The current stock price is $50. Consider a call and a put option on this stock with 1 year to maturity. If the interest rate is 8% per annum continuously compounded, at what strike price would the prices of the call and put options be the same? A. $43.18 B. $46.15 C. $54.16 D. $57.33 E. $60.12

1. Consider the following information about a European call option on stock ABC: . The strike price is S100 The current stock price is $110 The time to expiration is one year The annual continuously-compounded risk-free rate is 5% ·The continuous dividend yield is 3.5% Volatility is 30% . The length of period is 4 months. Find the risk-neutral probability p*. Hint: 45.68%

1. Consider the following information about a European call option on stock ABC: . The strike price is S100 The current stock price is $110 The time to expiration is one year The annual continuously-compounded risk-free rate is 5% ·The continuous dividend yield is 3.5% Volatility is 30% . The length of period is 4 months. Find the risk-neutral probability p*. Hint: 45.68%

1. [3 points] Assume that the current stock price is 30, the stock pays dividend continuously at a rate proportional to its price with yield 4%, and the volatility of stock is 18%. Suppose a one-year, 32-strike European call option and put option have prices 1.8779 and 2.3000. Jack sold 25 units of this cal option at time 0 and immediately used the delta hedge. After 3 months, the stock price becomes 35 and the call option price becomes 4.6345....

1. [3 points] Assume that the current stock price is 30, the stock pays dividend continuously at a rate proportional to its price with yield 4%, and the volatility of stock is 18%. Suppose a one-year, 32-strike European call option and put option have prices 1.8779 and 2.3000. Jack sold 25 units of this cal option at time 0 and immediately used the delta hedge. After 3 months, the stock price becomes 35 and the call option price becomes 4.6345....

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago