Using a binomial tree, calculate the price of a $40 strike 6-month call option, using 3-month...

Using a binomial tree, calculate the price of a $40 strike 6-month call option, using 3-month intervals as the time period. Using the US system. Assume the following data: S = $37.90, r = 5.0%, σ = 30%.

Homework Answers

Add Answer to:

Using a binomial tree, calculate the price of a $40 strike

6-month call option, using 3-month...

Using a binomial tree, what is the price of a $40 strike 6-month American put option,...

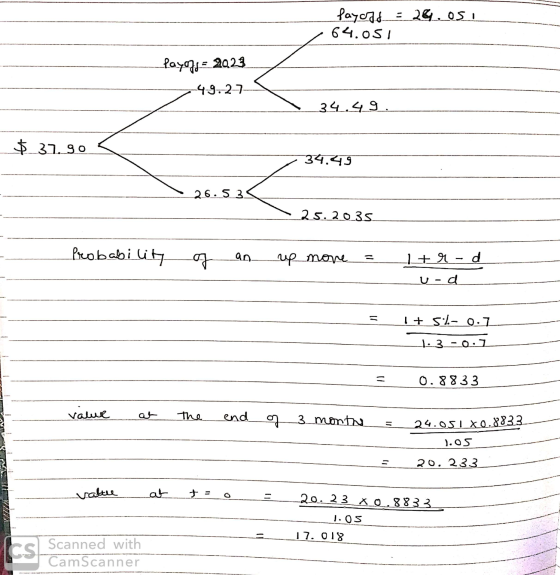

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

Part II (Binomial Tree) ai' 1. Compute the price of a call option using the stock...

Part II (Binomial Tree) ai' 1. Compute the price of a call option using the stock price tree u1.4634 and d=0.7317. The stock price is $38. The strike price is 840 and the interest rate is 8%. The time-period is 6 month. Use a 2 stage binomial tree 2. Assume that where ?-8%, the dividend yield ?. 0, ? is the annual standard deviation and ?VE is the standard deviation over a period of length h. The initial stock price...

Part II (Binomial Tree) ai' 1. Compute the price of a call option using the stock price tree u1.4634 and d=0.7317. The stock price is $38. The strike price is 840 and the interest rate is 8%. The time-period is 6 month. Use a 2 stage binomial tree 2. Assume that where ?-8%, the dividend yield ?. 0, ? is the annual standard deviation and ?VE is the standard deviation over a period of length h. The initial stock price...

A stock price is currently $100. A call option on this stock with a strike price...

A stock price is currently $100. A call option on this stock with a strike price of $100 and one year to maturity costs $13.61. The continuous-time interest rate is 5%. By using a one-step binomial tree, estimate the expected volatility level (σ) for the stock. Assume that u and d are modeled as below. ( Excel's Goal Seek will help solving this and will be much appreciated to be posted to see how it has been used to solve this problem, thanks)...

Calculate the price of a 6-month index call option with 1000 strike price using the following...

Calculate the price of a 6-month index call option with 1000 strike price using the following information. Current index level 1,083 Index dividend yield 1% per annum Risk-free rate 4% per annum 6-m index put option price w/ 1000 K $34.94 Round the the nearest 2 decimal points. For example, if your answer is $123.456, then enter "123.46"

A 1-year European call option is modeled with a 1-period binomial tree with u = 1.2, d = 0.7.

A 1-year European call option is modeled with a 1-period binomial tree with u = 1.2, d = 0.7. The stock price is 50. The strike price is 55. The stock pays no dividends. The call premium is 3.10. σ = 0.25.Determine the risk-free rate

Asian call option with strike equal to 100. Find the price of an Asian 2 month...

Asian call option with strike equal to 100. Find the price of an Asian 2 month option on a stock that currently trades at 100$ and its price will go up in each month by 40% with probability of 3/5, and will go down by 30% with probability of 2/5. The payoff of the Asian option is determined by the average underlying price over the period after buying option and the time of exercise. 1-month risk-free rate is 2%

A call option has a premium of $0.60, a strike price of $40, and 3 months...

A call option has a premium of $0.60, a strike price of $40, and 3 months to expiration. The current stock price is $39.60. The stock will pay a $0.80 dividend two months from now. The risk-free rate is 3 percent. What is the premium on a 3-month put with a strike price of $40? Assume the options are European style.

14. A call option has a premium of $0.60, a strike price of $40, and 3...

14. A call option has a premium of $0.60, a strike price of $40, and 3 months to expiration. The current stock price is $39.60. The stock will pay a $0.80 dividend two months from now. The risk-free rate is 3 percent. What is the premium on a 3-month put with a strike price of $40? Assume the options are European style. Page 4

14. A call option has a premium of $0.60, a strike price of $40, and 3 months to expiration. The current stock price is $39.60. The stock will pay a $0.80 dividend two months from now. The risk-free rate is 3 percent. What is the premium on a 3-month put with a strike price of $40? Assume the options are European style. Page 4

Finance - option pricing: Alex is looking to price a 6-month European put option with a...

Finance - option pricing:

Alex is looking to price a 6-month European put option with a strike price of $29 on a share in Omni Consumer Products (OCP). The current price for an OCP share is $30. Alex has used past data and his own judgement to estimate the volatility of these shares to be 15% per annum. The risk-free continuously compounding interest rate is 5% per year. a) Construct a 3-step binomial tree showing the possible share prices over...

Finance - option pricing:

Alex is looking to price a 6-month European put option with a strike price of $29 on a share in Omni Consumer Products (OCP). The current price for an OCP share is $30. Alex has used past data and his own judgement to estimate the volatility of these shares to be 15% per annum. The risk-free continuously compounding interest rate is 5% per year. a) Construct a 3-step binomial tree showing the possible share prices over...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annu...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

Part II (Binomial Tree) ai' 1. Compute the price of a call option using the stock price tree u1.4634 and d=0.7317. The stock price is $38. The strike price is 840 and the interest rate is 8%. The time-period is 6 month. Use a 2 stage binomial tree 2. Assume that where ?-8%, the dividend yield ?. 0, ? is the annual standard deviation and ?VE is the standard deviation over a period of length h. The initial stock price...

Part II (Binomial Tree) ai' 1. Compute the price of a call option using the stock price tree u1.4634 and d=0.7317. The stock price is $38. The strike price is 840 and the interest rate is 8%. The time-period is 6 month. Use a 2 stage binomial tree 2. Assume that where ?-8%, the dividend yield ?. 0, ? is the annual standard deviation and ?VE is the standard deviation over a period of length h. The initial stock price...

14. A call option has a premium of $0.60, a strike price of $40, and 3 months to expiration. The current stock price is $39.60. The stock will pay a $0.80 dividend two months from now. The risk-free rate is 3 percent. What is the premium on a 3-month put with a strike price of $40? Assume the options are European style. Page 4

14. A call option has a premium of $0.60, a strike price of $40, and 3 months to expiration. The current stock price is $39.60. The stock will pay a $0.80 dividend two months from now. The risk-free rate is 3 percent. What is the premium on a 3-month put with a strike price of $40? Assume the options are European style. Page 4

Finance - option pricing:

Alex is looking to price a 6-month European put option with a strike price of $29 on a share in Omni Consumer Products (OCP). The current price for an OCP share is $30. Alex has used past data and his own judgement to estimate the volatility of these shares to be 15% per annum. The risk-free continuously compounding interest rate is 5% per year. a) Construct a 3-step binomial tree showing the possible share prices over...

Finance - option pricing:

Alex is looking to price a 6-month European put option with a strike price of $29 on a share in Omni Consumer Products (OCP). The current price for an OCP share is $30. Alex has used past data and his own judgement to estimate the volatility of these shares to be 15% per annum. The risk-free continuously compounding interest rate is 5% per year. a) Construct a 3-step binomial tree showing the possible share prices over...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago