The table below shows market prices for four zero coupon bonds with four different terms: one,...

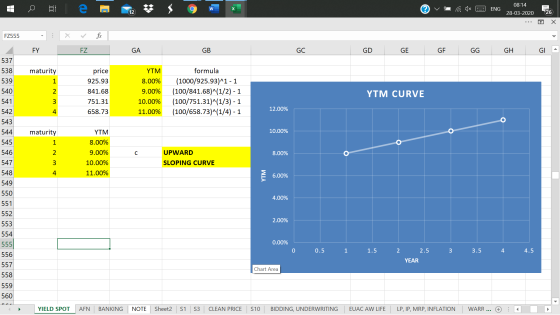

The table below shows market prices for four zero coupon bonds with four different terms: one, two, three and four years. The bonds all have a face value of $1 comma 000. Calculate the yields on the zero coupon bonds and graph the yield curve. What is the shape of the yield curve? Zero Coupon Bond Prices Term (years) Price ($) 1 925.93 2 841.68 3 751.31 4 658.73

Homework Answers

SEE THE IMAGE. ANY DOUBTS, FEEL FREE TO ASK. THUMBS UP PLEASE

Add Answer to:

The table below shows market prices for four zero coupon bonds

with four different terms: one,...

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM...

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of...

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

Assume the zero-coupon yields on default-free securities are as summarized in the following table: Maturity 1...

Assume the zero-coupon yields on default-free securities are as summarized in the following table: Maturity 1 year 2 years 3 years 4 years 5 years Zero-Coupon Yields 4.104.10% 4.604.60% 4.904.90% 5.305.30% 5.505.50% What is the price of a three-year, default-free security with a face value of $ 1 comma 000$1,000 and an annual coupon rate of 5 %5%? What is the yield to maturity for this bond? What is the price of a three-year, default-free security with a face value...

Prices in the table are for zero interest rate government bonds with a $1000 face value...

Prices in the table are for zero interest rate government bonds with a $1000 face value Maturity (years) Zero Price 1 $ 970.87 - 2 $ 920.13 3 $ 863.84 4 $ 807.22 • A 5 year government bond with a $1000 face value that pays a 4.0% coupon (with annual payments) is priced at $925 today. 13.(CH15) First, find the implied spot rates for years 1-5 (i.e. bootstrap the yield curve). Based on the spot rates, the shape of...

Prices in the table are for zero interest rate government bonds with a $1000 face value Maturity (years) Zero Price 1 $ 970.87 - 2 $ 920.13 3 $ 863.84 4 $ 807.22 • A 5 year government bond with a $1000 face value that pays a 4.0% coupon (with annual payments) is priced at $925 today. 13.(CH15) First, find the implied spot rates for years 1-5 (i.e. bootstrap the yield curve). Based on the spot rates, the shape of...

The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value...

The following table summarizes prices of

various default-free zero-coupon bonds (expressed as a percentage

of face value):

Maturity (years) Price (per $100 face value) | 1 | 2 | 3 | 4 | 5 94.52 89.68 85.40 81.65 78.35 The yield to maturity for the four-year zero-coupon bond is closest to _ a 0.18% Ob. 10.40% Oc. 2.60% Od. 22.47% Oe.5.20%

The following table summarizes prices of

various default-free zero-coupon bonds (expressed as a percentage

of face value):

Maturity (years) Price (per $100 face value) | 1 | 2 | 3 | 4 | 5 94.52 89.68 85.40 81.65 78.35 The yield to maturity for the four-year zero-coupon bond is closest to _ a 0.18% Ob. 10.40% Oc. 2.60% Od. 22.47% Oe.5.20%

Bond prices in the absence of arbitrage Consider a market with two risk-free zero-coupon bonds, A...

Bond prices in the absence of arbitrage Consider a market with two risk-free zero-coupon bonds, A and B. Their respective maturities are 1 and 2 years, and their market prices are 97.0874 and 95.1814 (expressed as percentage of the face value). (a) Calculate the discount rates rt for t = 1 and 2 years. (b) Suppose that a two-year bond C, with a coupon rate of 2.75%, also trades in the market. What should be its price if there is...

4. The following table summarizes prices of various zero-coupon bonds (expressed as a percentage of face...

4. The following table summarizes prices of various zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 123 Price (per $100 face value) $95.51 $91.05 | $86.38 $81.65 | $76.51 Compute the yield to maturity for each bond.

4. The following table summarizes prices of various zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 123 Price (per $100 face value) $95.51 $91.05 | $86.38 $81.65 | $76.51 Compute the yield to maturity for each bond.

Below are given the prices and maturities of zero-coupon bonds of the country X. Each bond...

Below are given the prices and maturities of zero-coupon bonds of the country X. Each bond has a face value of 1000. Maturity (years) Current price 1 952.38 2 942.60 3 928.60 What is the yield on the bond that matures in three years? Please write an answer in decimals. For example, 12.3% would be 0.123. Also, round your answer to the third decimal.

14, A one-year zero coupon bond yields 3.0%. The two-and three-year zero-coupon bonds yield 4.0% and 5.0% respectively. a. The forward rate for a one-year loan beginning in two years is closest t...

14, A one-year zero coupon bond yields 3.0%. The two-and three-year zero-coupon bonds yield 4.0% and 5.0% respectively. a. The forward rate for a one-year loan beginning in two years is closest to? (10 points) b. The four-year spot rate is not given above; however, the forward price for a one-year zero-coupon bond beginning in three years is known to be 0.8400. The price today of a four-year zero-coupon bond is closest to? (5 points)

14, A one-year zero coupon...

14, A one-year zero coupon bond yields 3.0%. The two-and three-year zero-coupon bonds yield 4.0% and 5.0% respectively. a. The forward rate for a one-year loan beginning in two years is closest to? (10 points) b. The four-year spot rate is not given above; however, the forward price for a one-year zero-coupon bond beginning in three years is known to be 0.8400. The price today of a four-year zero-coupon bond is closest to? (5 points)

14, A one-year zero coupon...

Below is a list of prices for zero-coupon bonds of various maturities. Price of $1,000 Par...

Below is a list of prices for zero-coupon bonds of various maturities. Price of $1,000 Par Maturity (Years) Bond (Zero-Coupon) $966.78 894.28 803.54 WN a. A 6.4% coupon $1,000 par bond pays an annual coupon and will mature in 3 years. What should the yield to maturity on the bond be? (Round your answer to 2 decimal places.) Yield to maturity % b. If at the end of the first year the yield curve flattens out at 8.1%, what will...

Below is a list of prices for zero-coupon bonds of various maturities. Price of $1,000 Par Maturity (Years) Bond (Zero-Coupon) $966.78 894.28 803.54 WN a. A 6.4% coupon $1,000 par bond pays an annual coupon and will mature in 3 years. What should the yield to maturity on the bond be? (Round your answer to 2 decimal places.) Yield to maturity % b. If at the end of the first year the yield curve flattens out at 8.1%, what will...

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

Prices in the table are for zero interest rate government bonds with a $1000 face value Maturity (years) Zero Price 1 $ 970.87 - 2 $ 920.13 3 $ 863.84 4 $ 807.22 • A 5 year government bond with a $1000 face value that pays a 4.0% coupon (with annual payments) is priced at $925 today. 13.(CH15) First, find the implied spot rates for years 1-5 (i.e. bootstrap the yield curve). Based on the spot rates, the shape of...

Prices in the table are for zero interest rate government bonds with a $1000 face value Maturity (years) Zero Price 1 $ 970.87 - 2 $ 920.13 3 $ 863.84 4 $ 807.22 • A 5 year government bond with a $1000 face value that pays a 4.0% coupon (with annual payments) is priced at $925 today. 13.(CH15) First, find the implied spot rates for years 1-5 (i.e. bootstrap the yield curve). Based on the spot rates, the shape of...

The following table summarizes prices of

various default-free zero-coupon bonds (expressed as a percentage

of face value):

Maturity (years) Price (per $100 face value) | 1 | 2 | 3 | 4 | 5 94.52 89.68 85.40 81.65 78.35 The yield to maturity for the four-year zero-coupon bond is closest to _ a 0.18% Ob. 10.40% Oc. 2.60% Od. 22.47% Oe.5.20%

The following table summarizes prices of

various default-free zero-coupon bonds (expressed as a percentage

of face value):

Maturity (years) Price (per $100 face value) | 1 | 2 | 3 | 4 | 5 94.52 89.68 85.40 81.65 78.35 The yield to maturity for the four-year zero-coupon bond is closest to _ a 0.18% Ob. 10.40% Oc. 2.60% Od. 22.47% Oe.5.20%

4. The following table summarizes prices of various zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 123 Price (per $100 face value) $95.51 $91.05 | $86.38 $81.65 | $76.51 Compute the yield to maturity for each bond.

4. The following table summarizes prices of various zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 123 Price (per $100 face value) $95.51 $91.05 | $86.38 $81.65 | $76.51 Compute the yield to maturity for each bond.

14, A one-year zero coupon bond yields 3.0%. The two-and three-year zero-coupon bonds yield 4.0% and 5.0% respectively. a. The forward rate for a one-year loan beginning in two years is closest to? (10 points) b. The four-year spot rate is not given above; however, the forward price for a one-year zero-coupon bond beginning in three years is known to be 0.8400. The price today of a four-year zero-coupon bond is closest to? (5 points)

14, A one-year zero coupon...

14, A one-year zero coupon bond yields 3.0%. The two-and three-year zero-coupon bonds yield 4.0% and 5.0% respectively. a. The forward rate for a one-year loan beginning in two years is closest to? (10 points) b. The four-year spot rate is not given above; however, the forward price for a one-year zero-coupon bond beginning in three years is known to be 0.8400. The price today of a four-year zero-coupon bond is closest to? (5 points)

14, A one-year zero coupon...

Below is a list of prices for zero-coupon bonds of various maturities. Price of $1,000 Par Maturity (Years) Bond (Zero-Coupon) $966.78 894.28 803.54 WN a. A 6.4% coupon $1,000 par bond pays an annual coupon and will mature in 3 years. What should the yield to maturity on the bond be? (Round your answer to 2 decimal places.) Yield to maturity % b. If at the end of the first year the yield curve flattens out at 8.1%, what will...

Below is a list of prices for zero-coupon bonds of various maturities. Price of $1,000 Par Maturity (Years) Bond (Zero-Coupon) $966.78 894.28 803.54 WN a. A 6.4% coupon $1,000 par bond pays an annual coupon and will mature in 3 years. What should the yield to maturity on the bond be? (Round your answer to 2 decimal places.) Yield to maturity % b. If at the end of the first year the yield curve flattens out at 8.1%, what will...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago