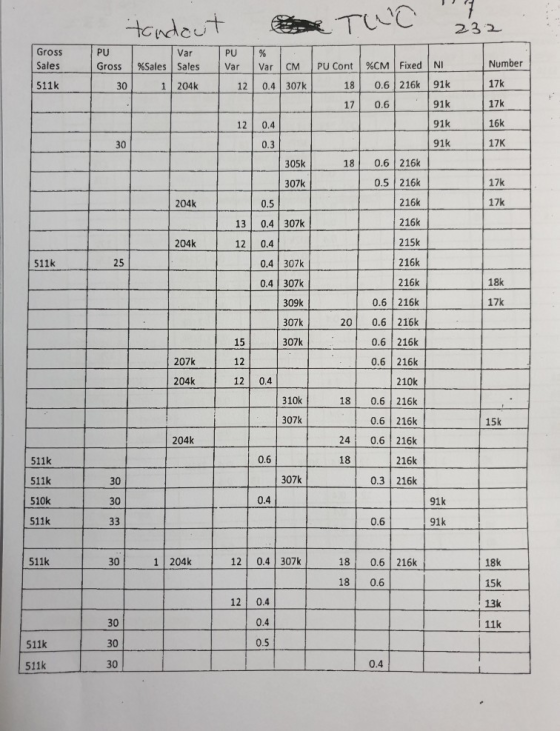

please, fill up the empty boxes. handout 1. from gross sales to number.

please, fill up the empty boxes. handout

2. from gross sales to number.

Homework Answers

ANSWERS OF 1ST PAGE.

1. Assumptions of CVP analysis

The assumptions underlying CVP analysis are: The behavior of both costs and revenues are linear throughout the relevant range of activity. (This assumption precludes the concept of volume discounts on either purchased materials or sales.) Costs can be classified accurately as either fixed or variable.

2. Definition of Leverage ratio

A leverage ratio is any kind of financial ratio that indicates the level of debt incurred by a business entity against several other accounts in its balance sheet, income statement, or cash flow statement. These ratios provide an indication of how the company’s assets and business operations are financed (using debt or equity).

List of common leverage ratios

- Debt-to-Assets Ratio = Total Debt / Total Assets

- Debt-to-Equity Ratio = Total Debt / Total Equity

- Debt-to-Capital Ratio = Today Debt / (Total Debt + Total Equity)

- Debt-to-EBITDA Ratio = Total Debt / Earnings Before Interest Taxes Depreciation & Amortization (EBITDA)

- Asset-to-Equity Ratio = Total Assets / Total Equity

Various types of leverage

Operating leverage is a measure of the combination of fixed costs and variable costs in a company's cost structure. A company with high fixed costs and low variable costs has high operating leverage; whereas a company with low fixed costs and high variable costs has low operating leverage

Financial leverage is the use of debt to buy more assets. Leverage is employed to increase the return on equity. However, an excessive amount of financial leverage increases the risk of failure, since it becomes more difficult to repay debt

Combined leverage is a leverage which refers to high profits due to fixed costs. It includes fixed operating expenses with fixed financial expenses. It indicates leverage benefits and risks which are in fixed quantity. ... Degree of combined leverage indicates benefits and risks involved in this particular leverage.

3. MARGIN OF SAFETY

Margin of safety is a principle of investing in which an investor only purchases securities when their market price is significantly below their intrinsic value. In other words, when the market price of a security is significantly below your estimation of its intrinsic value, the difference is the margin of safety.

4. BREAK EVEN POINT (UNITS & SALES)

It's defined as the point where sales and expenses are the same or when the sales of a company are enough to cover the expenses of the business. ... Break-Even Point in Units = Fixed Costs / (Sales Price Per Unit - Variable Costs) Break-Even Point in $ = Sales Price Per Unit x Break-Even Point in Units.

5. VARIABLE COST

A variable cost is a corporate expense that changes in proportion to production output. Variable costs increase or decrease depending on a company's production volume; they rise as production increases and fall as production decreases. Examples of variable costs include the costs of raw materials and packaging.

6. FIXED COST

A fixed cost is a cost that does not change with an increase or decrease in the amount of goods or services produced or sold. Fixed costs are expenses that have to be paid by a company, independent of any specific business activities

7. TARGET INCOME

Target income is the profit that the managers of a company expect to attain for a designated accounting period. It is a key concept in a corporate control system that drives corrective management actions. The term is used in the following situations: Budgeting

8. CONTRIBUTION MARGIN

The contribution margin is the sales price of a unit, minus the variable costs involved in the unit's production. It is used to find an optimal price point for a product. It also measures whether the product is generating enough revenue to pay for fixed costs and determine the profit it is generating.

Add Answer to:

please, fill up the empty boxes. handout 1. from gross

sales to number.

please, fill...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago