a. Assuming the budget was not amended, what was the budgetary journal entry recorded at the beginning of the fiscal year?

b. What is the Fund Balance?

c. Did the debt service find pay debt obligations related to lease agreements? (Y/N)

d. Did the debt service fund perform a debt refunding?

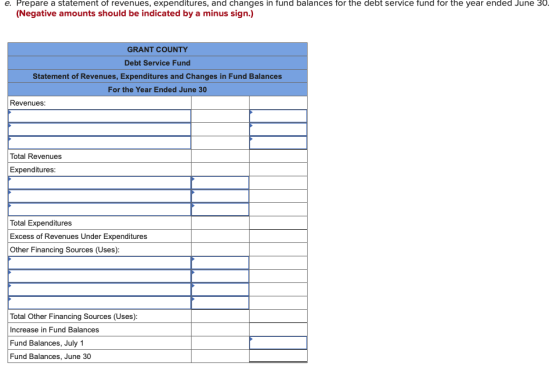

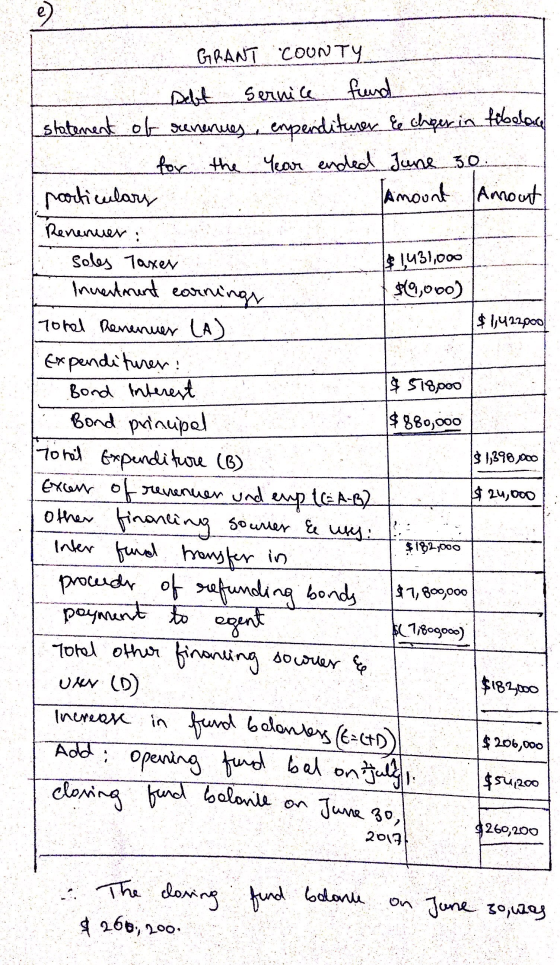

e.

Homework Answers

Add Answer to:

a. Assuming the budget was not amended, what was the budgetary

journal entry recorded at the...

· The City of Troutman had the following partial list of pre-closing account balances in its General Fund as of June...

· The City of Troutman had the following partial list of pre-closing account balances in its General Fund as of June 30, 2019. Debits Credits $3,675,000 385,000 111,000 60,000 107,000 290,000 Appropriations Control Budgetary Fund Balance Budgetary Fund Balance - Reserve for Encumbrances Due to Other Funds Encumbrances Control Estimated Other Financing Uses Control Estimated Revenues Control Expenditures Control Fund Balance Other Financing Uses Control-Transfers Out Revenues Control Taxes Receivable-Delinquent Vouchers Payable 3,860,000 3,405,000 272,000 315,000 3,968,000 85,000 275,000 Required:...

· The City of Troutman had the following partial list of pre-closing account balances in its General Fund as of June 30, 2019. Debits Credits $3,675,000 385,000 111,000 60,000 107,000 290,000 Appropriations Control Budgetary Fund Balance Budgetary Fund Balance - Reserve for Encumbrances Due to Other Funds Encumbrances Control Estimated Other Financing Uses Control Estimated Revenues Control Expenditures Control Fund Balance Other Financing Uses Control-Transfers Out Revenues Control Taxes Receivable-Delinquent Vouchers Payable 3,860,000 3,405,000 272,000 315,000 3,968,000 85,000 275,000 Required:...

The year-end pre-closing trial balance for the Chance County Woodland Park Capital Projects Fund is provided...

The year-end pre-closing trial balance for the Chance County Woodland Park Capital Projects Fund is provided below. Cash Grant Receivables Investments Contract Payable Contract Payable - Retained Percentage Encumbrances Outstanding Revenues Encumbrances Construction Expenditures Other Financing Sources - Proceeds of Bonds Debits Credits $ 987,000 600,000 1,800,000 $1,263, 588 66,500 1,625,000 707,600 1,625,000 4,150,000 4,700,890 $8,362,eee $8,362, eee Required a. Prepare the year-end statement of revenues, expenditures, and changes in fund balances for the capital projects fund, CHANCE COUNTY Woodland...

The year-end pre-closing trial balance for the Chance County Woodland Park Capital Projects Fund is provided below. Cash Grant Receivables Investments Contract Payable Contract Payable - Retained Percentage Encumbrances Outstanding Revenues Encumbrances Construction Expenditures Other Financing Sources - Proceeds of Bonds Debits Credits $ 987,000 600,000 1,800,000 $1,263, 588 66,500 1,625,000 707,600 1,625,000 4,150,000 4,700,890 $8,362,eee $8,362, eee Required a. Prepare the year-end statement of revenues, expenditures, and changes in fund balances for the capital projects fund, CHANCE COUNTY Woodland...

Record in general journal form entries to close the budgetary and operating statement accounts in the...

Record in general journal form entries to close the budgetary and operating statement accounts in the General Fund only. Do not close the governmental activities accounts. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations.) Debit Credit Transactions Fund General Journal 1. Record the closure of budgetary statements account General Fund Appropriations Estimated Revenues Budgetary Fund Balance 3,119,000 2. Record the closure of operating statements account....

Record in general journal form entries to close the budgetary and operating statement accounts in the General Fund only. Do not close the governmental activities accounts. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations.) Debit Credit Transactions Fund General Journal 1. Record the closure of budgetary statements account General Fund Appropriations Estimated Revenues Budgetary Fund Balance 3,119,000 2. Record the closure of operating statements account....

Listed below (in alphabetical order) are the general ledger and budgetary accounts for the City of...

Listed below (in alphabetical order) are the general ledger and budgetary accounts for the City of Walland. All balances are year-end, unless otherwise noted. All accounts have a normal balance. At the end of the year, the City Council passed an ordinance that all outstanding orders would be honored in the following fiscal year. Also, the Finance Officer set aside $40 for equipment replacement. City of Walland Preclosing Trial Balance For the Year Ended June 30, 20X9 Advance to Enterprise...

At the end of fiscal year 2017, the City of Georgetown's General Fund pre-adjusting trial balance...

At the end of fiscal year 2017, the City of Georgetown's General Fund pre-adjusting trial balance showed the following balances for operating and budgetary accounts and fund balance accounts. Debits Credits Appropriations $ 6,224,000 Estimated Other Financing Uses 2,776,000 Estimated Revenues $ 7,997,000 Encumbrances 0 Expenditures 6,192,000 Other Financing Uses 2,770,000 Revenues 7,980,000 Budgetary Fund Balance 1,003,000 Fund Balance-Nonspendable-Inventory of Supplies 140,000 Fund Balance-Unassigned 1,990,000 Required Prepare the closing entries for the year.

Journal entries, financial statements, and closing entries for a Capital Projects Fund The following transactions occurred...

Journal entries, financial statements, and closing entries for a Capital Projects Fund The following transactions occurred during the fiscal year July 1, 2018 to June 30, 2019: 1. The City of Spainville approved the construction of a city hall complex for a total cost of $120,000,000. A few days later, a contract with a 5 percent retainage clause was signed with Paltrow Construction for the complex. The buildings will be financed by a federal expenditure driven grant of $25,000,000 and...

Journal entries, financial statements, and closing entries for a Capital Projects Fund The following transactions occurred during the fiscal year July 1, 2018 to June 30, 2019: 1. The City of Spainville approved the construction of a city hall complex for a total cost of $120,000,000. A few days later, a contract with a 5 percent retainage clause was signed with Paltrow Construction for the complex. The buildings will be financed by a federal expenditure driven grant of $25,000,000 and...

Create the balance sheet according to this trial balance The following unadjusted trial balances are for...

Create the balance sheet according to this trial balance The following unadjusted trial balances are for the governmental funds of the City of Copeland prepared from the current accounting records: General Fund Debit Credit Cash $ 19,000 Taxes Receivable 202,000 Allowance for Uncollectible Taxes $ 2,000 Vouchers Payable 24,000 Due to Debt Service Fund 10,000 Unavailable Revenues 16,000 Encumbrances Outstanding 9,000 Fund Balance—Unassigned 103,000 Revenues 176,000 Expenditures 110,000 Encumbrances 9,000 Estimated Revenues 190,000 Appropriations 171,000...

The following is a pre-closing trial balance for the Village of Lake Augusta’s general Fund as...

The following is a pre-closing trial balance for the Village of Lake Augusta’s general Fund as of December 31, 2017: Debits Credits Accounts payable 6,800 Appropriations 160,000 Budgetary fund balance 38,000 Budgetary fund balance: reserve for encumbrances 5,000 Cash 116,500 Deferred revenues: property taxes 3,000 Due to other funds 5,000 Encumbrances 5,000 Estimated other financing sources 8,000 Estimated other financing uses 10,000 Estimated revenues 200,000 Estimated uncollectible taxes 2,000 Expenditures 154,000 Fund balance 54,700 Other financing sources 10,000 Other financing...

The following is a pre-closing trial balance for the Village of Lake Augusta’s general Fund as of December 31, 2017:...

The following is a pre-closing trial balance for the Village of Lake Augusta’s general Fund as of December 31, 2017: Debits Credits Accounts payable 6,800 Appropriations 160,000 Budgetary fund balance 38,000 Budgetary fund balance: reserve for encumbrances 5,000 Cash 116,500 Deferred revenues: property taxes 3,000 Due to other funds 5,000 Encumbrances 5,000 Estimated other financing sources 8,000 Estimated other financing uses 10,000 Estimated revenues 200,000 Estimated uncollectible taxes 2,000 Expenditures 154,000 Fund balance 54,700 Other financing sources 10,000 Other financing...

The City of Morganville had the following pre-closing account balances in its General Fund as of April 30, 2017. Debits...

The City of Morganville had the following pre-closing account balances in its General Fund as of April 30, 2017. Debits and credits are not separated; each account had its “normal” balance. Among the expenditures recorded this year is an amount expended on supplies ordered at the end of the previous year. Assume that encumbrances do not lapse and that the City failed to make the journal entry(s) necessary to re-establish the encumbrance in the current year. Required: Prepare all...

· The City of Troutman had the following partial list of pre-closing account balances in its General Fund as of June 30, 2019. Debits Credits $3,675,000 385,000 111,000 60,000 107,000 290,000 Appropriations Control Budgetary Fund Balance Budgetary Fund Balance - Reserve for Encumbrances Due to Other Funds Encumbrances Control Estimated Other Financing Uses Control Estimated Revenues Control Expenditures Control Fund Balance Other Financing Uses Control-Transfers Out Revenues Control Taxes Receivable-Delinquent Vouchers Payable 3,860,000 3,405,000 272,000 315,000 3,968,000 85,000 275,000 Required:...

· The City of Troutman had the following partial list of pre-closing account balances in its General Fund as of June 30, 2019. Debits Credits $3,675,000 385,000 111,000 60,000 107,000 290,000 Appropriations Control Budgetary Fund Balance Budgetary Fund Balance - Reserve for Encumbrances Due to Other Funds Encumbrances Control Estimated Other Financing Uses Control Estimated Revenues Control Expenditures Control Fund Balance Other Financing Uses Control-Transfers Out Revenues Control Taxes Receivable-Delinquent Vouchers Payable 3,860,000 3,405,000 272,000 315,000 3,968,000 85,000 275,000 Required:...

The year-end pre-closing trial balance for the Chance County Woodland Park Capital Projects Fund is provided below. Cash Grant Receivables Investments Contract Payable Contract Payable - Retained Percentage Encumbrances Outstanding Revenues Encumbrances Construction Expenditures Other Financing Sources - Proceeds of Bonds Debits Credits $ 987,000 600,000 1,800,000 $1,263, 588 66,500 1,625,000 707,600 1,625,000 4,150,000 4,700,890 $8,362,eee $8,362, eee Required a. Prepare the year-end statement of revenues, expenditures, and changes in fund balances for the capital projects fund, CHANCE COUNTY Woodland...

The year-end pre-closing trial balance for the Chance County Woodland Park Capital Projects Fund is provided below. Cash Grant Receivables Investments Contract Payable Contract Payable - Retained Percentage Encumbrances Outstanding Revenues Encumbrances Construction Expenditures Other Financing Sources - Proceeds of Bonds Debits Credits $ 987,000 600,000 1,800,000 $1,263, 588 66,500 1,625,000 707,600 1,625,000 4,150,000 4,700,890 $8,362,eee $8,362, eee Required a. Prepare the year-end statement of revenues, expenditures, and changes in fund balances for the capital projects fund, CHANCE COUNTY Woodland...

Record in general journal form entries to close the budgetary and operating statement accounts in the General Fund only. Do not close the governmental activities accounts. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations.) Debit Credit Transactions Fund General Journal 1. Record the closure of budgetary statements account General Fund Appropriations Estimated Revenues Budgetary Fund Balance 3,119,000 2. Record the closure of operating statements account....

Record in general journal form entries to close the budgetary and operating statement accounts in the General Fund only. Do not close the governmental activities accounts. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations.) Debit Credit Transactions Fund General Journal 1. Record the closure of budgetary statements account General Fund Appropriations Estimated Revenues Budgetary Fund Balance 3,119,000 2. Record the closure of operating statements account....

Journal entries, financial statements, and closing entries for a Capital Projects Fund The following transactions occurred during the fiscal year July 1, 2018 to June 30, 2019: 1. The City of Spainville approved the construction of a city hall complex for a total cost of $120,000,000. A few days later, a contract with a 5 percent retainage clause was signed with Paltrow Construction for the complex. The buildings will be financed by a federal expenditure driven grant of $25,000,000 and...

Journal entries, financial statements, and closing entries for a Capital Projects Fund The following transactions occurred during the fiscal year July 1, 2018 to June 30, 2019: 1. The City of Spainville approved the construction of a city hall complex for a total cost of $120,000,000. A few days later, a contract with a 5 percent retainage clause was signed with Paltrow Construction for the complex. The buildings will be financed by a federal expenditure driven grant of $25,000,000 and...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago