Homework Answers

Please find the solution in the below images

Add Answer to:

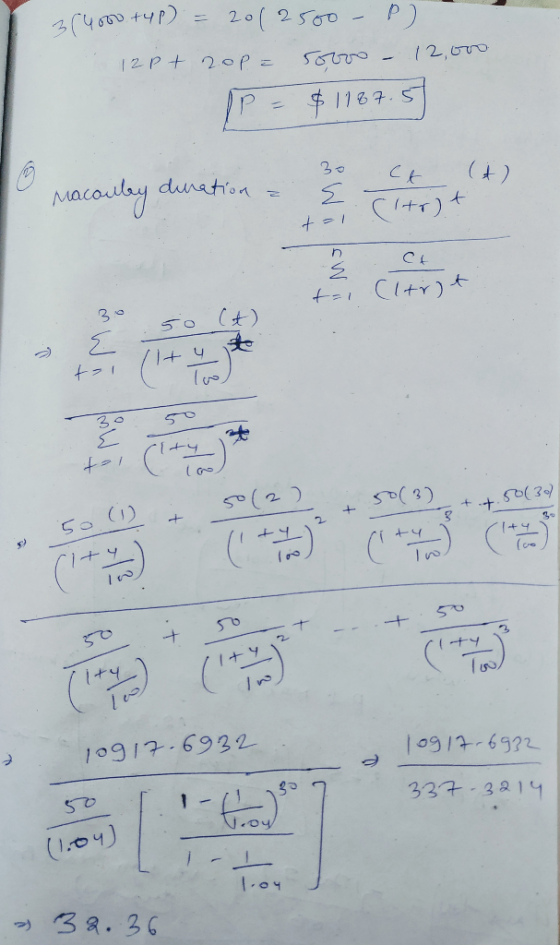

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value...

possible answers are 0.5%, 1%, 1.5%,2%,2.5% 25. A 15-year bond with annual coupons sold at par...

possible answers are 0.5%, 1%, 1.5%,2%,2.5%

25. A 15-year bond with annual coupons sold at par of 1,000 has a Macaulay duration of 9.0101. If the annual effective yield rate of the bond decreases by x, the price of the bond approximated using the first-order Macaulay approximation is 1,233.72. Calculate x.

possible answers are 0.5%, 1%, 1.5%,2%,2.5%

25. A 15-year bond with annual coupons sold at par of 1,000 has a Macaulay duration of 9.0101. If the annual effective yield rate of the bond decreases by x, the price of the bond approximated using the first-order Macaulay approximation is 1,233.72. Calculate x.

Sue buys a 10 year 1000 bond at par. The Macaulay duration is 8.329 years using...

Sue buys a 10 year 1000 bond at par. The Macaulay duration is 8.329 years using an annual effective interest rate of 6.8%. a. Calculate the estimated price of the bond, using the first-order modified approximation if the interest rate rises to 7%.

Sue buys a 10 year 1000 bond at par. The Macaulay duration is 8.329 years using an annual effective interest rate of 6.8%. a. Calculate the estimated price of the bond, using the first-order modified approximation if the interest rate rises to 7%.

1000 euro par value, 3% annual-coupon bond was issued 1.03.2015 and has 30 year maturity You...

1000 euro par value, 3% annual-coupon bond was issued 1.03.2015 and has 30 year maturity You purchased the bond on 20.10.2018 Market interest rate for similar securities is 2,8% Calculate following: a. Clean price b. Acrrued interest c. Full price d. Macaulay duration e. Modified duration If interest rate in the market declines by 50 bps g. Calculate new price with duration

1000 euro par value, 3% annual-coupon bond was issued 1.03.2015 and has 30 year maturity You purchased the bond on 20.10.2018 Market interest rate for similar securities is 2,8% Calculate following: a. Clean price b. Acrrued interest c. Full price d. Macaulay duration e. Modified duration If interest rate in the market declines by 50 bps g. Calculate new price with duration

1. Nov, 2005 #2. Calculate the Macaulay duration of an eight-year 100 par value bond with...

1. Nov, 2005 #2. Calculate the Macaulay duration of an eight-year 100 par value bond with 10% annual coupons and an effective rate of interest equal to 8%. (A) 4 (B) 5 (C) 6 (D) 7 (E) 8

1. Nov, 2005 #2. Calculate the Macaulay duration of an eight-year 100 par value bond with 10% annual coupons and an effective rate of interest equal to 8%. (A) 4 (B) 5 (C) 6 (D) 7 (E) 8

please answer the questions according to the marks appointed per question and sub question. this is...

please answer the questions according to the marks appointed per

question and sub question. this is a banking and finance question

so please answer it accordingly.

8. (a) Explain the concept of Macaulay duration and explain the relationship between Macaulay duration and: (i) bond maturity (ii) interest rates (iii) bond coupon rate (7 marks) (b) Calculate the price and Macaulay duration of a five-year 5% coupon bond where the market interest rate is 5%. Assume the par value of the...

please answer the questions according to the marks appointed per

question and sub question. this is a banking and finance question

so please answer it accordingly.

8. (a) Explain the concept of Macaulay duration and explain the relationship between Macaulay duration and: (i) bond maturity (ii) interest rates (iii) bond coupon rate (7 marks) (b) Calculate the price and Macaulay duration of a five-year 5% coupon bond where the market interest rate is 5%. Assume the par value of the...

You just purchased a $1000 par value bond maturing on 30th June 2025. Suppose today’s date...

You just purchased a $1000 par value bond maturing on 30th June 2025. Suppose today’s date (settlement date) is 30th June 2019 and the yield to maturity is 6%. Given all these inputs, do the following. a) Assume the bond is a zero coupon bond (with annual compounding). Compute the bond’s Macaulay duration (using the DURATION function) and modified duration (using the MDURATION function). b) Holding everything else constant, now assume the bond pays coupons semi-annually. Compute the bond’s Macaulay...

Bond Analysis Issue data Purchase date Maturity date Par value Coupon rate Frequency Market price October...

Bond Analysis Issue data Purchase date Maturity date Par value Coupon rate Frequency Market price October 12,2002 September 26,2012 November 24,2019 2279 1.5100% annually 94% All values must be rounded up to 2 decimals Characteristics Value 1 Yield to maturity <> 2 Macaulay duration <> 3 Modified duration <> 4 If the yield-to-maturity increases by 100 bps,the bond price will be changed by (calculate it precisely) <> 5 If the yield-to- maturity increases by 10 bps, the bond price will...

Graph (show the cash flows) of the following bond: a. A $20,000 par value bond with...

Graph (show the cash flows) of the following bond: a. A $20,000 par value bond with a coupon of 4.0% paid semi-annually, maturing in 6 years. b. Find the current price of the Bond if you use 4.0% as the discount rate. c. Is this bond priced at a discount or a premium? Macaulay Duration: a. Calculate the price of a bond with a Face Value of $1,000, with an ANNUAL coupon of 10% (not paid semi-annually, but once a...

A $1,000 par value bond pays an annual coupon of 10.0% and matures in 4 years....

A $1,000 par value bond pays an annual coupon of 10.0% and matures in 4 years. If the bond sells to yield 7%, what is the modified duration of this bond? a) The regular duration is: b) The modified duration is:

Calculate the Macaulay duration of a 10%, $1,000 par bond that matures in three years if...

Calculate the Macaulay duration of a 10%, $1,000 par bond that

matures in three years if the bond's YTM is 12% and interest is

paid semiannually.

Calculate this bond's modified duration (years). Do not round

intermediate calculations. Round your answer to two decimal

places.

Assuming the bond's YTM goes from 12% to 10.5%, calculate an

estimate of the price change. Do not round intermediate

calculations. Round your answer to three decimal places (in %). Use

a minus sign to enter...

Calculate the Macaulay duration of a 10%, $1,000 par bond that

matures in three years if the bond's YTM is 12% and interest is

paid semiannually.

Calculate this bond's modified duration (years). Do not round

intermediate calculations. Round your answer to two decimal

places.

Assuming the bond's YTM goes from 12% to 10.5%, calculate an

estimate of the price change. Do not round intermediate

calculations. Round your answer to three decimal places (in %). Use

a minus sign to enter...

possible answers are 0.5%, 1%, 1.5%,2%,2.5%

25. A 15-year bond with annual coupons sold at par of 1,000 has a Macaulay duration of 9.0101. If the annual effective yield rate of the bond decreases by x, the price of the bond approximated using the first-order Macaulay approximation is 1,233.72. Calculate x.

possible answers are 0.5%, 1%, 1.5%,2%,2.5%

25. A 15-year bond with annual coupons sold at par of 1,000 has a Macaulay duration of 9.0101. If the annual effective yield rate of the bond decreases by x, the price of the bond approximated using the first-order Macaulay approximation is 1,233.72. Calculate x.

Sue buys a 10 year 1000 bond at par. The Macaulay duration is 8.329 years using an annual effective interest rate of 6.8%. a. Calculate the estimated price of the bond, using the first-order modified approximation if the interest rate rises to 7%.

Sue buys a 10 year 1000 bond at par. The Macaulay duration is 8.329 years using an annual effective interest rate of 6.8%. a. Calculate the estimated price of the bond, using the first-order modified approximation if the interest rate rises to 7%.

1000 euro par value, 3% annual-coupon bond was issued 1.03.2015 and has 30 year maturity You purchased the bond on 20.10.2018 Market interest rate for similar securities is 2,8% Calculate following: a. Clean price b. Acrrued interest c. Full price d. Macaulay duration e. Modified duration If interest rate in the market declines by 50 bps g. Calculate new price with duration

1000 euro par value, 3% annual-coupon bond was issued 1.03.2015 and has 30 year maturity You purchased the bond on 20.10.2018 Market interest rate for similar securities is 2,8% Calculate following: a. Clean price b. Acrrued interest c. Full price d. Macaulay duration e. Modified duration If interest rate in the market declines by 50 bps g. Calculate new price with duration

1. Nov, 2005 #2. Calculate the Macaulay duration of an eight-year 100 par value bond with 10% annual coupons and an effective rate of interest equal to 8%. (A) 4 (B) 5 (C) 6 (D) 7 (E) 8

1. Nov, 2005 #2. Calculate the Macaulay duration of an eight-year 100 par value bond with 10% annual coupons and an effective rate of interest equal to 8%. (A) 4 (B) 5 (C) 6 (D) 7 (E) 8

please answer the questions according to the marks appointed per

question and sub question. this is a banking and finance question

so please answer it accordingly.

8. (a) Explain the concept of Macaulay duration and explain the relationship between Macaulay duration and: (i) bond maturity (ii) interest rates (iii) bond coupon rate (7 marks) (b) Calculate the price and Macaulay duration of a five-year 5% coupon bond where the market interest rate is 5%. Assume the par value of the...

please answer the questions according to the marks appointed per

question and sub question. this is a banking and finance question

so please answer it accordingly.

8. (a) Explain the concept of Macaulay duration and explain the relationship between Macaulay duration and: (i) bond maturity (ii) interest rates (iii) bond coupon rate (7 marks) (b) Calculate the price and Macaulay duration of a five-year 5% coupon bond where the market interest rate is 5%. Assume the par value of the...

Calculate the Macaulay duration of a 10%, $1,000 par bond that

matures in three years if the bond's YTM is 12% and interest is

paid semiannually.

Calculate this bond's modified duration (years). Do not round

intermediate calculations. Round your answer to two decimal

places.

Assuming the bond's YTM goes from 12% to 10.5%, calculate an

estimate of the price change. Do not round intermediate

calculations. Round your answer to three decimal places (in %). Use

a minus sign to enter...

Calculate the Macaulay duration of a 10%, $1,000 par bond that

matures in three years if the bond's YTM is 12% and interest is

paid semiannually.

Calculate this bond's modified duration (years). Do not round

intermediate calculations. Round your answer to two decimal

places.

Assuming the bond's YTM goes from 12% to 10.5%, calculate an

estimate of the price change. Do not round intermediate

calculations. Round your answer to three decimal places (in %). Use

a minus sign to enter...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago