help me with this please no excel please

Homework Answers

Calculating Beta of PE-Waters

| Year | Market Return (Rm) | PE-Waters Return (Rx) |  |

|

|

|

| 2008 | 7.5 | 4.5 | 7.875 | 8.5 | 66.9375 | 62.0156 |

| 2009 | -30 | -31.5 | -29.625 | -27.5 | 814.6875 | 877.6406 |

| 2010 | 9.5 | 6 | 9.875 | 10 | 98.75 | 97.5156 |

| 2011 | 11.5 | 5 | 11.875 | 9 | 106.875 | 141.0156 |

| -1.5 | -16 | 1087.25 | 1178.1875 | |||

| ΣRm | ΣRx |  |

|

Computing Standard Deviation of Market

= 1178.1875/4

= 294.55

Computing Covariance of Market and PE-Water Security Return

= 1087.25/4

=271.8125

Now, Calculating Beta of Security using Standard Deviation of Market and Covariance of Market and PE-Water Security Return:

= 271.8125/294.55

Beta of Security= 0.923

So, PE- Waters Beta is closest to option(c) which is 0.927.

Add Answer to:

help me with this please no excel please

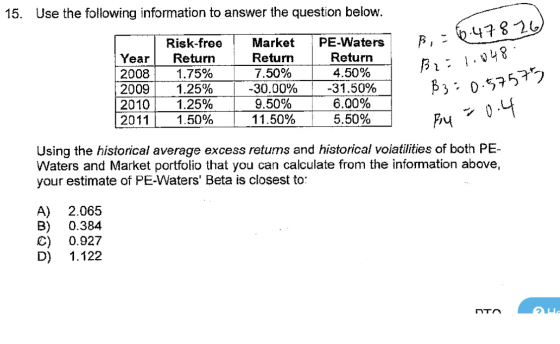

15. Use the following information to answer the...

How to calculate B when there is many risk free? • Use the following information to...

How to calculate B when there is many risk free?

• Use the following information to answer the question below. Year 2008 2009 2010 2011 Risk-free Return 1.75% 1.25% 1.25% 1.50% Market Return 7.50% -30.00% 9.50% 11.50% PE-Waters Return 4.50% -31.50% 6.00% 5.50% Using the historical average excess retums and historical volatilities of both PE- Waters and Market portfolio that you can calculate from the information above, your estimate of PE-Waters' Beta is closest to: A) 2.065 0.384 0.927 1.122...

How to calculate B when there is many risk free?

• Use the following information to answer the question below. Year 2008 2009 2010 2011 Risk-free Return 1.75% 1.25% 1.25% 1.50% Market Return 7.50% -30.00% 9.50% 11.50% PE-Waters Return 4.50% -31.50% 6.00% 5.50% Using the historical average excess retums and historical volatilities of both PE- Waters and Market portfolio that you can calculate from the information above, your estimate of PE-Waters' Beta is closest to: A) 2.065 0.384 0.927 1.122...

How to calculate B when there is many risk free?

• Use the following information to answer the question below. Year 2008 2009 2010 2011 Risk-free Return 1.75% 1.25% 1.25% 1.50% Market Return 7.50% -30.00% 9.50% 11.50% PE-Waters Return 4.50% -31.50% 6.00% 5.50% Using the historical average excess retums and historical volatilities of both PE- Waters and Market portfolio that you can calculate from the information above, your estimate of PE-Waters' Beta is closest to: A) 2.065 0.384 0.927 1.122...

How to calculate B when there is many risk free?

• Use the following information to answer the question below. Year 2008 2009 2010 2011 Risk-free Return 1.75% 1.25% 1.25% 1.50% Market Return 7.50% -30.00% 9.50% 11.50% PE-Waters Return 4.50% -31.50% 6.00% 5.50% Using the historical average excess retums and historical volatilities of both PE- Waters and Market portfolio that you can calculate from the information above, your estimate of PE-Waters' Beta is closest to: A) 2.065 0.384 0.927 1.122...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago