Kenworth Company uses a job-order costing system. Only three jobs—Job 105, Job 106, and Job 107—were worked on during November and December. Job 105 was completed on December 10; the other two jobs were still in production on December 31, the end of the company’s operating year. Data from the job cost sheets of the three jobs follow:

| Job Cost Sheet | |||||||||

| Job 105 | Job 106 | Job 107 | |||||||

| November costs incurred: | |||||||||

| Direct materials | $ | 19,900 | $ | 12,700 | $ | 0 | |||

| Direct labour | $ | 16,400 | $ | 10,400 | $ | 0 | |||

| Manufacturing overhead | $ | 24,600 | $ | 15,600 | $ | 0 | |||

| December costs incurred: | |||||||||

| Direct materials | $ | 0 | $ | 9,900 | $ | 28,100 | |||

| Direct labour | $ | 6,550 | $ | 7,700 | $ | 13,400 | |||

| Manufacturing overhead | ? | ? | ? | ||||||

The following additional information is available:

- Manufacturing overhead is applied to jobs on the basis of direct labour cost.

- Balances in the inventory accounts at November 30 were as follows:

| Raw Materials | $ | 50,200 | |

| Work in Process | ? | ||

| Finished Goods | $ | 102,000 | |

Homework Answers

| Job cost sheet | |||||||||

| Job 105 | Job 106 | Job 107 | total | ||||||

| November costs incurred: | |||||||||

| Direct materials | 19,900 | 12,700 | 0 | 32,600 | |||||

| Direct labor | 16,400 | 10,400 | 0 | 26,800 | |||||

| Manufacturing overhead | 24,600 | 15,600 | 0 | 40,200 | |||||

| Total Beginning WIP | 60,900 | 38,700 | 0 | 99,600 | |||||

| December costs incurred: | |||||||||

| Direct materials | 0 | 9,900 | 28,100 | 38,000 | |||||

| Direct labor | 6,550 | 7,700 | 13,400 | 27,650 | |||||

| Manufacturing overhead | 9825 | 11550 | 20100 | 41,475 | |||||

| cost added during december | 16,375 | 29,150 | 61,600 | 107,125 | |||||

| total cost of job | 77,275 | 67,850 | 61,600 | 206,725 | |||||

| 1) | T-Accounts | ||||||||

| Raw materials | Work in progress | ||||||||

| Beg.bal | 50,200 | Beg bal | 99,600 | ||||||

| 44,550 | a) | a) | 38,000 | 77,275 | e) | ||||

| b) | 27,650 | ||||||||

| End bal | d) | 41,475 | |||||||

| End bal | 129,450 | ||||||||

| Finished goods | Manufacturing overhead | ||||||||

| Beg.Bal | 102,000 | Beg.Bal | 0 | ||||||

| e) | 77,275 | a) | 6,550 | 41,475 | d) | ||||

| b) | 11,400 | ||||||||

| End bal | 179,275 | c) | 20,825 | ||||||

| End bal | 2,700 | ||||||||

| Salaries & wages payable | Accounts payable | ||||||||

| Beg bal | Beg bal | ||||||||

| 39,050 | b) | 20,825 | c) | ||||||

| End bal | end bal | ||||||||

| 2) | Event | General Journl | Debit | Credit | |||||

| a) | 1) | Work in process | 38,000 | ||||||

| Manufacturing overhead | 6,550 | ||||||||

| Raw Materials | 44,550 | ||||||||

| b) | 2) | Work in process | 27,650 | ||||||

| Manufacturing overhead | 11,400 | ||||||||

| Salaries & wages payable | 39,050 | ||||||||

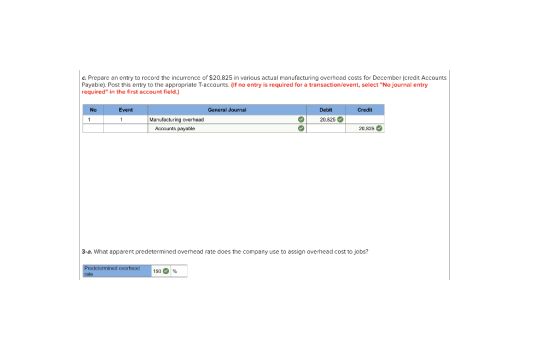

| c) | 3) | Manufacturing overhead | 20,825 | ||||||

| Accounts payable | 20,825 | ||||||||

| 3a) | predetermined overhead rate | 150% | |||||||

| 3b) | Work in process | 41,475 | |||||||

| Manufacturing ovehead | 41,475 | ||||||||

| 4) | Finished goods | 77,275 | |||||||

| Work in process inventory | 77,275 | ||||||||

| 5) | Job 106 | job 107 | total | ||||||

| Direct materials | 22,600 | 28,100 | 50,700 | ||||||

| direct labor | 18,100 | 13,400 | 31,500 | ||||||

| manufacturing overhead | 27,150 | 20100 | 47,250 | ||||||

| Total cost | 67,850 | 61,600 | 129,450 | ||||||

Add Answer to:

Kenworth Company uses a job-order costing system. Only three

jobs—Job 105, Job 106, and Job 107—were...

Kenworth Company uses a job-order costing system. Only three jobs—Job 105, Job 106, and Job 107—were...

Kenworth Company uses a job-order costing system. Only three

jobs—Job 105, Job 106, and Job 107—were worked on during November

and December. Job 105 was completed on December 10; the other two

jobs were still in production on December 31, the end of the

company’s operating year. Data from the job cost sheets of the

three jobs follow:

Job Cost Sheet

Job 105

Job 106

Job 107

November costs incurred:

Direct materials

$

20,500

$

13,300

$

0...

Kenworth Company uses a job-order costing system. Only three

jobs—Job 105, Job 106, and Job 107—were worked on during November

and December. Job 105 was completed on December 10; the other two

jobs were still in production on December 31, the end of the

company’s operating year. Data from the job cost sheets of the

three jobs follow:

Job Cost Sheet

Job 105

Job 106

Job 107

November costs incurred:

Direct materials

$

20,500

$

13,300

$

0...

Ravsten Company uses a job-order costing system. On January 1, the beginning of the current year, the company's...

Ravsten Company uses a job-order costing system. On January 1, the beginning of the current year, the company's inventory balances were as follows: Raw materials Work in process Finished goods $16,500 $10,200 $30, 100 The company applies overhead cost to jobs on the basis of machine-hours. For the current year, the company estimated that it would work 36.100 machine-hours and incur $155.230 in manufacturing overhead cost. The following transactions were recorded for the year: a. Raw materials were purchased on...

Ravsten Company uses a job-order costing system. On January 1, the beginning of the current year, the company's inventory balances were as follows: Raw materials Work in process Finished goods $16,500 $10,200 $30, 100 The company applies overhead cost to jobs on the basis of machine-hours. For the current year, the company estimated that it would work 36.100 machine-hours and incur $155.230 in manufacturing overhead cost. The following transactions were recorded for the year: a. Raw materials were purchased on...

ACC378 Cost Accounting Assignment CH5 Perry Company employs a job-order costing system. Only three jobs-Job #205,...

ACC378 Cost Accounting Assignment CH5 Perry Company employs a job-order costing system. Only three jobs-Job #205, Job # 206, and Job #207- were worked on during January and February. Job #205 was completed February 10; the other two jobs were still in production on February 28, the end of the company's operating year. Job cost sheets on the three jobs follow: Job Cost Sheet Job #206 Job #205 Job #207 Totals January costs incurred: Direct material $16,500 13,000 20,800 $...

ACC378 Cost Accounting Assignment CH5 Perry Company employs a job-order costing system. Only three jobs-Job #205, Job # 206, and Job #207- were worked on during January and February. Job #205 was completed February 10; the other two jobs were still in production on February 28, the end of the company's operating year. Job cost sheets on the three jobs follow: Job Cost Sheet Job #206 Job #205 Job #207 Totals January costs incurred: Direct material $16,500 13,000 20,800 $...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $211,000. b. Raw materials used in production, $192,000 ($153,600 direct materials and $38,400 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $211,000. b. Raw materials used in production, $192,000 ($153,600 direct materials and $38,400 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

Ravsten Company uses a job-order costing system. On January 1, the beginning of the current year,...

Ravsten Company uses a job-order costing system. On January 1, the beginning of the current year, the company's inventory balances were as follows: Raw materials Work in process Finished goods $21, 500 $12, 200 $31, 100 The company applies overhead cost to jobs on the basis of machine-hours. For the current year, the company estimated that it would work 37,100 machine-hours and incur $150,255 in manufacturing overhead cost. The following transactions were recorded for the year: a. Raw materials were...

Ravsten Company uses a job-order costing system. On January 1, the beginning of the current year, the company's inventory balances were as follows: Raw materials Work in process Finished goods $21, 500 $12, 200 $31, 100 The company applies overhead cost to jobs on the basis of machine-hours. For the current year, the company estimated that it would work 37,100 machine-hours and incur $150,255 in manufacturing overhead cost. The following transactions were recorded for the year: a. Raw materials were...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: ES a....

The Polaris Company uses a job-order costing system. The following transactions occurred in October: ES a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $190,000 ($152,000 direct materials and $38,000 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $129,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $6...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: ES a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $190,000 ($152,000 direct materials and $38,000 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $129,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $6...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $190,000 ($152,000 direct materials and $38,000 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $20,000. d. Depreciation recorded on factory equipment, $104,000. e. Other manufacturing overhead costs accrued during October, $131,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $5 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $190,000 ($152,000 direct materials and $38,000 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $20,000. d. Depreciation recorded on factory equipment, $104,000. e. Other manufacturing overhead costs accrued during October, $131,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $5 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $209,000. b. Raw materials used in production, $192,000 ($153,600 direct materials and $38,400 indirect materials). c. Accrued direct labor cost of $49,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $9 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $209,000. b. Raw materials used in production, $192,000 ($153,600 direct materials and $38,400 indirect materials). c. Accrued direct labor cost of $49,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $9 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $189,000 ($151,200 direct materials and $37,800 indirect materials). C. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $106,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $189,000 ($151,200 direct materials and $37,800 indirect materials). C. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $106,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $209,000. b. Raw materials used in production, $191,000 ($152,800 direct materials and $38,200 indirect materials). C. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $104,000. e. Other manufacturing overhead costs accrued during October, $129,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $209,000. b. Raw materials used in production, $191,000 ($152,800 direct materials and $38,200 indirect materials). C. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $104,000. e. Other manufacturing overhead costs accrued during October, $129,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

Kenworth Company uses a job-order costing system. Only three

jobs—Job 105, Job 106, and Job 107—were worked on during November

and December. Job 105 was completed on December 10; the other two

jobs were still in production on December 31, the end of the

company’s operating year. Data from the job cost sheets of the

three jobs follow:

Job Cost Sheet

Job 105

Job 106

Job 107

November costs incurred:

Direct materials

$

20,500

$

13,300

$

0...

Kenworth Company uses a job-order costing system. Only three

jobs—Job 105, Job 106, and Job 107—were worked on during November

and December. Job 105 was completed on December 10; the other two

jobs were still in production on December 31, the end of the

company’s operating year. Data from the job cost sheets of the

three jobs follow:

Job Cost Sheet

Job 105

Job 106

Job 107

November costs incurred:

Direct materials

$

20,500

$

13,300

$

0...

Ravsten Company uses a job-order costing system. On January 1, the beginning of the current year, the company's inventory balances were as follows: Raw materials Work in process Finished goods $16,500 $10,200 $30, 100 The company applies overhead cost to jobs on the basis of machine-hours. For the current year, the company estimated that it would work 36.100 machine-hours and incur $155.230 in manufacturing overhead cost. The following transactions were recorded for the year: a. Raw materials were purchased on...

Ravsten Company uses a job-order costing system. On January 1, the beginning of the current year, the company's inventory balances were as follows: Raw materials Work in process Finished goods $16,500 $10,200 $30, 100 The company applies overhead cost to jobs on the basis of machine-hours. For the current year, the company estimated that it would work 36.100 machine-hours and incur $155.230 in manufacturing overhead cost. The following transactions were recorded for the year: a. Raw materials were purchased on...

ACC378 Cost Accounting Assignment CH5 Perry Company employs a job-order costing system. Only three jobs-Job #205, Job # 206, and Job #207- were worked on during January and February. Job #205 was completed February 10; the other two jobs were still in production on February 28, the end of the company's operating year. Job cost sheets on the three jobs follow: Job Cost Sheet Job #206 Job #205 Job #207 Totals January costs incurred: Direct material $16,500 13,000 20,800 $...

ACC378 Cost Accounting Assignment CH5 Perry Company employs a job-order costing system. Only three jobs-Job #205, Job # 206, and Job #207- were worked on during January and February. Job #205 was completed February 10; the other two jobs were still in production on February 28, the end of the company's operating year. Job cost sheets on the three jobs follow: Job Cost Sheet Job #206 Job #205 Job #207 Totals January costs incurred: Direct material $16,500 13,000 20,800 $...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $211,000. b. Raw materials used in production, $192,000 ($153,600 direct materials and $38,400 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $211,000. b. Raw materials used in production, $192,000 ($153,600 direct materials and $38,400 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

Ravsten Company uses a job-order costing system. On January 1, the beginning of the current year, the company's inventory balances were as follows: Raw materials Work in process Finished goods $21, 500 $12, 200 $31, 100 The company applies overhead cost to jobs on the basis of machine-hours. For the current year, the company estimated that it would work 37,100 machine-hours and incur $150,255 in manufacturing overhead cost. The following transactions were recorded for the year: a. Raw materials were...

Ravsten Company uses a job-order costing system. On January 1, the beginning of the current year, the company's inventory balances were as follows: Raw materials Work in process Finished goods $21, 500 $12, 200 $31, 100 The company applies overhead cost to jobs on the basis of machine-hours. For the current year, the company estimated that it would work 37,100 machine-hours and incur $150,255 in manufacturing overhead cost. The following transactions were recorded for the year: a. Raw materials were...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: ES a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $190,000 ($152,000 direct materials and $38,000 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $129,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $6...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: ES a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $190,000 ($152,000 direct materials and $38,000 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $129,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $6...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $190,000 ($152,000 direct materials and $38,000 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $20,000. d. Depreciation recorded on factory equipment, $104,000. e. Other manufacturing overhead costs accrued during October, $131,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $5 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $190,000 ($152,000 direct materials and $38,000 indirect materials). c. Accrued direct labor cost of $50,000 and indirect labor cost of $20,000. d. Depreciation recorded on factory equipment, $104,000. e. Other manufacturing overhead costs accrued during October, $131,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $5 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $209,000. b. Raw materials used in production, $192,000 ($153,600 direct materials and $38,400 indirect materials). c. Accrued direct labor cost of $49,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $9 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $209,000. b. Raw materials used in production, $192,000 ($153,600 direct materials and $38,400 indirect materials). c. Accrued direct labor cost of $49,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $105,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $9 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $189,000 ($151,200 direct materials and $37,800 indirect materials). C. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $106,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $210,000. b. Raw materials used in production, $189,000 ($151,200 direct materials and $37,800 indirect materials). C. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $106,000. e. Other manufacturing overhead costs accrued during October, $130,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $209,000. b. Raw materials used in production, $191,000 ($152,800 direct materials and $38,200 indirect materials). C. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $104,000. e. Other manufacturing overhead costs accrued during October, $129,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

The Polaris Company uses a job-order costing system. The following transactions occurred in October: a. Raw materials purchased on account, $209,000. b. Raw materials used in production, $191,000 ($152,800 direct materials and $38,200 indirect materials). C. Accrued direct labor cost of $50,000 and indirect labor cost of $21,000. d. Depreciation recorded on factory equipment, $104,000. e. Other manufacturing overhead costs accrued during October, $129,000. f. The company applies manufacturing overhead cost to production using a predetermined rate of $10 per...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago