Homework Answers

1)

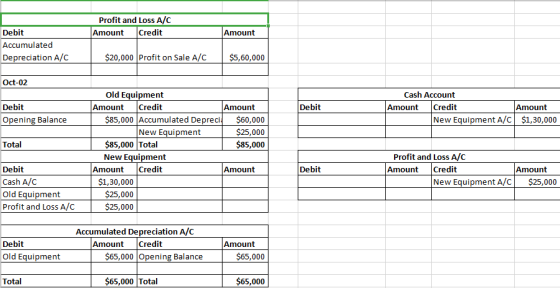

Note -1

Building:

| S.No | Particulars | Amount | ||

| A | Purchase Cost (A) | $8,00,000 | ||

| B | Useful Life ( Years ) (B) | 20 | ||

| C | Residual Value (C) | $0 | ||

| D | Depreciable Value (D = A-C) | $8,00,000 | ||

| E | Depreciation Per Anum (E = A/B) | $40,000 | ||

| F | Depreciation from Dec'31st to July 1st (E*6)/12 | $20,000 | ||

| G | Total Accumulated Depreciation ( $400000 + $20000) | $4,20,000 | ||

| H | Book Value on the date of sale (A-G) | $3,80,000 | ||

| I | Sale Cosideration | $9,40,000 | ||

| J | Profit on Sale (I - H) | $5,60,000 | ||

2)

Equipment :

| S.No | Particulars | Amount | ||

| A | Purchase Cost (A) | $1,60,000 | ||

| B | Useful Life ( Years ) (B) | 5 | ||

| C | Residual Value (C) | $10,000 | ||

| D | Depreciable Value (D = A-C) | $1,60,000 | ||

| E | Depreciation Per Anum (E = A/B) | $32,000 | ||

| F | Depreciation Rate | 20% | ||

| G | Tripple Depreciation Rate | 60% | ||

| H | Depreciation Expense(D*G) | $96,000 | ||

| Equipment | ||||||||

| Accumulated Depreciation A/C | Depreciation A/C | |||||||

| Debit | Amount | Credit | Amount | Debit | Amount | Credit | Amount | |

| Depreciation A/C | $96,000 | Profit and Loss A/C | $96,000 | Accumulated Depreciation A/C | $96,000 | |||

Coal Field :

| Units of Production Method of Depreciation ( Amount in $ ) | |||||||

| Year |

Cost (A) |

Depreciable Amount (B) |

Total Capacity ( Tons ) (C) |

Units Produced in the Year (D) |

Depreciation Per Year (E)=(B)/(C) * |

Accumulated Depreciatoin(F) |

Carrying Value (G) = (A)-(F) |

| 1 | $20,00,000 | 2000000 | 40000 | 3000 | $1,50,000 | $1,50,000 | $18,50,000 |

| Coal Field | ||||||||

| Accumulated Depreciation A/C | Depreciation A/C | |||||||

| Debit | Amount | Credit | Amount | Debit | Amount | Credit | Amount | |

| Depreciation A/C | $1,50,000 | Profit and Loss A/C | $1,50,000 | Accumulated Depreciation A/C | $1,50,000 | |||

Copy Right:

| S.No | Particulars | Amount | ||

| A | Purchase Cost (A) | $1,20,000 | ||

| B | Useful Life ( Years ) (B) | 4 | ||

| C | Residual Value (C) | $0 | ||

| D | Depreciable Value (D = A-C) | $1,20,000 | ||

| E | Depreciation Per Anum (E = A/B) | $30,000 | ||

| Depreciation Expense (E *302/365 days) | $24,822 | |||

| Copyright | ||||||||

| Accumulated Depreciation A/C | Depreciation A/C | |||||||

| Debit | Amount | Credit | Amount | Debit | Amount | Credit | Amount | |

| Depreciation A/C | $24,822 | Profit and Loss A/C | $24,822 | Accumulated Depreciation A/C | $24,822 | |||

Patents:

| S.No | Particulars | Amount | ||

| A | Purchase Cost (A) | $12,000 | ||

| B | Useful Life ( Years ) (B) | 5 | ||

| C | Residual Value (C) | $0 | ||

| D | Depreciable Value (D = A-C) | $12,000 | ||

| E | Depreciation Per Anum (E = A/B) | $2,400 | ||

| Depreciation Expense (E *241/365 days) | $1,585 | |||

| Patent | ||||||||

| Accumulated Depreciation A/C | Depreciation A/C | |||||||

| Debit | Amount | Credit | Amount | Debit | Amount | Credit | Amount | |

| Depreciation A/C | $1,585 | Profit and Loss A/C | $1,585 | Accumulated Depreciation A/C | $1,585 | |||

New Equipment:

| S.No | Particulars | Amount | ||

| A | Purchase Cost (A) | $1,80,000 | ||

| B | Useful Life ( Years ) (B) | 6 | ||

| C | Residual Value (C) | $0 | ||

| D | Depreciable Value (D = A-C) | $1,80,000 | ||

| E | Depreciation Per Anum (E = A/B) | $30,000 | ||

| Depreciation Expense (E *90/365 days) | $7,397 | |||

| New Equipment | ||||||||

| Accumulated Depreciation A/C | Depreciation A/C | |||||||

| Debit | Amount | Credit | Amount | Debit | Amount | Credit | Amount | |

| Depreciation A/C | $7,397 | Profit and Loss A/C | $7,397 | Accumulated Depreciation A/C | $7,397 | |||

Add Answer to:

Problems for Section 8B 8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment,...

Problems for Section 8B 8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment,...

Problems for Section 8B 8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents, Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 March 4 May 5 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120,000 cash. Purchased a patent and...

Problems for Section 8B 8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents, Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 March 4 May 5 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120,000 cash. Purchased a patent and...

8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents. Copyrights, and Coal...

8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents. Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120.000 cash. Purchased a patent and a piece of land for a lump sum...

8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents. Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120.000 cash. Purchased a patent and a piece of land for a lump sum...

requirement 2 Plz Problems for Section 8B 8B-1. RASPBERRY Corporation's chart of accounts includes the following...

requirement 2 Plz

Problems for Section 8B 8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents, Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120,000 cash. Purchased a patent and a...

requirement 2 Plz

Problems for Section 8B 8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents, Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120,000 cash. Purchased a patent and a...

4. Tarrier, Inc., has the following PPE account: Land, Building, and Equipment, with a separate accumulated...

4. Tarrier, Inc., has the following PPE account: Land, Building, and Equipment, with a separate accumulated depreciation account for each of these except land. Tarrier completed the following transactions: (12marks) Traded in equipment with accumulated depreciation of $65,000(cost of$ 139,000) for similar new equipment with a cash cost of $ 179,000. Received a trade-in allowance of $73,000 on the old equipment and paid $106,000 in cash Jan 2 Sold a building that had a cost of $635,000 and had accumulated...

4. Tarrier, Inc., has the following PPE account: Land, Building, and Equipment, with a separate accumulated depreciation account for each of these except land. Tarrier completed the following transactions: (12marks) Traded in equipment with accumulated depreciation of $65,000(cost of$ 139,000) for similar new equipment with a cash cost of $ 179,000. Received a trade-in allowance of $73,000 on the old equipment and paid $106,000 in cash Jan 2 Sold a building that had a cost of $635,000 and had accumulated...

4) Tucker, Inc., has the following plant asset accounts: Land, Buildings, and Equipment, with a separate...

4) Tucker, Inc., has the following plant asset accounts: Land, Buildings, and Equipment, with a separate accumulated depreciation account for each of these except Land. Tucker completed the following transactions: Jan 3 Traded in equipment with accumulated depreciation of $61,000 (cost of $131,000) for similar new equipment with a cash cost of $177,000. Received a trade-in allowance of $76,000 on the old equipment and paid $101,000 in cash, Jun 30 Sold a building that had a cost of $640,000 and...

4) Tucker, Inc., has the following plant asset accounts: Land, Buildings, and Equipment, with a separate accumulated depreciation account for each of these except Land. Tucker completed the following transactions: Jan 3 Traded in equipment with accumulated depreciation of $61,000 (cost of $131,000) for similar new equipment with a cash cost of $177,000. Received a trade-in allowance of $76,000 on the old equipment and paid $101,000 in cash, Jun 30 Sold a building that had a cost of $640,000 and...

The intangible assets section of Bramble Corporation's balance sheet at December 31, 2022 is presented here....

The intangible assets section of Bramble Corporation's balance sheet at December 31, 2022 is presented here. Patents (579,900 cost less $7.990 amortization) Copyrights ($53,000 cost less $41,500 amortization) Total $73.400 11.500 $84.900 The patent was acquired in January 2022 and has a useful life of 10 years. The copyright was acquired in January 2016 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2023. Jan. 2 Pald $36,000 legal costs...

The intangible assets section of Bramble Corporation's balance sheet at December 31, 2022 is presented here. Patents (579,900 cost less $7.990 amortization) Copyrights ($53,000 cost less $41,500 amortization) Total $73.400 11.500 $84.900 The patent was acquired in January 2022 and has a useful life of 10 years. The copyright was acquired in January 2016 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2023. Jan. 2 Pald $36,000 legal costs...

Instructions Chart of Accounts ! Journal Instructions The following transactions, adjusting entries, and closing entries were...

Instructions Chart of Accounts ! Journal Instructions The following transactions, adjusting entries, and closing entries were completed by Legacy Furniture Co. during a three-year period. All are related to the use of delivery equipment. The double-declining-balance method of depreciation is used. 2014 Jan. 4. Nov. 2. Dec. 31. Purchased a used delivery truck for $28,000, paying cash. Paid garage $675 for miscellaneous repairs to the truck. Recorded depreciation on the truck for the year. The estimated useful life of the...

Instructions Chart of Accounts ! Journal Instructions The following transactions, adjusting entries, and closing entries were completed by Legacy Furniture Co. during a three-year period. All are related to the use of delivery equipment. The double-declining-balance method of depreciation is used. 2014 Jan. 4. Nov. 2. Dec. 31. Purchased a used delivery truck for $28,000, paying cash. Paid garage $675 for miscellaneous repairs to the truck. Recorded depreciation on the truck for the year. The estimated useful life of the...

Question 3 0.6 The intangible assets section of Martinez Corporation's balance sheet at December ...

Question 3 0.6 The intangible assets section of Martinez Corporation's balance sheet at December 31, 2017, is presented here. Patents ($78,100 cost less $7,810 amortization) $70.290 Copyrights ($42.000 cost less $29 400 amortization) 12600 $82,890 Total has a useful life of 10 years. The copyright was acquired in January 2011 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2018. Jan. 2 Paid $36,000 egal costs to successtully defend the...

Question 3 0.6 The intangible assets section of Martinez Corporation's balance sheet at December 31, 2017, is presented here. Patents ($78,100 cost less $7,810 amortization) $70.290 Copyrights ($42.000 cost less $29 400 amortization) 12600 $82,890 Total has a useful life of 10 years. The copyright was acquired in January 2011 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2018. Jan. 2 Paid $36,000 egal costs to successtully defend the...

The intangible assets section of Marigold Corporation's balance sheet at December 31, 2022, is presented here....

The intangible assets section of Marigold Corporation's balance sheet at December 31, 2022, is presented here. Patents ($71,800 cost less $7,180 amortization) $63,400 Copyrights ($50,500 cost less $39,400 amortization) 11,100 $74,500 Total The patent was acquired in January 2022 and has a useful life of 10 years. The copyright was acquired in January 2016 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2023. Jan Paid $45,000 legal costs to...

The intangible assets section of Marigold Corporation's balance sheet at December 31, 2022, is presented here. Patents ($71,800 cost less $7,180 amortization) $63,400 Copyrights ($50,500 cost less $39,400 amortization) 11,100 $74,500 Total The patent was acquired in January 2022 and has a useful life of 10 years. The copyright was acquired in January 2016 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2023. Jan Paid $45,000 legal costs to...

Comparing three depreciation methods Dexter Industries purchased packaging equipment on January 8 for $135,000. The equipment...

Comparing three depreciation methods Dexter Industries purchased packaging equipment on January 8 for $135,000. The equipment was expected to have a useful life of three years, or 27,000 operating hours, and a residual value of $5,400. The equipment was used for 10,800 hours during Year 1, 8,100 hours in Year 2, and 8,100 hours in Year 3. Required: 1. Determine the amount of depreciation expense for the three years ending December 31, by (a) the straight-line method, (b) the units-of-activity...

Comparing three depreciation methods Dexter Industries purchased packaging equipment on January 8 for $135,000. The equipment was expected to have a useful life of three years, or 27,000 operating hours, and a residual value of $5,400. The equipment was used for 10,800 hours during Year 1, 8,100 hours in Year 2, and 8,100 hours in Year 3. Required: 1. Determine the amount of depreciation expense for the three years ending December 31, by (a) the straight-line method, (b) the units-of-activity...

Problems for Section 8B 8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents, Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 March 4 May 5 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120,000 cash. Purchased a patent and...

Problems for Section 8B 8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents, Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 March 4 May 5 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120,000 cash. Purchased a patent and...

8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents. Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120.000 cash. Purchased a patent and a piece of land for a lump sum...

8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents. Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120.000 cash. Purchased a patent and a piece of land for a lump sum...

requirement 2 Plz

Problems for Section 8B 8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents, Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120,000 cash. Purchased a patent and a...

requirement 2 Plz

Problems for Section 8B 8B-1. RASPBERRY Corporation's chart of accounts includes the following categories: Land, Equipment, Patents, Copyrights, and Coal Reserves. RASPBERRY completed the following transactions during the year: Jan 2 Feb 3 Purchased Equipment for $140,000 cash; RASPBERRY also had to pay 10% tax and a $6,000 license fee. Purchased a coal field with 40,000 tons of coal reserves for $2,000,000 cash. Purchased a copyright from another company for $120,000 cash. Purchased a patent and a...

4. Tarrier, Inc., has the following PPE account: Land, Building, and Equipment, with a separate accumulated depreciation account for each of these except land. Tarrier completed the following transactions: (12marks) Traded in equipment with accumulated depreciation of $65,000(cost of$ 139,000) for similar new equipment with a cash cost of $ 179,000. Received a trade-in allowance of $73,000 on the old equipment and paid $106,000 in cash Jan 2 Sold a building that had a cost of $635,000 and had accumulated...

4. Tarrier, Inc., has the following PPE account: Land, Building, and Equipment, with a separate accumulated depreciation account for each of these except land. Tarrier completed the following transactions: (12marks) Traded in equipment with accumulated depreciation of $65,000(cost of$ 139,000) for similar new equipment with a cash cost of $ 179,000. Received a trade-in allowance of $73,000 on the old equipment and paid $106,000 in cash Jan 2 Sold a building that had a cost of $635,000 and had accumulated...

4) Tucker, Inc., has the following plant asset accounts: Land, Buildings, and Equipment, with a separate accumulated depreciation account for each of these except Land. Tucker completed the following transactions: Jan 3 Traded in equipment with accumulated depreciation of $61,000 (cost of $131,000) for similar new equipment with a cash cost of $177,000. Received a trade-in allowance of $76,000 on the old equipment and paid $101,000 in cash, Jun 30 Sold a building that had a cost of $640,000 and...

4) Tucker, Inc., has the following plant asset accounts: Land, Buildings, and Equipment, with a separate accumulated depreciation account for each of these except Land. Tucker completed the following transactions: Jan 3 Traded in equipment with accumulated depreciation of $61,000 (cost of $131,000) for similar new equipment with a cash cost of $177,000. Received a trade-in allowance of $76,000 on the old equipment and paid $101,000 in cash, Jun 30 Sold a building that had a cost of $640,000 and...

The intangible assets section of Bramble Corporation's balance sheet at December 31, 2022 is presented here. Patents (579,900 cost less $7.990 amortization) Copyrights ($53,000 cost less $41,500 amortization) Total $73.400 11.500 $84.900 The patent was acquired in January 2022 and has a useful life of 10 years. The copyright was acquired in January 2016 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2023. Jan. 2 Pald $36,000 legal costs...

The intangible assets section of Bramble Corporation's balance sheet at December 31, 2022 is presented here. Patents (579,900 cost less $7.990 amortization) Copyrights ($53,000 cost less $41,500 amortization) Total $73.400 11.500 $84.900 The patent was acquired in January 2022 and has a useful life of 10 years. The copyright was acquired in January 2016 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2023. Jan. 2 Pald $36,000 legal costs...

Instructions Chart of Accounts ! Journal Instructions The following transactions, adjusting entries, and closing entries were completed by Legacy Furniture Co. during a three-year period. All are related to the use of delivery equipment. The double-declining-balance method of depreciation is used. 2014 Jan. 4. Nov. 2. Dec. 31. Purchased a used delivery truck for $28,000, paying cash. Paid garage $675 for miscellaneous repairs to the truck. Recorded depreciation on the truck for the year. The estimated useful life of the...

Instructions Chart of Accounts ! Journal Instructions The following transactions, adjusting entries, and closing entries were completed by Legacy Furniture Co. during a three-year period. All are related to the use of delivery equipment. The double-declining-balance method of depreciation is used. 2014 Jan. 4. Nov. 2. Dec. 31. Purchased a used delivery truck for $28,000, paying cash. Paid garage $675 for miscellaneous repairs to the truck. Recorded depreciation on the truck for the year. The estimated useful life of the...

Question 3 0.6 The intangible assets section of Martinez Corporation's balance sheet at December 31, 2017, is presented here. Patents ($78,100 cost less $7,810 amortization) $70.290 Copyrights ($42.000 cost less $29 400 amortization) 12600 $82,890 Total has a useful life of 10 years. The copyright was acquired in January 2011 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2018. Jan. 2 Paid $36,000 egal costs to successtully defend the...

Question 3 0.6 The intangible assets section of Martinez Corporation's balance sheet at December 31, 2017, is presented here. Patents ($78,100 cost less $7,810 amortization) $70.290 Copyrights ($42.000 cost less $29 400 amortization) 12600 $82,890 Total has a useful life of 10 years. The copyright was acquired in January 2011 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2018. Jan. 2 Paid $36,000 egal costs to successtully defend the...

The intangible assets section of Marigold Corporation's balance sheet at December 31, 2022, is presented here. Patents ($71,800 cost less $7,180 amortization) $63,400 Copyrights ($50,500 cost less $39,400 amortization) 11,100 $74,500 Total The patent was acquired in January 2022 and has a useful life of 10 years. The copyright was acquired in January 2016 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2023. Jan Paid $45,000 legal costs to...

The intangible assets section of Marigold Corporation's balance sheet at December 31, 2022, is presented here. Patents ($71,800 cost less $7,180 amortization) $63,400 Copyrights ($50,500 cost less $39,400 amortization) 11,100 $74,500 Total The patent was acquired in January 2022 and has a useful life of 10 years. The copyright was acquired in January 2016 and also has a useful life of 10 years. The following cash transactions may have affected intangible assets during 2023. Jan Paid $45,000 legal costs to...

Comparing three depreciation methods Dexter Industries purchased packaging equipment on January 8 for $135,000. The equipment was expected to have a useful life of three years, or 27,000 operating hours, and a residual value of $5,400. The equipment was used for 10,800 hours during Year 1, 8,100 hours in Year 2, and 8,100 hours in Year 3. Required: 1. Determine the amount of depreciation expense for the three years ending December 31, by (a) the straight-line method, (b) the units-of-activity...

Comparing three depreciation methods Dexter Industries purchased packaging equipment on January 8 for $135,000. The equipment was expected to have a useful life of three years, or 27,000 operating hours, and a residual value of $5,400. The equipment was used for 10,800 hours during Year 1, 8,100 hours in Year 2, and 8,100 hours in Year 3. Required: 1. Determine the amount of depreciation expense for the three years ending December 31, by (a) the straight-line method, (b) the units-of-activity...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago