(a) Explain and discuss the discounted free cash flow equity valuation model. (b) CBT has reported...

(a) Explain and discuss the discounted free cash flow equity valuation model.

(b) CBT has reported EBIT of $500mn this year. Its net investment, including capital expenditure net of depreciation and working capital investment is $200mn. Its EBIT and investment needs are expected to grow at a constant rate of 1% per year. It is expected that CBT maintains the current debt-to-equity ratio of 4. The corporate tax rate is 20%. The required return on its assets (business) is 14%. The cost of the debt capital is 5%. The number of total outstanding shares is 100mn.

(i) Obtain the value of stock based on discounted free cash flow model. Explain your procedure.

(ii)What is the amount of tax shield in the enterprise value? Explain.

Homework Answers

Part (a)

Under discounted cash flow analysis to value a business or a business segment or a business combination, we look at two different types of free cash flows:

- Free cash flow to the firm (FCFF) given by:

This is post tax operating cash flow after capital expenditure.

- Free cash flow to equity holder (FCFE) given by:

If there is a preference share capital in the company, FCFE formula will also incorporate preferred stock dividend and will be given by:

FCFE is a cash flow which is free from all kinds of claims. It is a cash flow that ordinary equity holder can pocket safely. It’s the residual cash flow left after meeting all the liabilities, claims and investment needs of the company.

Steps involved in discounted cash flow valuation:

- Project FCFF / FCFE for a reasonable horizon of projection.

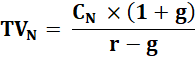

- Assume that the cash flows will grow at a constant growth rate (called terminal growth rate) beyond the horizon of projection. Calculate terminal value as present value of all the cash flows beyond the horizon period at the end of horizon period. This is given by equation:

Where TVN is the terminal value at the end of horizon of projection of N years, CN is the cash flow in the last year of horizon of projection (i.e. year N), “g” is terminal growth rate and “r” is the discount rate. Alternatively, terminal value can also be calculated by applying any of the relative valuation multiple on the applicable parameter. EV / EBITDA multiple can be applied on EBITDA in the last year of projection to obtain the terminal enterprise value. P / B or P / E or P / Sales can be applied on ordinary (common) stock book value or earnings or Sales respectively to get the terminal equity value. The multiple chosen for terminal value should be consistent with the cash flow being discounted. Note that when you are discounting FCFF, you should use EV / EBITDA multiple for terminal enterprise value. You should use P / E or P / B or P / Sales multiple to obtain terminal equity value when you are discounting FCFE.

- Discount the cash flows and

terminal value using the discount rate to obtain their present

values at year 0. Appropriate discount rate is:

- WACC when FCFF is used

- Cost of equity when FCFE is used

- Sum total of all the present value of future cash flows is the valuation today at year 0. When FCFF is used, the resultant valuation is called “Enterprise Value (EV)” of “Value of the firm”. All potential non-operating liabilities and claims need to be removed from the EV to get the equity value. Enterprise value = Value of the net debt (short term as well long term) + Value of preference stock (if any) + Value of the common equity. Hence, value of ordinary equity stock (or common stock) = Enterprise value – Value of net debt – value of preference stock (if any). Net debt = Total debt (short term as well as long term) – Surplus cash. Hence, When FCFE is discounted under discounted cash flow analysis, one ends up getting the “common equity value” or “ordinary equity value” directly.

This concept can be applied to valuing a business, a business segment, a company or a stock, a business combination by using the following analogous parameters:

|

Sl. No. |

Situation |

Business |

Business Segment |

Company / stock |

Business combination |

|

1. |

Cash flows |

Cash flows for the entire business that needs to be valued |

Cash flows only from the business segment under consideration |

Cash flows of the entire company include all businesses, segments, verticals etc. |

Cash flows of the target under consideration |

|

2. |

Discount rate |

Discount rate applicable to the particular business. Surrogate can be WACC of the business |

Discount rate applicable to the particular business segment. Surrogate can be WACC of that particular business segment |

Discount rate applicable to the overall firm. Surrogate can be WACC of the firm. |

Discount rate applicable to the acquirer. Surrogate can be WACC of the acquirer or WACC of target or WACC based on funding mix for acquisition |

Further note that:

- If a firm is undertaking a new project, the enterprise value (or firm’s value) or equity value of the firm will increase by a quantum equal to the NPV of the project. That’s why we have been harping in the previous sections that a positive NPV leads to shareholders’ wealth creation.

- We have already been through various forms of dividend discount models for equity valuation. All those models of equity valuation are also applicable if FCFE is used instead of dividends. FCFE is in a way maximum free cash flow available for distribution as dividend to the shareholders. Recall that all the variants of dividend discount model uses cost of equity as a discount rate.

Part (b)

(i) FCFF1 = EBIT0 x (1 + g) x (1 - T) - Net investment0 x (1 + g) = 500 x (1 - 20%) x (1 + 1%) - 200 x (1 + 1%) = $ 202 million

Unlevered cost of equity = Keu = 14%; Kd = 5%; D / E = 4

Hence, levered cost of equity, Ke = Keu + (Keu - Kd) x D / E = 14% + (14% - 5%) x 4 = 50%

Proportion of debt = Wd = D / (D + E) = 4 / (4 + 1) = 0.8

Proportion of equity = We = 1 - Wd = 1 - 0.8 = 0.2

Hence, WACC= r = Wd x Kd x (1 - T) + We x Ke = 0.8 x 5% x (1 - 20%) + 0.2 x 50% = 13.20%

Hence, Enterprise value = FCFF1 / (r - g) = 202 / (13.20% - 1%) = $ 1,656 mn

Value of stock = Enterprise value / Nos. of shares outstanding = 1,656 / 100 = $ 16.56 / share

Part (ii)

Value of the unlevered firm = FCFF1 / (Keu - g) = 202 / (14% - 1%) = $ 1,554 mn

Value of the levered firm = Value of the unlevered firm + value of tax shield

Hence, 1,656 = 1,554 + Value of tax shield

Hence, value of tax shield = 1,656 - 1,554 = $ 102 mn

Add Answer to:

(a) Explain and discuss the discounted free cash flow equity

valuation model.

(b) CBT has reported...

CBT has reported EBIT of $100mn this year. Its total capital expenditure is $20mn and depreciation...

CBT has reported EBIT of $100mn this year. Its total capital expenditure is $20mn and depreciation is $10mn this year. This year’s account receivables and account payables are $5mn and $2mn, respectively. The net working capital was $10mn last year and $20mn this year, respectively. Both the company’s EBIT and investment (including tangible and working capital) needs are expected to grow at a constant rate of 1% per year. It is expected that CBT maintains the current debt-to-equity ratio of...

Basic Stock Valuation: Free Cash Flow Valuation Model The recognition that dividends are dependent on earnings,...

Basic Stock Valuation: Free Cash Flow Valuation Model The recognition that dividends are dependent on earnings, so a reliable dividend forecast is based on an underlying forecast of the firm's future sales, costs and capital requirements, has led to an alternative stock valuation approach, known as the free cash flow valuation model. The market value of a firm is equal to the present value of its expected future free cash flows: Market value of company FCF (1+WACC) + FCF (1+WACC)...

Basic Stock Valuation: Free Cash Flow Valuation Model The recognition that dividends are dependent on earnings, so a reliable dividend forecast is based on an underlying forecast of the firm's future sales, costs and capital requirements, has led to an alternative stock valuation approach, known as the free cash flow valuation model. The market value of a firm is equal to the present value of its expected future free cash flows: Market value of company FCF (1+WACC) + FCF (1+WACC)...

Problem #1 Free Cash Flow Model ABC Company has an equity beta of 1.72 and a...

Problem #1 Free Cash Flow Model ABC Company has an equity beta of 1.72 and a tax rate of 35%. What is the asset beta if the debt to equity ratio is 40%? Using the answer from above, calculate the discount rate if the risk free rate is 2.75% and the market risk premium is 6.15%? ABC Company had an EBIT last year of $15.6 million. Depreciation expense was $1.45 million. In other areas, ABC spent $1.75 million on capital...

Flagstaff Enterprises expected to have free cash flow in the coming year of $8 million, and...

Flagstaff Enterprises expected to have free cash flow in the coming year of $8 million, and this free cash flow is expected to grow at a rate of 3% per year thereafter. Flagstaff has an equity cost of capital of 13%, a debt cost of capital of 7%, and it is in the 35% corporate tax bracket. If Flagstaff currently maintains a 0.5 debt to equity ratio, then the value of Flagstaffʹs interest tax shield is closest to (all calculations...

Which one of the following factors is not considered in calculating the firm’s cost of equity? risk free rate of retu...

Which one of the following factors is not considered in calculating the firm’s cost of equity? risk free rate of return beta interest rate on corporate debt expected return on equities difference between expected return on stocks and the risk free rate of return Which one of the following factors is not considered in calculating the firm’s cost of capital? cost of equity interest rate on debt the firm’s marginal tax rate book value of debt and equity the firm’s...

4. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic...

4. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic value added (EVA) approach are some examples of valuation techniques. The corporate valuation model is similar to the dividend-based valuation that you've done in previous problems, but it focuses on a firm's free cash flows (FCFS) instead of its dividends. Some firms don't pay dividends, or their dividends are difficult to forecast. For that reason, some analysts use the corporate valuation model. Charles Underwood Agency Inc....

4. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic value added (EVA) approach are some examples of valuation techniques. The corporate valuation model is similar to the dividend-based valuation that you've done in previous problems, but it focuses on a firm's free cash flows (FCFS) instead of its dividends. Some firms don't pay dividends, or their dividends are difficult to forecast. For that reason, some analysts use the corporate valuation model. Charles Underwood Agency Inc....

West Fraser Timber Company (WFT) is expected to have free cash flow in the coming year...

West Fraser Timber Company (WFT) is expected to have free cash flow in the coming year of $2 million and its free cash flow is expected maintain at a sustainable growth rate of 4% per year. It has a debt worth $10 million. It’s equity cost of capital is 12%, cost of debt before tax is 6%, and it pays a corporate tax rate of 30%. If WFT Company maintains a debt-equity ratio of 0.5 and the company has 3...

Which of the following is true of the equity valuation model? a. Discounts free cash...

Which of the following is true of the equity valuation model? a. Discounts free cash flow to the firm by the weighted average cost of capital b. Discounts free cash flow to equity by the cost of equity c. Discounts free cash flow the firm by the cost of equity d. Discounts free cash flow to equity by the weighted average cost of capital e. None of the above

10. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic...

10. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic value added (EVA) approach are some examples of valuation techniques. The corporate valuation model is similar to the dividend-based valuation that you've done in previous problems, but it focuses on a firm's free cash flows (FCFS) instead of its dividends. Some firms don't pay dividends, or their dividends are difficult to forecast. For that reason, some analysts use the corporate valuation model. Blur Corp....

10. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic value added (EVA) approach are some examples of valuation techniques. The corporate valuation model is similar to the dividend-based valuation that you've done in previous problems, but it focuses on a firm's free cash flows (FCFS) instead of its dividends. Some firms don't pay dividends, or their dividends are difficult to forecast. For that reason, some analysts use the corporate valuation model. Blur Corp....

8. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic...

8. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic value added (EVA) approach are some examples of valuation techniques. The corporate valuation model is similar to the dividend-based valuation that you’ve done in previous problems, but it focuses on a firm’s free cash flows (FCFs) instead of its dividends. Some firms don’t pay dividends, or their dividends are difficult to forecast. For that reason, some analysts use the corporate valuation model. Stay Swift...

Basic Stock Valuation: Free Cash Flow Valuation Model The recognition that dividends are dependent on earnings, so a reliable dividend forecast is based on an underlying forecast of the firm's future sales, costs and capital requirements, has led to an alternative stock valuation approach, known as the free cash flow valuation model. The market value of a firm is equal to the present value of its expected future free cash flows: Market value of company FCF (1+WACC) + FCF (1+WACC)...

Basic Stock Valuation: Free Cash Flow Valuation Model The recognition that dividends are dependent on earnings, so a reliable dividend forecast is based on an underlying forecast of the firm's future sales, costs and capital requirements, has led to an alternative stock valuation approach, known as the free cash flow valuation model. The market value of a firm is equal to the present value of its expected future free cash flows: Market value of company FCF (1+WACC) + FCF (1+WACC)...

4. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic value added (EVA) approach are some examples of valuation techniques. The corporate valuation model is similar to the dividend-based valuation that you've done in previous problems, but it focuses on a firm's free cash flows (FCFS) instead of its dividends. Some firms don't pay dividends, or their dividends are difficult to forecast. For that reason, some analysts use the corporate valuation model. Charles Underwood Agency Inc....

4. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic value added (EVA) approach are some examples of valuation techniques. The corporate valuation model is similar to the dividend-based valuation that you've done in previous problems, but it focuses on a firm's free cash flows (FCFS) instead of its dividends. Some firms don't pay dividends, or their dividends are difficult to forecast. For that reason, some analysts use the corporate valuation model. Charles Underwood Agency Inc....

10. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic value added (EVA) approach are some examples of valuation techniques. The corporate valuation model is similar to the dividend-based valuation that you've done in previous problems, but it focuses on a firm's free cash flows (FCFS) instead of its dividends. Some firms don't pay dividends, or their dividends are difficult to forecast. For that reason, some analysts use the corporate valuation model. Blur Corp....

10. Corporate valuation model The corporate valuation model, the price-to-earnings (P/E) multiple approach, and the economic value added (EVA) approach are some examples of valuation techniques. The corporate valuation model is similar to the dividend-based valuation that you've done in previous problems, but it focuses on a firm's free cash flows (FCFS) instead of its dividends. Some firms don't pay dividends, or their dividends are difficult to forecast. For that reason, some analysts use the corporate valuation model. Blur Corp....

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago