Assume that the assumptions of the CAPM hold. The expected return and the standard deviation of...

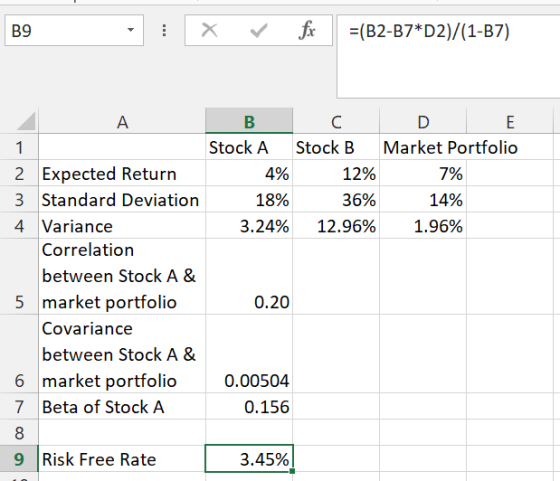

Assume that the assumptions of the CAPM hold. The expected return and the standard deviation of the market portfolio are 7% and 14%, respectively. There are two individual stocks A and B:

Mean Return A: 4% Standard Deviation A: 18%

Mean Return B: 12% Standard Deviation B: 36%

Stock A has a correlation of 0.2 with the market portfolio.

A.What is the beta of stock A?

B.What is the risk free rate?

C.What is the beta of a portfolio with 40% in stock A and 60% in stock B?

D.What is the idiosyncratic volatility of the portfolio from part C?

Homework Answers

A.

Beta = Covariance(Stock returns, market portfolio returns)/Variance(Stock Returns)

Covariance(Stock returns, market portfolio returns) = Correlation(Stock returns, market portfolio returns)*Standard Deviation of Stock Returns*Standard Deviation of Market Portfolio

b.

Using CAPM

Expected Stock Return = Risk Free Rate +Beta*(Market Returns - Risk Free Rate)

Risk free rate = [Expected Stock return - Beta*Market Return]/(1 - Beta)

c.

Using CAPM

Beta = (Expected Return - Risk Free Rate)/(Market Returns - Risk Free Rate)

D.

Idiosyncratic Volatility = Total Variance - Market Variance

Add Answer to:

Assume that the assumptions of the CAPM hold. The expected

return and the standard deviation of...

Assume a setting in which the risk-free rate is 4% and the CAPM holds. The market...

Assume a setting in which the risk-free rate is 4% and the CAPM holds. The market portfolio has a mean return of 16% and a return standard deviation of 30%. The data on two stocks that exist in this market are as follows. Stock X has a mean return of 10% and a standard deviation of 40%. Stock Y has a mean return of 20% and a standard deviation of 50%. The pair of stocks have a return correlation of...

Assume a setting in which the risk-free rate is 4% and the CAPM holds. The market portfolio has a mean return of 16% and a return standard deviation of 30%. The data on two stocks that exist in this market are as follows. Stock X has a mean return of 10% and a standard deviation of 40%. Stock Y has a mean return of 20% and a standard deviation of 50%. The pair of stocks have a return correlation of...

Compute the expected return, standard deviation, beta, and nonsystematic standard deviation of the portfolio. 4. Assume...

Compute the expected return, standard deviation, beta, and nonsystematic standard deviation of the portfolio. 4. Assume that the total market value of an initial portfolio is $300,000. Suppose that the owner of this portfolio wishes to decrease risk by reducing the allocation to the risky portfolio from y = 0.7 to y = 0.56. How do you reallocate your risky portfolio? 5. Which of the following factors reflect pure market risk for a given corporation? a. Increased short-term interest rates....

Compute the expected return, standard deviation, beta, and nonsystematic standard deviation of the portfolio. 4. Assume that the total market value of an initial portfolio is $300,000. Suppose that the owner of this portfolio wishes to decrease risk by reducing the allocation to the risky portfolio from y = 0.7 to y = 0.56. How do you reallocate your risky portfolio? 5. Which of the following factors reflect pure market risk for a given corporation? a. Increased short-term interest rates....

1. The riskless interest rate is 2%. You hold a portfolio consisting of short-term safe assets...

1. The riskless interest rate is 2%. You hold a portfolio consisting of short-term safe assets and the market portfolio of risky assets, which has a mean return of 7% and a standard deviation of 20%. You are considering the stock of Microsoft Inc. that you believe to have a beta of 1.2 with the market portfolio, and a standard deviation of return of 30%. a) What is the standard deviation of the idiosyncratic component of Microsoft's return (the residual...

1. The riskless interest rate is 2%. You hold a portfolio consisting of short-term safe assets and the market portfolio of risky assets, which has a mean return of 7% and a standard deviation of 20%. You are considering the stock of Microsoft Inc. that you believe to have a beta of 1.2 with the market portfolio, and a standard deviation of return of 30%. a) What is the standard deviation of the idiosyncratic component of Microsoft's return (the residual...

Stock A has an expected return of 11 percent, a beta of 0.9, and a standard deviation of 15 perce...

Stock A has an expected return of 11 percent, a beta of 0.9, and a standard deviation of 15 percent Stock B also has a beta of 0.9, but its expected returm is 9 percent and its standard deviation is 13 percent. Portfolio AB has $900,000 invested in Stock A and $300,000 invested in Stock B. The correlation between the two stocks' returns is zero. Which of the following statements is CORRECT? Select one O a.I am not sure b....

Stock A has an expected return of 11 percent, a beta of 0.9, and a standard deviation of 15 percent Stock B also has a beta of 0.9, but its expected returm is 9 percent and its standard deviation is 13 percent. Portfolio AB has $900,000 invested in Stock A and $300,000 invested in Stock B. The correlation between the two stocks' returns is zero. Which of the following statements is CORRECT? Select one O a.I am not sure b....

Problem 1 2pts] According to the CAPM, what is the expected return of the stock with...

Problem 1 2pts] According to the CAPM, what is the expected return of the stock with the standard deviation of the returns of 40% and the correlation between its returns and the market returns is -0.12 The market's expected return and standard deviation are 6% and 15%, respectively. The risk-free rate is 30 Problem 2 The risk-free rate is 1% and the market risk premium is 6%. Below table slows the ru characteristics of three stocks A, B, and C:...

Problem 1 2pts] According to the CAPM, what is the expected return of the stock with the standard deviation of the returns of 40% and the correlation between its returns and the market returns is -0.12 The market's expected return and standard deviation are 6% and 15%, respectively. The risk-free rate is 30 Problem 2 The risk-free rate is 1% and the market risk premium is 6%. Below table slows the ru characteristics of three stocks A, B, and C:...

(a) Suppose that the CAPM holds. Consider stocks A, B, C and D plotted in the graph below together with portfolios X, T (the tangency or market portfolio), Z, and the risk-free asset S. No explanation...

(a) Suppose that the CAPM holds. Consider stocks A, B, C and D

plotted in the graph below together with portfolios X, T (the

tangency or market portfolio), Z, and the risk-free asset S. No

explanation necessary.

(i) If you could invest in the risk-free asset S and only one of

the stocks A, B, C or D, which stock would you choose?

(ii) Which of the stocks, A, B, C, or D, has the highest

beta?

(iii) Which of...

(a) Suppose that the CAPM holds. Consider stocks A, B, C and D

plotted in the graph below together with portfolios X, T (the

tangency or market portfolio), Z, and the risk-free asset S. No

explanation necessary.

(i) If you could invest in the risk-free asset S and only one of

the stocks A, B, C or D, which stock would you choose?

(ii) Which of the stocks, A, B, C, or D, has the highest

beta?

(iii) Which of...

Stock X has an expected return of 15%, standard deviation of 20%, beta of 0.8. Stock...

Stock X has an expected return of 15%, standard deviation of 20%, beta of 0.8. Stock Y has an expected return of 20%, a standard deviation of 40% and a beta of 0.3, and a correlation with stock X of 0.6. Assume the CAPM holds. a. If you are a typical, risk-averse investor with a well-diversified portfolio, which stock would you prefer? b. What are the expected return and standard deviation of a portfolio consisting of 30% of stock X...

Stock X has an expected return of 15%, standard deviation of 20%, beta of 0.8. Stock Y has an expected return of 20%, a standard deviation of 40% and a beta of 0.3, and a correlation with stock X of 0.6. Assume the CAPM holds. a. If you are a typical, risk-averse investor with a well-diversified portfolio, which stock would you prefer? b. What are the expected return and standard deviation of a portfolio consisting of 30% of stock X...

(The following information applies to Questions 3 and 4) You observe the following information in a market where the CAPM holds: beta Expected return Annual standard deviation Stock A 1.5 15.0% 0.25 Stock B 1.2 13.2% 0.30 The correlation co

(The following information applies to Questions 3 and 4)You observe the following information in a market where the CAPM holds:betaExpected returnAnnual standard deviationStock A1.515.0%0.25Stock B1.213.2%0.30The correlation coefficient between stock A and the market is 60%. Question 3:Compute the expected return on the market portfolio.Question 4:What is the expected return of a portfolio that is split (perhaps unevenly) between the risk-free asset and the market, if this portfolio has a standard deviation of 0.07?

4. Stock A has the expected return of 12%, the standard deviation of 15%, and the...

4. Stock A has the expected return of 12%, the standard deviation of 15%, and the CAPM beta of 0.5. Stock B has the expected return of 18%, the standard deviation of 20% and the CAPM beta of 1.1. The risk-free rate is 3%. If you have no other wealth could invest in some combination of the risk-free asset and only one of these two stocks, which of the stocks A and B will you choose and why? (1 point)

4. Stock A has the expected return of 12%, the standard deviation of 15%, and the CAPM beta of 0.5. Stock B has the expected return of 18%, the standard deviation of 20% and the CAPM beta of 1.1. The risk-free rate is 3%. If you have no other wealth could invest in some combination of the risk-free asset and only one of these two stocks, which of the stocks A and B will you choose and why? (1 point)

2. Consider a market with only two risky stocks, A and B, and one risk-free asset....

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

Assume a setting in which the risk-free rate is 4% and the CAPM holds. The market portfolio has a mean return of 16% and a return standard deviation of 30%. The data on two stocks that exist in this market are as follows. Stock X has a mean return of 10% and a standard deviation of 40%. Stock Y has a mean return of 20% and a standard deviation of 50%. The pair of stocks have a return correlation of...

Assume a setting in which the risk-free rate is 4% and the CAPM holds. The market portfolio has a mean return of 16% and a return standard deviation of 30%. The data on two stocks that exist in this market are as follows. Stock X has a mean return of 10% and a standard deviation of 40%. Stock Y has a mean return of 20% and a standard deviation of 50%. The pair of stocks have a return correlation of...

Compute the expected return, standard deviation, beta, and nonsystematic standard deviation of the portfolio. 4. Assume that the total market value of an initial portfolio is $300,000. Suppose that the owner of this portfolio wishes to decrease risk by reducing the allocation to the risky portfolio from y = 0.7 to y = 0.56. How do you reallocate your risky portfolio? 5. Which of the following factors reflect pure market risk for a given corporation? a. Increased short-term interest rates....

Compute the expected return, standard deviation, beta, and nonsystematic standard deviation of the portfolio. 4. Assume that the total market value of an initial portfolio is $300,000. Suppose that the owner of this portfolio wishes to decrease risk by reducing the allocation to the risky portfolio from y = 0.7 to y = 0.56. How do you reallocate your risky portfolio? 5. Which of the following factors reflect pure market risk for a given corporation? a. Increased short-term interest rates....

1. The riskless interest rate is 2%. You hold a portfolio consisting of short-term safe assets and the market portfolio of risky assets, which has a mean return of 7% and a standard deviation of 20%. You are considering the stock of Microsoft Inc. that you believe to have a beta of 1.2 with the market portfolio, and a standard deviation of return of 30%. a) What is the standard deviation of the idiosyncratic component of Microsoft's return (the residual...

1. The riskless interest rate is 2%. You hold a portfolio consisting of short-term safe assets and the market portfolio of risky assets, which has a mean return of 7% and a standard deviation of 20%. You are considering the stock of Microsoft Inc. that you believe to have a beta of 1.2 with the market portfolio, and a standard deviation of return of 30%. a) What is the standard deviation of the idiosyncratic component of Microsoft's return (the residual...

Stock A has an expected return of 11 percent, a beta of 0.9, and a standard deviation of 15 percent Stock B also has a beta of 0.9, but its expected returm is 9 percent and its standard deviation is 13 percent. Portfolio AB has $900,000 invested in Stock A and $300,000 invested in Stock B. The correlation between the two stocks' returns is zero. Which of the following statements is CORRECT? Select one O a.I am not sure b....

Stock A has an expected return of 11 percent, a beta of 0.9, and a standard deviation of 15 percent Stock B also has a beta of 0.9, but its expected returm is 9 percent and its standard deviation is 13 percent. Portfolio AB has $900,000 invested in Stock A and $300,000 invested in Stock B. The correlation between the two stocks' returns is zero. Which of the following statements is CORRECT? Select one O a.I am not sure b....

Problem 1 2pts] According to the CAPM, what is the expected return of the stock with the standard deviation of the returns of 40% and the correlation between its returns and the market returns is -0.12 The market's expected return and standard deviation are 6% and 15%, respectively. The risk-free rate is 30 Problem 2 The risk-free rate is 1% and the market risk premium is 6%. Below table slows the ru characteristics of three stocks A, B, and C:...

Problem 1 2pts] According to the CAPM, what is the expected return of the stock with the standard deviation of the returns of 40% and the correlation between its returns and the market returns is -0.12 The market's expected return and standard deviation are 6% and 15%, respectively. The risk-free rate is 30 Problem 2 The risk-free rate is 1% and the market risk premium is 6%. Below table slows the ru characteristics of three stocks A, B, and C:...

(a) Suppose that the CAPM holds. Consider stocks A, B, C and D

plotted in the graph below together with portfolios X, T (the

tangency or market portfolio), Z, and the risk-free asset S. No

explanation necessary.

(i) If you could invest in the risk-free asset S and only one of

the stocks A, B, C or D, which stock would you choose?

(ii) Which of the stocks, A, B, C, or D, has the highest

beta?

(iii) Which of...

(a) Suppose that the CAPM holds. Consider stocks A, B, C and D

plotted in the graph below together with portfolios X, T (the

tangency or market portfolio), Z, and the risk-free asset S. No

explanation necessary.

(i) If you could invest in the risk-free asset S and only one of

the stocks A, B, C or D, which stock would you choose?

(ii) Which of the stocks, A, B, C, or D, has the highest

beta?

(iii) Which of...

Stock X has an expected return of 15%, standard deviation of 20%, beta of 0.8. Stock Y has an expected return of 20%, a standard deviation of 40% and a beta of 0.3, and a correlation with stock X of 0.6. Assume the CAPM holds. a. If you are a typical, risk-averse investor with a well-diversified portfolio, which stock would you prefer? b. What are the expected return and standard deviation of a portfolio consisting of 30% of stock X...

Stock X has an expected return of 15%, standard deviation of 20%, beta of 0.8. Stock Y has an expected return of 20%, a standard deviation of 40% and a beta of 0.3, and a correlation with stock X of 0.6. Assume the CAPM holds. a. If you are a typical, risk-averse investor with a well-diversified portfolio, which stock would you prefer? b. What are the expected return and standard deviation of a portfolio consisting of 30% of stock X...

4. Stock A has the expected return of 12%, the standard deviation of 15%, and the CAPM beta of 0.5. Stock B has the expected return of 18%, the standard deviation of 20% and the CAPM beta of 1.1. The risk-free rate is 3%. If you have no other wealth could invest in some combination of the risk-free asset and only one of these two stocks, which of the stocks A and B will you choose and why? (1 point)

4. Stock A has the expected return of 12%, the standard deviation of 15%, and the CAPM beta of 0.5. Stock B has the expected return of 18%, the standard deviation of 20% and the CAPM beta of 1.1. The risk-free rate is 3%. If you have no other wealth could invest in some combination of the risk-free asset and only one of these two stocks, which of the stocks A and B will you choose and why? (1 point)

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago