•Suppose that you forecast the GBP/USD exchange rate at the end of next year to be...

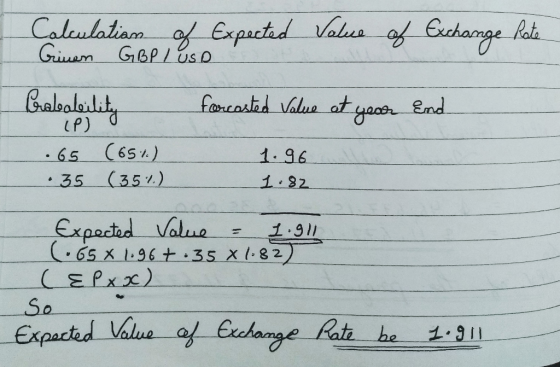

•Suppose that you forecast the GBP/USD exchange rate at the end of next year to be either:

•1.96 with a probability of 65%, or

1.82 with a probability of 35%

•What is the expected value of the exchange rate at the end of next year?

Homework Answers

Add Answer to:

•Suppose that you forecast the GBP/USD exchange rate at the end

of next year to be...

Suppose that the USD/ZAR spot rate is quoted as 13.50ZAR and the GBP/USD is $1.30. The...

Suppose that the USD/ZAR spot rate is quoted as 13.50ZAR and the GBP/USD is $1.30. The cross exchange rate between GBP/ZAR is?

22 The spot ask USD/GBP exchange rate is $1.89 - £100. The spot bid USD/GBP exchange rate is $1.88 - £100. What is the...

22 The spot ask USD/GBP exchange rate is $1.89 - £100. The spot bid USD/GBP exchange rate is $1.88 - £100. What is the profit (loss) if an investor buys $10,000,000 worth of British pounds and simultaneously sell the pounds proceeds of that purchase? points Multiple Choice 302.50:11 0 ($52,910) 0 None of the options 0 (552,632) 0 $52,910 0 $52,632 The dollar-euro exchange rate is $1.40 - €1.00 and the dollar-yen exchange rate is 110 - $1.00. What is...

22 The spot ask USD/GBP exchange rate is $1.89 - £100. The spot bid USD/GBP exchange rate is $1.88 - £100. What is the profit (loss) if an investor buys $10,000,000 worth of British pounds and simultaneously sell the pounds proceeds of that purchase? points Multiple Choice 302.50:11 0 ($52,910) 0 None of the options 0 (552,632) 0 $52,910 0 $52,632 The dollar-euro exchange rate is $1.40 - €1.00 and the dollar-yen exchange rate is 110 - $1.00. What is...

Currently the spot exchange rate is $1.558 per pound (USD/GBP). The interest rate in the UK...

Currently the spot exchange rate is $1.558 per pound (USD/GBP). The interest rate in the UK is 6%. The one-year forward exchange rate is $1.5200/GBP. If interest rate parity holds, what must be the US interest rate for the same period?

Suppose the Swiss Franc exchange rate is CHF 2.00 = USD 1.00 and the British Pound...

Suppose the Swiss Franc exchange rate is CHF 2.00 = USD 1.00 and the British Pound exchange rate is GBP 0.60 = USD 1.00. Suppose a dealer quotes a rate of 3 CHF = 1 GBP. What is the CHF/GBP cross rate? Is there an arbitrage opportunity here? If, yes then calculate the arbitrage profit on $5,000?

2) The spot USD /GBP rate is 1.1505. The1 year t-bill rate in the US is...

2) The spot USD /GBP rate is 1.1505. The1 year t-bill rate in the US is .9335%. The 1 year rate in the UK is 0.7969%. a) Calculate the 1 year USD/GBP 1 year forward rate. b) If the observed 1 year forward rate is 1.35 USD/GBP, is there an arbitrage opportunity? How would you take advantage of this? Show all your transactions and steps.

2) The spot USD /GBP rate is 1.1505. The1 year t-bill rate in the US is .9335%. The 1 year rate in the UK is 0.7969%. a) Calculate the 1 year USD/GBP 1 year forward rate. b) If the observed 1 year forward rate is 1.35 USD/GBP, is there an arbitrage opportunity? How would you take advantage of this? Show all your transactions and steps.

Suppose that the exchange rate (spot price) of Euro in GBP (British Pound) is GBP 0.95. &nbs...

Suppose that the exchange rate (spot price) of Euro in GBP (British Pound) is GBP 0.95. In addition, assume that you can freely borrow and lend in GBP for any maturity at a rate of 2% per annum and that you can do the same in Euro at a rate of 1% per annum. Both rates are continuously compounded rates. Given these assumptions: Compute the forward price (exchange rate) of the GBP in Euro for delivery of the GBP in...

Country USD Nominal Rate 2.5% GBP 3.5% The above table contains nominal interest rate information for the United States...

Country USD Nominal Rate 2.5% GBP 3.5% The above table contains nominal interest rate information for the United States and Great Britain. Assume the current U.S. dollar-British spot rate is GBP0.6134/USD. what is the approximate forward exchange rate for delivery 360 days from now? [Assume the USD is the home currency (currency of interest)] 0 GBP 0.6195/USD GBP 0.6073/USD USD 0.6195/GBP 0 USD0.6073/GBP

Country USD Nominal Rate 2.5% GBP 3.5% The above table contains nominal interest rate information for the United States and Great Britain. Assume the current U.S. dollar-British spot rate is GBP0.6134/USD. what is the approximate forward exchange rate for delivery 360 days from now? [Assume the USD is the home currency (currency of interest)] 0 GBP 0.6195/USD GBP 0.6073/USD USD 0.6195/GBP 0 USD0.6073/GBP

Suppose your broker give you the following information: Spot exchange rate (USD/EUR) = 1.1370 One year...

Suppose your broker give you the following information: Spot exchange rate (USD/EUR) = 1.1370 One year forward rate (USD/EUR) = 1.1405 One year USD interest rate = 0.87% One year Euro interest rate = 0.65% a. Is there any violation of interest rate parity? b. How would you take advantage of any arbitrage situation? c. What is your profit? d. Suggest an equilibrium value for the forward rate

5. Suppose that the current value of the S&P 500 stock index is USD 2600. Assume that the per ann...

5. Suppose that the current value of the S&P 500 stock index is USD 2600. Assume that the per annum rates of interest in USD and GBP(British Pound) are respectively 3% and 2% on a continuously compounded basis, and that the S&P 500 index pays a continuous dividend rate of 2% per annum. Finally, the spot exchange rate is USD1.3 per GBP. a) Compute the forward price of the S&P 500 in USD for delivery in one year. for delivery...

5. Suppose that the current value of the S&P 500 stock index is USD 2600. Assume that the per annum rates of interest in USD and GBP(British Pound) are respectively 3% and 2% on a continuously compounded basis, and that the S&P 500 index pays a continuous dividend rate of 2% per annum. Finally, the spot exchange rate is USD1.3 per GBP. a) Compute the forward price of the S&P 500 in USD for delivery in one year. for delivery...

19 Suppose that the GBP is pegged to gold at £20 per ounce. The USD is...

19 Suppose that the GBP is pegged to gold at £20 per ounce. The USD is pegged to gold at $35 per ounce. This implies an exchange rate of $175/18. How might an Investor take advantage of situation if the current market exchange rate is $1.60/1£? Multiple Choice points 02-50-30 0 Buy gold at $35 per ounce. Convert the gold to $200 at $20 per ounce. Exchange the €200 for dollars at the current rate of $160 per pound 0...

19 Suppose that the GBP is pegged to gold at £20 per ounce. The USD is pegged to gold at $35 per ounce. This implies an exchange rate of $175/18. How might an Investor take advantage of situation if the current market exchange rate is $1.60/1£? Multiple Choice points 02-50-30 0 Buy gold at $35 per ounce. Convert the gold to $200 at $20 per ounce. Exchange the €200 for dollars at the current rate of $160 per pound 0...

22 The spot ask USD/GBP exchange rate is $1.89 - £100. The spot bid USD/GBP exchange rate is $1.88 - £100. What is the profit (loss) if an investor buys $10,000,000 worth of British pounds and simultaneously sell the pounds proceeds of that purchase? points Multiple Choice 302.50:11 0 ($52,910) 0 None of the options 0 (552,632) 0 $52,910 0 $52,632 The dollar-euro exchange rate is $1.40 - €1.00 and the dollar-yen exchange rate is 110 - $1.00. What is...

22 The spot ask USD/GBP exchange rate is $1.89 - £100. The spot bid USD/GBP exchange rate is $1.88 - £100. What is the profit (loss) if an investor buys $10,000,000 worth of British pounds and simultaneously sell the pounds proceeds of that purchase? points Multiple Choice 302.50:11 0 ($52,910) 0 None of the options 0 (552,632) 0 $52,910 0 $52,632 The dollar-euro exchange rate is $1.40 - €1.00 and the dollar-yen exchange rate is 110 - $1.00. What is...

2) The spot USD /GBP rate is 1.1505. The1 year t-bill rate in the US is .9335%. The 1 year rate in the UK is 0.7969%. a) Calculate the 1 year USD/GBP 1 year forward rate. b) If the observed 1 year forward rate is 1.35 USD/GBP, is there an arbitrage opportunity? How would you take advantage of this? Show all your transactions and steps.

2) The spot USD /GBP rate is 1.1505. The1 year t-bill rate in the US is .9335%. The 1 year rate in the UK is 0.7969%. a) Calculate the 1 year USD/GBP 1 year forward rate. b) If the observed 1 year forward rate is 1.35 USD/GBP, is there an arbitrage opportunity? How would you take advantage of this? Show all your transactions and steps.

Country USD Nominal Rate 2.5% GBP 3.5% The above table contains nominal interest rate information for the United States and Great Britain. Assume the current U.S. dollar-British spot rate is GBP0.6134/USD. what is the approximate forward exchange rate for delivery 360 days from now? [Assume the USD is the home currency (currency of interest)] 0 GBP 0.6195/USD GBP 0.6073/USD USD 0.6195/GBP 0 USD0.6073/GBP

Country USD Nominal Rate 2.5% GBP 3.5% The above table contains nominal interest rate information for the United States and Great Britain. Assume the current U.S. dollar-British spot rate is GBP0.6134/USD. what is the approximate forward exchange rate for delivery 360 days from now? [Assume the USD is the home currency (currency of interest)] 0 GBP 0.6195/USD GBP 0.6073/USD USD 0.6195/GBP 0 USD0.6073/GBP

5. Suppose that the current value of the S&P 500 stock index is USD 2600. Assume that the per annum rates of interest in USD and GBP(British Pound) are respectively 3% and 2% on a continuously compounded basis, and that the S&P 500 index pays a continuous dividend rate of 2% per annum. Finally, the spot exchange rate is USD1.3 per GBP. a) Compute the forward price of the S&P 500 in USD for delivery in one year. for delivery...

5. Suppose that the current value of the S&P 500 stock index is USD 2600. Assume that the per annum rates of interest in USD and GBP(British Pound) are respectively 3% and 2% on a continuously compounded basis, and that the S&P 500 index pays a continuous dividend rate of 2% per annum. Finally, the spot exchange rate is USD1.3 per GBP. a) Compute the forward price of the S&P 500 in USD for delivery in one year. for delivery...

19 Suppose that the GBP is pegged to gold at £20 per ounce. The USD is pegged to gold at $35 per ounce. This implies an exchange rate of $175/18. How might an Investor take advantage of situation if the current market exchange rate is $1.60/1£? Multiple Choice points 02-50-30 0 Buy gold at $35 per ounce. Convert the gold to $200 at $20 per ounce. Exchange the €200 for dollars at the current rate of $160 per pound 0...

19 Suppose that the GBP is pegged to gold at £20 per ounce. The USD is pegged to gold at $35 per ounce. This implies an exchange rate of $175/18. How might an Investor take advantage of situation if the current market exchange rate is $1.60/1£? Multiple Choice points 02-50-30 0 Buy gold at $35 per ounce. Convert the gold to $200 at $20 per ounce. Exchange the €200 for dollars at the current rate of $160 per pound 0...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago