Homework Answers

The answers are as follows:

Add Answer to:

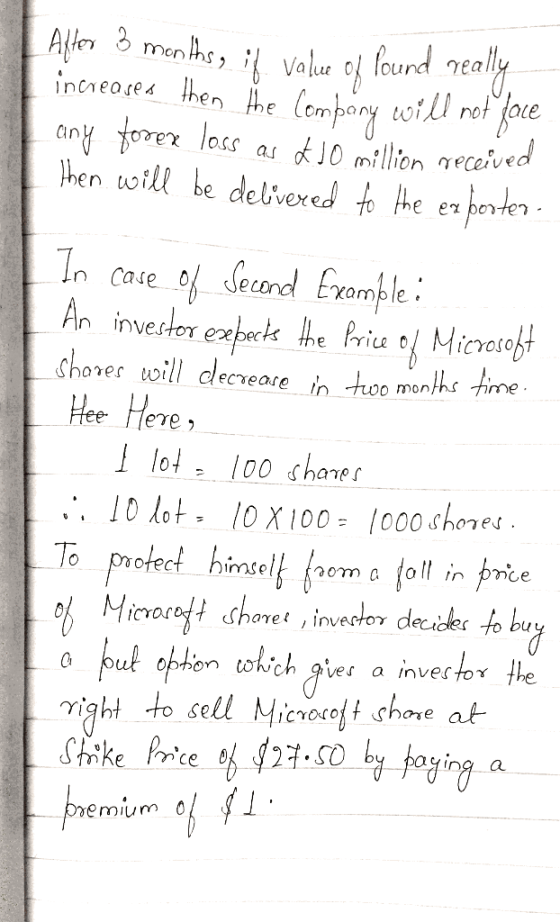

Hedging Examples (pages 10-12) o buy) A US company will pay £10 million for imports from...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging strategy...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging strategy...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging strategy...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging strategy...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging strategy...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging strategy...

) A U.S. firm imports €10 million of goods from a German firm, and needs to...

) A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging...

One company in the US knows that it will have to pay 30 million euros in...

One company in the US knows that it will have to pay 30 million euros in three months. The current exchange rate is $ 1.08 per euro. a. At what risk is the company exposed? b. Explain how she could use forward contracts to hedge her report. c. Explain how she could use Futures to offset her report. d. If it had decided to hedge its position on forward contracts, when would it have made a profit and when had...

a US. company, sold equipment to a French company for Euro 100 million. Payment is due...

a US. company, sold equipment to a French company for Euro 100 million. Payment is due in 90 days. Answer the following questions (24-26) using the information below: Current spot rate 90 day Forward rate $.95/E $.98/E Interest rate in U.S Interest rate in France 6% PA. 896 PA. Call option Strike price Premium S.97/E 3% Put option Strike price Premium $.97/E 496 24. If a firm uses a money market hedge, how much money should the firm get in...

a US. company, sold equipment to a French company for Euro 100 million. Payment is due in 90 days. Answer the following questions (24-26) using the information below: Current spot rate 90 day Forward rate $.95/E $.98/E Interest rate in U.S Interest rate in France 6% PA. 896 PA. Call option Strike price Premium S.97/E 3% Put option Strike price Premium $.97/E 496 24. If a firm uses a money market hedge, how much money should the firm get in...

Airbus sold an aircraft, A400, to Delta Airlines, a U.S. company, and billed $30 million payable...

Airbus sold an aircraft, A400, to Delta Airlines, a U.S. company, and billed $30 million payable in six months. Airbus is concerned with the euro proceeds from international sales and would like to control exchange risk. The current spot exchange rate is $1.05/€ and six-month forward exchange rate is $1.10/€ at the moment. Airbus can buy a six-month put option on U.S. dollars with a strike price of €0.95/$ for a premium of €0.02 per U.S. dollar. Currently, six-month interest...

a US. company, sold equipment to a French company for Euro 100 million. Payment is due in 90 days. Answer the following questions (24-26) using the information below: Current spot rate 90 day Forward rate $.95/E $.98/E Interest rate in U.S Interest rate in France 6% PA. 896 PA. Call option Strike price Premium S.97/E 3% Put option Strike price Premium $.97/E 496 24. If a firm uses a money market hedge, how much money should the firm get in...

a US. company, sold equipment to a French company for Euro 100 million. Payment is due in 90 days. Answer the following questions (24-26) using the information below: Current spot rate 90 day Forward rate $.95/E $.98/E Interest rate in U.S Interest rate in France 6% PA. 896 PA. Call option Strike price Premium S.97/E 3% Put option Strike price Premium $.97/E 496 24. If a firm uses a money market hedge, how much money should the firm get in...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago