Homework Answers

Solution:

Buyers(holders) of the option pay premium to the writers of the option.

Sellers(writers) of the options receive premium from the holders of the option.

Holder(Buyer) of call option exercise a call option only when the spot exchange rate is higher than the strike price.

Holder(Buyer) of put option exercise a put option only when the spot exchange rate is lower than the strike price.

Net profit of buyer of call option = max(0, spot price - strike price) - premium paid

Net profit of seller of call option = min(o, strike price - spot price) + premium received

Net profit of buyer of put option = max(o, strike price - spot price) + premium paid

Net profit of seller of put option = min(0, spot price - strike price) + premium received

| Spot Exchange Rate($/€) | 1.05 | 1.1 | 1.15 | 1.2 | 1.25 | 1.3 | |

| Sell Call Option | Does holder exercise? | no | no | no | yes | yes | yes |

| Holder's net profit per unit | -0.03 | -0.03 | -0.03 | -0.08 | -0.13 | -0.18 | |

| Sellers's net profit per unit | 0.03 | 0.03 | 0.03 | -0.02 | -0.07 | -0.12 | |

| Sell Put Option | Does holder exercise? | no | no | no | no | no | no |

| Holder's net profit per unit | -0.02 | -0.02 | -0.02 | -0.02 | -0.02 | -0.02 | |

| Sellers's net profit per unit | 0.02 | 0.02 | 0.02 | 0.02 | 0.02 | 0.02 | |

| Net Profit | 0.05 | 0.05 | 0.05 | -4.51E-17 | -0.05 | -0.1 | |

Break-even point for the seller of call option is when the spot price is equal to the strike price + premium received.

Break-even point for the seller of put option is when the spot price is equal to the strike price - premium received.

So in this case break even point on

short call option is 1.15+0.03 = 1.18 dollar/euro.

short put option id 1.05-0.02=1.03 dollar/euro.

There are 2 Break even points for a short strangle.

Lower Strike Price - Sum of premium received = 1.05 - (0.03+0.02) = 1 dollar/euro

Higher Strike Price + Sum of premium received = 1.15 + (0.02+0.03) = 1.2 dollar/euro

Graphs

| Write a Call | Write a Put | ||||||||||

| Spot Price | Holder Exer | Gross Gain | Premium | Net Gain | Holder E/L | Gross Gain | Premium | Net Gain | NET PROFIT | ||

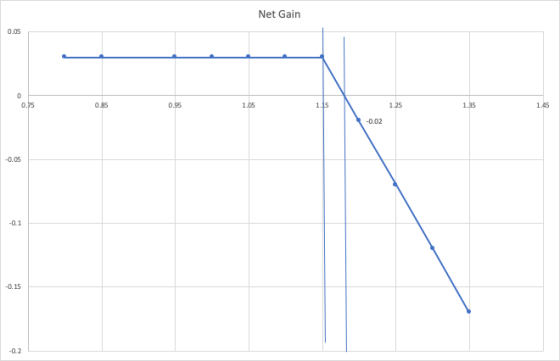

| 0.8 | no | 0 | 0.03 | 0.03 | yes | -0.25 | 0.02 | -0.23 | -0.20 | ||

| 0.85 | no | 0 | 0.03 | 0.03 | yes | -0.2 | 0.02 | -0.18 | -0.15 | ||

| 0.95 | no | 0 | 0.03 | 0.03 | yes | -0.1 | 0.02 | -0.08 | -0.05 | ||

| 1 | no | 0 | 0.03 | 0.03 | yes | -0.05 | 0.02 | -0.03 | 0.00 | ||

| 1.05 | no | 0 | 0.03 | 0.03 | no | 0 | 0.02 | 0.02 | 0.05 | ||

| 1.1 | no | 0 | 0.03 | 0.03 | no | 0 | 0.02 | 0.02 | 0.05 | ||

| 1.15 | no | 0 | 0.03 | 0.03 | no | 0 | 0.02 | 0.02 | 0.05 | ||

| 1.2 | yes | -0.05 | 0.03 | -0.02 | no | 0 | 0.02 | 0.02 | 0.00 | ||

| 1.25 | yes | -0.1 | 0.03 | -0.07 | no | 0 | 0.02 | 0.02 | -0.05 | ||

| 1.3 | yes | -0.15 | 0.03 | -0.12 | no | 0 | 0.02 | 0.02 | -0.10 | ||

| 1.35 | yes | -0.2 | 0.03 | -0.17 | no | 0 | 0.02 | 0.02 | -0.15 | ||

SHORT CALL OPTION

breakeven point in this is 1.18 dollar/euro.

SHORT PUT OPTION

breakeven point for this is 1.03 dollar/euro

SHORT SRANGLE

breakeven points are 1 dollar/euro and 1.2 dollar/euro.

Add Answer to:

• Short currency strangle . Call option premium - $0.03/€, Put option premium - $0.028€ Call...

• Long cury strangle Call option premium - 50.03., Put option premium - $0.02 € Call...

• Long cury strangle Call option premium - 50.03., Put option premium - $0.02 € Call option strike price 1.25/6, Put option strike price $1.15 € Option contract size - €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium 1 S105 S 15E $1.20 € $1.25 € $1.30/E Long call option Spot exchange rate Exercise (NY) Holder's net profit per unit Exercise (NY Holder's net profit per unit Net profit...

• Long cury strangle Call option premium - 50.03., Put option premium - $0.02 € Call option strike price 1.25/6, Put option strike price $1.15 € Option contract size - €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium 1 S105 S 15E $1.20 € $1.25 € $1.30/E Long call option Spot exchange rate Exercise (NY) Holder's net profit per unit Exercise (NY Holder's net profit per unit Net profit...

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price =...

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price = $1.10/€, Option contract size = €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium Spot exchange rate $1.00/€ $1.05/€ $1.10/€ $1.15/€ $1.20/€ $1.25/€ Long call option Exercise (N/Y) Holder’s net profit per unit Long put option Exercise (N/Y) Holder’s net profit per unit Net profit Net profit per unit (graph) Short currency straddle Call...

Mark buys Call and Put options with different strike prices. Please read the following information. Call...

Mark buys Call and Put options with different strike prices. Please read the following information. Call option premium: $0.02/€ Put option premium: $0.01/€ Call option strike price: $1.15/€ Put option strike price: $1.05/€ Option contract size: €50,000 Break-even points for Mark are _______. a. None of the above b. $1.02/€ and $1.18/€ c. $1.08/€ and $1.12/€ d. $1.06/€ and $1.16/€

Compute the upper and lower breakeven point for a strangle. The exercise price on call option...

Compute the upper and lower breakeven point for a strangle. The exercise price on call option is $1.72 and the exercise price on put option is $1.55. The premium on put option is $0.014 and premium on call option is $0.01. a. $1.526 and -$1.744 b. $1.744 and $1.526 c. $1.734 and $1.526 d. $1.744 and $1.574

Compute the upper and lower breakeven point for a strangle. The exercise price on call option is $1.72 and the exercise price on put option is $1.55. The premium on put option is $0.014 and premium on call option is $0.01. a. $1.526 and -$1.744 b. $1.744 and $1.526 c. $1.734 and $1.526 d. $1.744 and $1.574

A trader creates a long strangle with put options with a strike price of $160 per...

A trader creates a long strangle with put options with a strike price of $160 per share, and call options with a strike price of $170 per share by trading a total of 20 option contracts (10 put contracts and 10 call contracts). Each contract is written on 100 shares of stock. The put option is worth $18 per share, and the call option is worth $15 per share. What is the value (payoff) of the strangle at maturity as...

A trader creates a long strangle with put options with a strike price of $160 per...

A trader creates a long strangle with put options with a strike price of $160 per share, and call options with a strike price of $170 per share by trading a total of 20 option contracts (10 put contracts and 10 call contracts). Each contract is written on 100 shares of stock. The put option is worth $18 per share, and the call option is worth $15 per share. What is the value (payoff) of the strangle at maturity as...

Why with 'long strangle', the loss is decreased if price remains unchanged, compared with 'long straddle'? Why the loss sustained by investors would be the double premium ( long strang...

Why with 'long strangle', the loss is decreased if price remains

unchanged, compared with 'long straddle'?

Why the loss sustained by investors would be the double premium

( long strangle) which is same as the loss ( long straddle) equal

to double premium.

Market price of asset Premium- LOSS (c) Long call+ long put Profit Price expectations Market price of asset Net (double premium Loss c) Long put + long call Profit Price expectations ㅡ ㅡ ㅡㅡ Market p of...

Why with 'long strangle', the loss is decreased if price remains

unchanged, compared with 'long straddle'?

Why the loss sustained by investors would be the double premium

( long strangle) which is same as the loss ( long straddle) equal

to double premium.

Market price of asset Premium- LOSS (c) Long call+ long put Profit Price expectations Market price of asset Net (double premium Loss c) Long put + long call Profit Price expectations ㅡ ㅡ ㅡㅡ Market p of...

Q1: If Jasim purchase a put option on Canadian dollar from Sara for a premium of...

Q1: If Jasim purchase a put option on Canadian dollar from Sara for a premium of € 0.03, with an exercise price of € 0.42. The option will not be exercised until the expiration date, if at all. If the spot rate on the expiration date is € 0.37. a) What is the net profit for Jasim and Sara per unit? (1 mark) SZERE- ---ODDELEEEEEEEEEE -OOOOOOOOOOOOOOOOOOOOOOOOO SEBEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE b) If you know that one option contract represents 20000 units, what is...

Q1: If Jasim purchase a put option on Canadian dollar from Sara for a premium of € 0.03, with an exercise price of € 0.42. The option will not be exercised until the expiration date, if at all. If the spot rate on the expiration date is € 0.37. a) What is the net profit for Jasim and Sara per unit? (1 mark) SZERE- ---ODDELEEEEEEEEEE -OOOOOOOOOOOOOOOOOOOOOOOOO SEBEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE b) If you know that one option contract represents 20000 units, what is...

13. The premium on a pound put option is $.03 per unit. The exercise price is...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

NEED HELP You create a straddle with a call and put option with the same strike...

NEED HELP

You create a straddle with a call and put option with the same strike price of $50. The price of the call option is $4 and the price of the put option is $3. If the stock price is $18 at the maturity of the options, what is the net payoff from the straddle? A. $17 ம ப ்

NEED HELP

You create a straddle with a call and put option with the same strike price of $50. The price of the call option is $4 and the price of the put option is $3. If the stock price is $18 at the maturity of the options, what is the net payoff from the straddle? A. $17 ம ப ்

• Long cury strangle Call option premium - 50.03., Put option premium - $0.02 € Call option strike price 1.25/6, Put option strike price $1.15 € Option contract size - €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium 1 S105 S 15E $1.20 € $1.25 € $1.30/E Long call option Spot exchange rate Exercise (NY) Holder's net profit per unit Exercise (NY Holder's net profit per unit Net profit...

• Long cury strangle Call option premium - 50.03., Put option premium - $0.02 € Call option strike price 1.25/6, Put option strike price $1.15 € Option contract size - €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium 1 S105 S 15E $1.20 € $1.25 € $1.30/E Long call option Spot exchange rate Exercise (NY) Holder's net profit per unit Exercise (NY Holder's net profit per unit Net profit...

Compute the upper and lower breakeven point for a strangle. The exercise price on call option is $1.72 and the exercise price on put option is $1.55. The premium on put option is $0.014 and premium on call option is $0.01. a. $1.526 and -$1.744 b. $1.744 and $1.526 c. $1.734 and $1.526 d. $1.744 and $1.574

Compute the upper and lower breakeven point for a strangle. The exercise price on call option is $1.72 and the exercise price on put option is $1.55. The premium on put option is $0.014 and premium on call option is $0.01. a. $1.526 and -$1.744 b. $1.744 and $1.526 c. $1.734 and $1.526 d. $1.744 and $1.574

Why with 'long strangle', the loss is decreased if price remains

unchanged, compared with 'long straddle'?

Why the loss sustained by investors would be the double premium

( long strangle) which is same as the loss ( long straddle) equal

to double premium.

Market price of asset Premium- LOSS (c) Long call+ long put Profit Price expectations Market price of asset Net (double premium Loss c) Long put + long call Profit Price expectations ㅡ ㅡ ㅡㅡ Market p of...

Why with 'long strangle', the loss is decreased if price remains

unchanged, compared with 'long straddle'?

Why the loss sustained by investors would be the double premium

( long strangle) which is same as the loss ( long straddle) equal

to double premium.

Market price of asset Premium- LOSS (c) Long call+ long put Profit Price expectations Market price of asset Net (double premium Loss c) Long put + long call Profit Price expectations ㅡ ㅡ ㅡㅡ Market p of...

Q1: If Jasim purchase a put option on Canadian dollar from Sara for a premium of € 0.03, with an exercise price of € 0.42. The option will not be exercised until the expiration date, if at all. If the spot rate on the expiration date is € 0.37. a) What is the net profit for Jasim and Sara per unit? (1 mark) SZERE- ---ODDELEEEEEEEEEE -OOOOOOOOOOOOOOOOOOOOOOOOO SEBEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE b) If you know that one option contract represents 20000 units, what is...

Q1: If Jasim purchase a put option on Canadian dollar from Sara for a premium of € 0.03, with an exercise price of € 0.42. The option will not be exercised until the expiration date, if at all. If the spot rate on the expiration date is € 0.37. a) What is the net profit for Jasim and Sara per unit? (1 mark) SZERE- ---ODDELEEEEEEEEEE -OOOOOOOOOOOOOOOOOOOOOOOOO SEBEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE b) If you know that one option contract represents 20000 units, what is...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

NEED HELP

You create a straddle with a call and put option with the same strike price of $50. The price of the call option is $4 and the price of the put option is $3. If the stock price is $18 at the maturity of the options, what is the net payoff from the straddle? A. $17 ம ப ்

NEED HELP

You create a straddle with a call and put option with the same strike price of $50. The price of the call option is $4 and the price of the put option is $3. If the stock price is $18 at the maturity of the options, what is the net payoff from the straddle? A. $17 ம ப ்

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago