Homework Answers

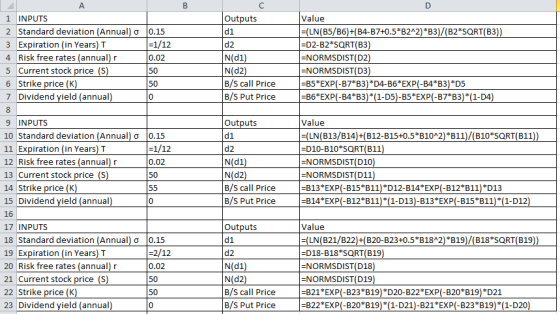

a. We can use excel in following manner to calculate the value of call option and put option:

|

INPUTS |

Outputs |

Value |

|

|

Standard deviation (Annual) σ |

15.00% |

d1 |

0.0601 |

|

Expiration (in Years) T |

0.08 |

d2 |

0.0168 |

|

Risk free rates (annual) r |

2.00% |

N(d1) |

0.5240 |

|

Current stock price (S) |

$50.00 |

N(d2) |

0.5067 |

|

Strike price (K) |

$50.00 |

B/S call Price |

0.9052 |

|

Dividend yield (annual) |

0 |

B/S Put Price |

0.8220 |

Call Price = $0.9052

Put Price = $0.8220

b. Strike price is increased from $50 to $55

|

INPUTS |

Outputs |

Value |

|

|

Standard deviation (Annual) σ |

15.00% |

d1 |

-2.1410 |

|

Expiration (in Years) T |

0.08 |

d2 |

-2.1843 |

|

Risk free rates (annual) r |

2.00% |

N(d1) |

0.0161 |

|

Current stock price (S) |

$50.00 |

N(d2) |

0.0145 |

|

Strike price (K) |

$55.00 |

B/S call Price |

0.0123 |

|

Dividend yield (annual) |

0 |

B/S Put Price |

4.9207 |

Call Price = $0.0123

Put Price = $4.9207

c. Doubling the time of maturity form one month (1/12 =0.08 years) to two months (=2/12 =0.17 years). Strike price is assumed at original level ($50)

|

INPUTS |

Outputs |

Value |

|

|

Standard deviation (Annual) σ |

15.00% |

d1 |

0.0851 |

|

Expiration (in Years) T |

0.17 |

d2 |

0.0238 |

|

Risk free rates (annual) r |

2.00% |

N(d1) |

0.5339 |

|

Current stock price (S) |

$50.00 |

N(d2) |

0.5095 |

|

Strike price (K) |

$50.00 |

B/S call Price |

1.3043 |

|

Dividend yield (annual) |

0 |

B/S Put Price |

1.1379 |

Call Price = $1.3043

Put Price = $1.1379

Formulas used in excel calculation:

Add Answer to:

Use an options calculator for the first 2 problems 1a prices of a one month put...

1a. For a stock trading at $50 with 15% volatility and 2% risk free interest rate,...

1a. For a stock trading at $50 with 15% volatility and 2% risk free interest rate, find the prices of a one month put and call options with a strike price of $50. Determine the effect on both the put and call of increasing the strike price to $55 Determine the effect of doubling the time to maturity

1a. For a stock trading at $50 with 15% volatility and 2% risk free interest rate, find the prices of a one month put and call options with a strike price of $50. Determine the effect on both the put and call of increasing the strike price to $55 Determine the effect of doubling the time to maturity

1a. For a stock trading at $50 with 15% volatility and 2% risk free interest rate,...

1a. For a stock trading at $50 with 15% volatility and 2% risk free interest rate, find the prices of a one month put and call options with a strike price of $50. b. Determine the effect on both the put and call of increasing the strike price to $55 c. Determine the effect of doubling the time to maturity

show work, step by step and explain please. no excel. 1a. For a stock trading at...

show work, step by step and explain please. no excel.

1a. For a stock trading at $50 with 15% volatility and 2% risk free interest rate, find the prices of a one month put and call options with a strike price of $50. b. Determine the effect on both the put and call of increasing the strike price to $55 Determine the effect of doubling the time to maturity

show work, step by step and explain please. no excel.

1a. For a stock trading at $50 with 15% volatility and 2% risk free interest rate, find the prices of a one month put and call options with a strike price of $50. b. Determine the effect on both the put and call of increasing the strike price to $55 Determine the effect of doubling the time to maturity

The table below gives today’s prices of six-month European put and call options written on a...

The table below gives today’s prices of six-month European put and call options written on a share of ABC stock at different strike prices. The stock does not pay a dividend and the risk-free interest rate is 0% per annum. Call Price ($) Strike Price ($) Put Price ($) 13.1 105 8.2 9.7 110 9.7 7.9 115 12.9 Using call options with strike prices of 105 and 110, create a bear spread and show in a table the profit of the...

8. The five factors affecting prices of call and put options Both call and put options...

8. The five factors affecting prices of call and put options Both call and put options are affected by the following five factors: the exercise price, the underlying stock price, the time to expiration, the stock’s standard deviation, and the risk-free rate. However, the direction of the effects on call and put options could be different. Use the following table to identify whether each statement describes put options or call options: Statement Put Option Call Option 1. An increase in...

(a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC

2. (a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC.(b) Consider an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 20% per annum, and the time to maturity is 5 months. What is the price of the option if it is a European call?

The following prices are available for call and put options on a stock priced at $50....

The following prices are available for call and put options on a stock priced at $50. The risk-free rate is 6 percent and the volatility is 0.35. The March options have 90 days remaining and the June options have 180 days remaining. The Black-Scholes model was used to obtain the prices. Calls Puts Strike March June March June 45 6.84 8.41 1.18 2.09 50 3.82 5.58 3.08 4.13 55 1.89 3.54 6.08 6.93 Use this information to answer questions 1...

5.8. The prices of European call and put options on a non-dividend-paying stock with 15 months to...

5.8. The prices of European call and put options on a non-dividend-paying stock with 15 months to maturity, a strike price of $118, and an expiration date in 15 months are $21 and $5, respectively. The current stock price is $125. What is the implied risk-free rate?

An options exchange has a number of European call and put options listed for trading on...

An options exchange has a number of European call and put options listed for trading on ENCORE stock. You have been paying close attention to two call options on ENCORE, one with an exercise price of $52 and the other with an exercise price of $50. The former is currently trading at $4.25 and the latter at $6.50. Both options have a remaining life of six months. The current price of ENCORE stock is $51 and the six-month risk free...

The prices of European call and put options on a dividend-paying stock with 6 months to...

The prices of European call and put options on a dividend-paying stock with 6 months to maturity and a strike price of $125 are $20 and $5, respectively. If the current stock price is $140, what is the implied annual continuously compounded risk-free rate? Assume the present value of dividend to be paid out over the next 6 months is $3.

1a. For a stock trading at $50 with 15% volatility and 2% risk free interest rate, find the prices of a one month put and call options with a strike price of $50. Determine the effect on both the put and call of increasing the strike price to $55 Determine the effect of doubling the time to maturity

1a. For a stock trading at $50 with 15% volatility and 2% risk free interest rate, find the prices of a one month put and call options with a strike price of $50. Determine the effect on both the put and call of increasing the strike price to $55 Determine the effect of doubling the time to maturity

show work, step by step and explain please. no excel.

1a. For a stock trading at $50 with 15% volatility and 2% risk free interest rate, find the prices of a one month put and call options with a strike price of $50. b. Determine the effect on both the put and call of increasing the strike price to $55 Determine the effect of doubling the time to maturity

show work, step by step and explain please. no excel.

1a. For a stock trading at $50 with 15% volatility and 2% risk free interest rate, find the prices of a one month put and call options with a strike price of $50. b. Determine the effect on both the put and call of increasing the strike price to $55 Determine the effect of doubling the time to maturity

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago