Homework Answers

Add Answer to:

Question 3 (total of 20 marks): An investor holds a portfolio comprising three assets (or stocks)...

Question 3 (total of 20 marks): Refer to the below table to answer the questions that follow. Assume that returns are e...

Question 3 (total of 20 marks): Refer to the below table to answer the questions that follow. Assume that returns are effective annual rates Year Return on Stock A Return on Market 2007 35% 15% 2008 -35% -25% 2009 15% 40% Question 3a (1 marks): What is stock A's expected return? Question 3b (1 marks): What is the market's expected return? Question 3c (4 marks): What is the sample standard deviation of stock A's returns? buestion 3d (4 marks): What...

Question 3 (total of 20 marks): Refer to the below table to answer the questions that follow. Assume that returns are effective annual rates Year Return on Stock A Return on Market 2007 35% 15% 2008 -35% -25% 2009 15% 40% Question 3a (1 marks): What is stock A's expected return? Question 3b (1 marks): What is the market's expected return? Question 3c (4 marks): What is the sample standard deviation of stock A's returns? buestion 3d (4 marks): What...

statistics 4. An investor holds a portfolio consisting of two stocks. She puts 25% of her...

statistics

4. An investor holds a portfolio consisting of two stocks. She puts 25% of her money in Stock A and 75% into Stock B. Stock A has an expected return of Ri=8% and a standard deviation of 0,=12%. Stock B has an expected return of Rg=15% with a standard deviation of o,=22%. The portfolio return is P=0.25RA +0.75R, (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of the returns on the portfolio assuming that...

statistics

4. An investor holds a portfolio consisting of two stocks. She puts 25% of her money in Stock A and 75% into Stock B. Stock A has an expected return of Ri=8% and a standard deviation of 0,=12%. Stock B has an expected return of Rg=15% with a standard deviation of o,=22%. The portfolio return is P=0.25RA +0.75R, (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of the returns on the portfolio assuming that...

Three-stock Portfolio The information regarding a portfolio consisting of three stocks is given below. Stock A...

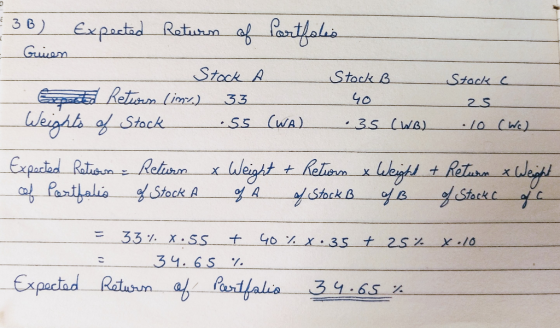

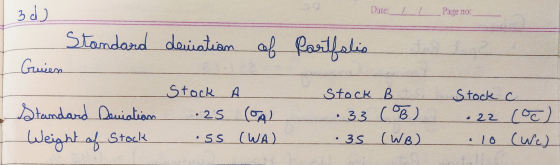

Three-stock Portfolio The information regarding a portfolio consisting of three stocks is given below. Stock A Stock B Stock C E(R) 15% 21% Standard Deviation 10% 30% Weight 0.30 0.30 17% 14% 0.40 The correlation coefficient between Stocks A and B is 0.27. The correlation coefficient between Stocks A and C is 0.67. The correlation coefficient between Stocks B and C is 0.12. What is the expected return of the portfolio? Select one: o a. 12.54% b. 10.68% c. 17.60%...

Three-stock Portfolio The information regarding a portfolio consisting of three stocks is given below. Stock A Stock B Stock C E(R) 15% 21% Standard Deviation 10% 30% Weight 0.30 0.30 17% 14% 0.40 The correlation coefficient between Stocks A and B is 0.27. The correlation coefficient between Stocks A and C is 0.67. The correlation coefficient between Stocks B and C is 0.12. What is the expected return of the portfolio? Select one: o a. 12.54% b. 10.68% c. 17.60%...

Part II Question 1: You invest in a portfolio of 5 stocks with an equal investment...

Part II Question 1: You invest in a portfolio of 5 stocks with an equal investment in each one. The betas of the 5 stocks are as follows: .8, -1.3, .95, 1.2 and 1.4. The risk-free return is 3% and the market return is 7%. Compute the beta of the portfolio. Compute the required return of the portfolio. Question 2: You are given the following probability distribution for a stock: Probability Outcome .5 -6% .5 18% A) Compute the...

P.14 An investor holding a portfolio consisting of two stocks invests 25% of assets in Stock...

P.14 An investor holding a portfolio consisting of two stocks invests 25% of assets in Stock A and 75% into Stock B. The return RA from Stock A has a mean of 4% and a standard deviation of A = 8%. Stock B has an expected return E(RB) = 8% with a standard deviation of ob = 12%. The portfolio return is P = 0.25RA +0.75RB. (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of...

P.14 An investor holding a portfolio consisting of two stocks invests 25% of assets in Stock A and 75% into Stock B. The return RA from Stock A has a mean of 4% and a standard deviation of A = 8%. Stock B has an expected return E(RB) = 8% with a standard deviation of ob = 12%. The portfolio return is P = 0.25RA +0.75RB. (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of...

An investor can design a risky portfolio based on two stocks, A and B. Stock A...

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 45% and a standard deviation of return of 9%. Stock B has an expected return of 15% and a standard deviation of return of 2%.The correlation coefficient between the returns of A and B is 0.0025. The risk-free rate of return is 2%. The standard deviation of return on the minimum variance portfolio is _________.

s presented with the two following stocks 17. The investor Stock A Stock B Expected Return...

s presented with the two following stocks 17. The investor Stock A Stock B Expected Return Standard Deviation 30% 40% 60% 50% the portfolio that the expected return Assume that the correlation coefficient between the stocks is zero. What stock A invests 30% i A.20% B.37% 07a 18. The investor is presented with the two following stocks: Stock A Stock B Expected Return Standard Deviation 0% 40% 50% 60% Assume that the correlation coefficient between the stocks is zero. What...

s presented with the two following stocks 17. The investor Stock A Stock B Expected Return Standard Deviation 30% 40% 60% 50% the portfolio that the expected return Assume that the correlation coefficient between the stocks is zero. What stock A invests 30% i A.20% B.37% 07a 18. The investor is presented with the two following stocks: Stock A Stock B Expected Return Standard Deviation 0% 40% 50% 60% Assume that the correlation coefficient between the stocks is zero. What...

An investor can design a risky portfolio based on two stocks, A and B. Stock A...

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 14% and a standard deviation of return of 24.0%. Stock B has an expected return of 10% and a standard deviation of return of 4%. The correlation coefficient between the returns of A and B is 0.50. The risk-free rate of return is 8%. The proportion of the optimal risky portfolio that should be invested in stock A is...

Question 12 1 pts A portfolio is composed of two stocks, A and B Stock A...

Question 12 1 pts A portfolio is composed of two stocks, A and B Stock A has a standard deviation of return of 24%, while stock Bhas a standard deviation of return of 18%. Stock A comprises 60% of the portfolio, while stock B comprises 40% of the portfolio. If the variance of return on the portfolio is.0350, the correlation coefficient between the returns on A and Bis 583 438 327 .225 • Previous Next Quiz saved at 10:34am Submit...

Question 12 1 pts A portfolio is composed of two stocks, A and B Stock A has a standard deviation of return of 24%, while stock Bhas a standard deviation of return of 18%. Stock A comprises 60% of the portfolio, while stock B comprises 40% of the portfolio. If the variance of return on the portfolio is.0350, the correlation coefficient between the returns on A and Bis 583 438 327 .225 • Previous Next Quiz saved at 10:34am Submit...

Show work in excel please An investor can design a risky portfolio based on two stocks,...

Show work in excel please An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 19% and a standard deviation of return of 15.0%. Stock B has an expected return of 15% and a standard deviation of return of 6%. The correlation coefficient between the returns of A and B is 0.80. The risk-free rate of return is 11%. The proportion of the optimal risky portfolio that should be...

Question 3 (total of 20 marks): Refer to the below table to answer the questions that follow. Assume that returns are effective annual rates Year Return on Stock A Return on Market 2007 35% 15% 2008 -35% -25% 2009 15% 40% Question 3a (1 marks): What is stock A's expected return? Question 3b (1 marks): What is the market's expected return? Question 3c (4 marks): What is the sample standard deviation of stock A's returns? buestion 3d (4 marks): What...

Question 3 (total of 20 marks): Refer to the below table to answer the questions that follow. Assume that returns are effective annual rates Year Return on Stock A Return on Market 2007 35% 15% 2008 -35% -25% 2009 15% 40% Question 3a (1 marks): What is stock A's expected return? Question 3b (1 marks): What is the market's expected return? Question 3c (4 marks): What is the sample standard deviation of stock A's returns? buestion 3d (4 marks): What...

statistics

4. An investor holds a portfolio consisting of two stocks. She puts 25% of her money in Stock A and 75% into Stock B. Stock A has an expected return of Ri=8% and a standard deviation of 0,=12%. Stock B has an expected return of Rg=15% with a standard deviation of o,=22%. The portfolio return is P=0.25RA +0.75R, (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of the returns on the portfolio assuming that...

statistics

4. An investor holds a portfolio consisting of two stocks. She puts 25% of her money in Stock A and 75% into Stock B. Stock A has an expected return of Ri=8% and a standard deviation of 0,=12%. Stock B has an expected return of Rg=15% with a standard deviation of o,=22%. The portfolio return is P=0.25RA +0.75R, (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of the returns on the portfolio assuming that...

Three-stock Portfolio The information regarding a portfolio consisting of three stocks is given below. Stock A Stock B Stock C E(R) 15% 21% Standard Deviation 10% 30% Weight 0.30 0.30 17% 14% 0.40 The correlation coefficient between Stocks A and B is 0.27. The correlation coefficient between Stocks A and C is 0.67. The correlation coefficient between Stocks B and C is 0.12. What is the expected return of the portfolio? Select one: o a. 12.54% b. 10.68% c. 17.60%...

Three-stock Portfolio The information regarding a portfolio consisting of three stocks is given below. Stock A Stock B Stock C E(R) 15% 21% Standard Deviation 10% 30% Weight 0.30 0.30 17% 14% 0.40 The correlation coefficient between Stocks A and B is 0.27. The correlation coefficient between Stocks A and C is 0.67. The correlation coefficient between Stocks B and C is 0.12. What is the expected return of the portfolio? Select one: o a. 12.54% b. 10.68% c. 17.60%...

P.14 An investor holding a portfolio consisting of two stocks invests 25% of assets in Stock A and 75% into Stock B. The return RA from Stock A has a mean of 4% and a standard deviation of A = 8%. Stock B has an expected return E(RB) = 8% with a standard deviation of ob = 12%. The portfolio return is P = 0.25RA +0.75RB. (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of...

P.14 An investor holding a portfolio consisting of two stocks invests 25% of assets in Stock A and 75% into Stock B. The return RA from Stock A has a mean of 4% and a standard deviation of A = 8%. Stock B has an expected return E(RB) = 8% with a standard deviation of ob = 12%. The portfolio return is P = 0.25RA +0.75RB. (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of...

s presented with the two following stocks 17. The investor Stock A Stock B Expected Return Standard Deviation 30% 40% 60% 50% the portfolio that the expected return Assume that the correlation coefficient between the stocks is zero. What stock A invests 30% i A.20% B.37% 07a 18. The investor is presented with the two following stocks: Stock A Stock B Expected Return Standard Deviation 0% 40% 50% 60% Assume that the correlation coefficient between the stocks is zero. What...

s presented with the two following stocks 17. The investor Stock A Stock B Expected Return Standard Deviation 30% 40% 60% 50% the portfolio that the expected return Assume that the correlation coefficient between the stocks is zero. What stock A invests 30% i A.20% B.37% 07a 18. The investor is presented with the two following stocks: Stock A Stock B Expected Return Standard Deviation 0% 40% 50% 60% Assume that the correlation coefficient between the stocks is zero. What...

Question 12 1 pts A portfolio is composed of two stocks, A and B Stock A has a standard deviation of return of 24%, while stock Bhas a standard deviation of return of 18%. Stock A comprises 60% of the portfolio, while stock B comprises 40% of the portfolio. If the variance of return on the portfolio is.0350, the correlation coefficient between the returns on A and Bis 583 438 327 .225 • Previous Next Quiz saved at 10:34am Submit...

Question 12 1 pts A portfolio is composed of two stocks, A and B Stock A has a standard deviation of return of 24%, while stock Bhas a standard deviation of return of 18%. Stock A comprises 60% of the portfolio, while stock B comprises 40% of the portfolio. If the variance of return on the portfolio is.0350, the correlation coefficient between the returns on A and Bis 583 438 327 .225 • Previous Next Quiz saved at 10:34am Submit...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago