Homework Answers

![to B-13 -ntem) Se (B) 95% confidence internal 5 p[rtis ** )=0.95 p[-t st[+]=0.95 p[-+ C Boli sti]=0.95 p[-t.s.e(B) < B-B 5 tu](http://img.homeworklib.com/questions/513ec690-c420-11ea-8423-7fe6d97faa8e.png?x-oss-process=image/resize,w_560)

![1 p [-t.S.e(B) { Ê - B Ś Łse.(R)] = 0.95 PHAB P[-t?sec8) + B-B Ł*se (B)]=0.95 - (multiply by al) PL Å - tt se (B) e B S Å a](http://img.homeworklib.com/questions/51d0dc20-c420-11ea-9950-fd59b48ef608.png?x-oss-process=image/resize,w_560)

Add Answer to:

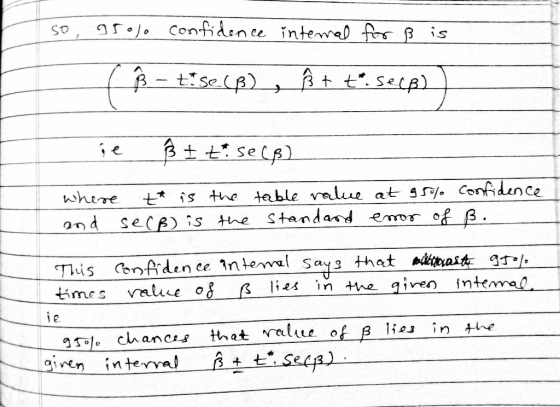

2. Suppose § is an unbiased OLS estimator of parameter B, and the t-statistic t =...

Complete the sentence: An unbiased estimator is _____. a. any sample statistic used to approximate a...

Complete the sentence: An unbiased estimator is _____. a. any sample statistic used to approximate a population parameter b. a sample statistic, which has an expected value equal to the value of the population parameter c. a sample statistic whose value is usually less than the value of the population parameter d. any estimator whose standard error is relatively small

Suppose you have an unbiased, normally distributed estimator of a parameter B, and are testing the...

Suppose you have an unbiased, normally distributed estimator of a parameter B, and are testing the null hypothesis B=0 with a two tail test. For the present sample, the standard error of the estimator is 1.0 Suppose the true value of B=0.5. Professor X conducts the study and finds a positive and significant B. If you attempt to replicate Professor X's study in other data sets of the same size, what percentage of those data sets would you expect the...

1. An estimator is unbiased if A. the expected value of the estimator is equal to...

1. An estimator is unbiased if A. the expected value of the estimator is equal to the sample statistic. B. the p-value is less than .05. C. the standard error is small. D. the expected value of the estimator is equal to the true population parameter. 2.If we find that it is unlikely to observe the sample statistic that is actually observed if the null hypothesis is true, then we should A. reject the alternative hypothesis. B. fail to reject...

A) Find the variance of each unbiased estimator. b) Use the Central Limit Theorem to create an ap...

a) Find the variance of each unbiased estimator.

b) Use the Central Limit Theorem to create an approximate 95%

confidence interval for theta.

c) Use the pivotal quantity Beta(alpha=13, beta=13) to create an

approximate 95% confidence interval for theta.

d) Use the pivotal quantity Beta(alpha=25, beta=1) to create an

approximate 95% confidence interval for theta.

Suppose that Xi, , x25 are i.i.d. Unifom(0,0), where θ is unknown. Consider three unbiased estimators of 6 25 26 25 25 26 max (X...,...

a) Find the variance of each unbiased estimator.

b) Use the Central Limit Theorem to create an approximate 95%

confidence interval for theta.

c) Use the pivotal quantity Beta(alpha=13, beta=13) to create an

approximate 95% confidence interval for theta.

d) Use the pivotal quantity Beta(alpha=25, beta=1) to create an

approximate 95% confidence interval for theta.

Suppose that Xi, , x25 are i.i.d. Unifom(0,0), where θ is unknown. Consider three unbiased estimators of 6 25 26 25 25 26 max (X...,...

7. When we impose a restriction on the OLS estimation that the intercept estimator is zero, we ca...

7. When we impose a restriction on the OLS estimation that the intercept estimator is zero, we call it regression through the origin. Consider a population model Y- Au + βίχ + u and we estimate an OLS regression model through the origin: Y-β¡XHi (note that the true intercept parameter Bo is not necessarily zero). (i) Under assumptions SLR.1-SLR.4, either use the method of moments or minimize the SSR to show that the βί-1-- ie1 (2) Find E(%) in terms...

7. When we impose a restriction on the OLS estimation that the intercept estimator is zero, we call it regression through the origin. Consider a population model Y- Au + βίχ + u and we estimate an OLS regression model through the origin: Y-β¡XHi (note that the true intercept parameter Bo is not necessarily zero). (i) Under assumptions SLR.1-SLR.4, either use the method of moments or minimize the SSR to show that the βί-1-- ie1 (2) Find E(%) in terms...

Which of the statements about large-sample estimation is correct? (1) An estimator should be unbiased and...

Which of the statements about large-sample estimation is correct? (1) An estimator should be unbiased and the spread (as measured by the mean) should be as small as possible. (2) The distance between an estimate and the true value of the statistic is called the error of estimation. (3) The 95% Margin of error is: 1.96 Standard error of the estimator. (4) A good confidence interval is as wide as possible.

Which of the statements about large-sample estimation is correct? (1) An estimator should be unbiased and the spread (as measured by the mean) should be as small as possible. (2) The distance between an estimate and the true value of the statistic is called the error of estimation. (3) The 95% Margin of error is: 1.96 Standard error of the estimator. (4) A good confidence interval is as wide as possible.

Which of the statements about large-sample estimation is correct? (1) An estimator should be unbiased and...

Which of the statements about large-sample estimation is correct? (1) An estimator should be unbiased and the spread (as measured by the mean) should be as small as possible. (2) The distance between an estimate and the true value of the statistic is called the error of estimation. (3) The 95% Margin of error is: 1.96 x Standard error of the estimator. (4) A good confidence interval is as wide as possible.

Which of the statements about large-sample estimation is correct? (1) An estimator should be unbiased and the spread (as measured by the mean) should be as small as possible. (2) The distance between an estimate and the true value of the statistic is called the error of estimation. (3) The 95% Margin of error is: 1.96 x Standard error of the estimator. (4) A good confidence interval is as wide as possible.

7.20 Consider Y1,...,Yn as defined in Exercise 7.19. (a) Show that Yilti is an unbiased estimator...

7.20 Consider Y1,...,Yn as defined in Exercise 7.19. (a) Show that Yilti is an unbiased estimator of B. (b) Calculate the exact variance of Yi/ xi and compare it to the variance of the MLE. 7.19 Suppose that the random variables Yı, ..., Yn satisfy Yi = Bli +ti, i = 1,...,n, where x1, ..., In are fixed constants, and €1,..., En are iid n(0,02), o2 unknown. (a) Find a two-dimensional sufficient statistic for (0,0%). (b) Find the MLE of...

7.20 Consider Y1,...,Yn as defined in Exercise 7.19. (a) Show that Yilti is an unbiased estimator of B. (b) Calculate the exact variance of Yi/ xi and compare it to the variance of the MLE. 7.19 Suppose that the random variables Yı, ..., Yn satisfy Yi = Bli +ti, i = 1,...,n, where x1, ..., In are fixed constants, and €1,..., En are iid n(0,02), o2 unknown. (a) Find a two-dimensional sufficient statistic for (0,0%). (b) Find the MLE of...

2. (a) Define the bias of ˆ θ as an estimator for the parameter θ. [2...

2. (a) Define the bias of ˆ θ as an estimator for the parameter θ. [2 marks] (b) For independent random variables X1,X2,...,Xn, assume that E(Xi) = µ and var(Xi) = σ2, i = 1,...,n. (i) Show that ˆ µ1 = {(X1+Xn)/2}is an unbiased estimator for µ and determine its variance. [3 marks] (ii) Find the relative efficiency of ˆ µ1 to the unbiased estimator ˆ µ2 = X, the sample mean. [2 marks] (iii) Is ˆ µ1 a consistent...

7. True/False a. If Cov(x,u)>0, then the OLS estimator βι will then to be higher than...

7. True/False a. If Cov(x,u)>0, then the OLS estimator βι will then to be higher than β b. Suppose you run a regression and obtain the estimate B1 - 3.4. Stata tells you that the test statistic for the null hypothesis that B12 is equal to 2. This implies that the standard error of the slope coefficient is also equal to 2.

7. True/False a. If Cov(x,u)>0, then the OLS estimator βι will then to be higher than β b. Suppose you run a regression and obtain the estimate B1 - 3.4. Stata tells you that the test statistic for the null hypothesis that B12 is equal to 2. This implies that the standard error of the slope coefficient is also equal to 2.

a) Find the variance of each unbiased estimator.

b) Use the Central Limit Theorem to create an approximate 95%

confidence interval for theta.

c) Use the pivotal quantity Beta(alpha=13, beta=13) to create an

approximate 95% confidence interval for theta.

d) Use the pivotal quantity Beta(alpha=25, beta=1) to create an

approximate 95% confidence interval for theta.

Suppose that Xi, , x25 are i.i.d. Unifom(0,0), where θ is unknown. Consider three unbiased estimators of 6 25 26 25 25 26 max (X...,...

a) Find the variance of each unbiased estimator.

b) Use the Central Limit Theorem to create an approximate 95%

confidence interval for theta.

c) Use the pivotal quantity Beta(alpha=13, beta=13) to create an

approximate 95% confidence interval for theta.

d) Use the pivotal quantity Beta(alpha=25, beta=1) to create an

approximate 95% confidence interval for theta.

Suppose that Xi, , x25 are i.i.d. Unifom(0,0), where θ is unknown. Consider three unbiased estimators of 6 25 26 25 25 26 max (X...,...

7. When we impose a restriction on the OLS estimation that the intercept estimator is zero, we call it regression through the origin. Consider a population model Y- Au + βίχ + u and we estimate an OLS regression model through the origin: Y-β¡XHi (note that the true intercept parameter Bo is not necessarily zero). (i) Under assumptions SLR.1-SLR.4, either use the method of moments or minimize the SSR to show that the βί-1-- ie1 (2) Find E(%) in terms...

7. When we impose a restriction on the OLS estimation that the intercept estimator is zero, we call it regression through the origin. Consider a population model Y- Au + βίχ + u and we estimate an OLS regression model through the origin: Y-β¡XHi (note that the true intercept parameter Bo is not necessarily zero). (i) Under assumptions SLR.1-SLR.4, either use the method of moments or minimize the SSR to show that the βί-1-- ie1 (2) Find E(%) in terms...

Which of the statements about large-sample estimation is correct? (1) An estimator should be unbiased and the spread (as measured by the mean) should be as small as possible. (2) The distance between an estimate and the true value of the statistic is called the error of estimation. (3) The 95% Margin of error is: 1.96 Standard error of the estimator. (4) A good confidence interval is as wide as possible.

Which of the statements about large-sample estimation is correct? (1) An estimator should be unbiased and the spread (as measured by the mean) should be as small as possible. (2) The distance between an estimate and the true value of the statistic is called the error of estimation. (3) The 95% Margin of error is: 1.96 Standard error of the estimator. (4) A good confidence interval is as wide as possible.

Which of the statements about large-sample estimation is correct? (1) An estimator should be unbiased and the spread (as measured by the mean) should be as small as possible. (2) The distance between an estimate and the true value of the statistic is called the error of estimation. (3) The 95% Margin of error is: 1.96 x Standard error of the estimator. (4) A good confidence interval is as wide as possible.

Which of the statements about large-sample estimation is correct? (1) An estimator should be unbiased and the spread (as measured by the mean) should be as small as possible. (2) The distance between an estimate and the true value of the statistic is called the error of estimation. (3) The 95% Margin of error is: 1.96 x Standard error of the estimator. (4) A good confidence interval is as wide as possible.

7.20 Consider Y1,...,Yn as defined in Exercise 7.19. (a) Show that Yilti is an unbiased estimator of B. (b) Calculate the exact variance of Yi/ xi and compare it to the variance of the MLE. 7.19 Suppose that the random variables Yı, ..., Yn satisfy Yi = Bli +ti, i = 1,...,n, where x1, ..., In are fixed constants, and €1,..., En are iid n(0,02), o2 unknown. (a) Find a two-dimensional sufficient statistic for (0,0%). (b) Find the MLE of...

7.20 Consider Y1,...,Yn as defined in Exercise 7.19. (a) Show that Yilti is an unbiased estimator of B. (b) Calculate the exact variance of Yi/ xi and compare it to the variance of the MLE. 7.19 Suppose that the random variables Yı, ..., Yn satisfy Yi = Bli +ti, i = 1,...,n, where x1, ..., In are fixed constants, and €1,..., En are iid n(0,02), o2 unknown. (a) Find a two-dimensional sufficient statistic for (0,0%). (b) Find the MLE of...

7. True/False a. If Cov(x,u)>0, then the OLS estimator βι will then to be higher than β b. Suppose you run a regression and obtain the estimate B1 - 3.4. Stata tells you that the test statistic for the null hypothesis that B12 is equal to 2. This implies that the standard error of the slope coefficient is also equal to 2.

7. True/False a. If Cov(x,u)>0, then the OLS estimator βι will then to be higher than β b. Suppose you run a regression and obtain the estimate B1 - 3.4. Stata tells you that the test statistic for the null hypothesis that B12 is equal to 2. This implies that the standard error of the slope coefficient is also equal to 2.

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago