Exercise 1. Short-Run Industry Supply Curve In a perfectly competitive market there are n firms with...

Homework Answers

Add Answer to:

Exercise 1. Short-Run Industry Supply Curve

In a perfectly competitive market there are n firms with...

For a constant cost industry in which all firms the same cost functions, their long-run average...

For a constant cost industry in which all firms the same cost functions, their long-run average cost is minimized at $10 per unit output and 20 units (i.e. q = 20). Market demand is given by QD=DP=1,500-50P. Find the long-run market supply function Find the long-run equilibrium price (P*), market quantity (Q*), firm output (q*), number of firms (n), and each firm’s profit. The short-run total cost function associated with each firm’s long-run costs is SCq=0.5q2-10q+200. Calculate the short-run average...

Consider a perfectly competitive market with many identical firms. Each firm has a long-run marginal cost...

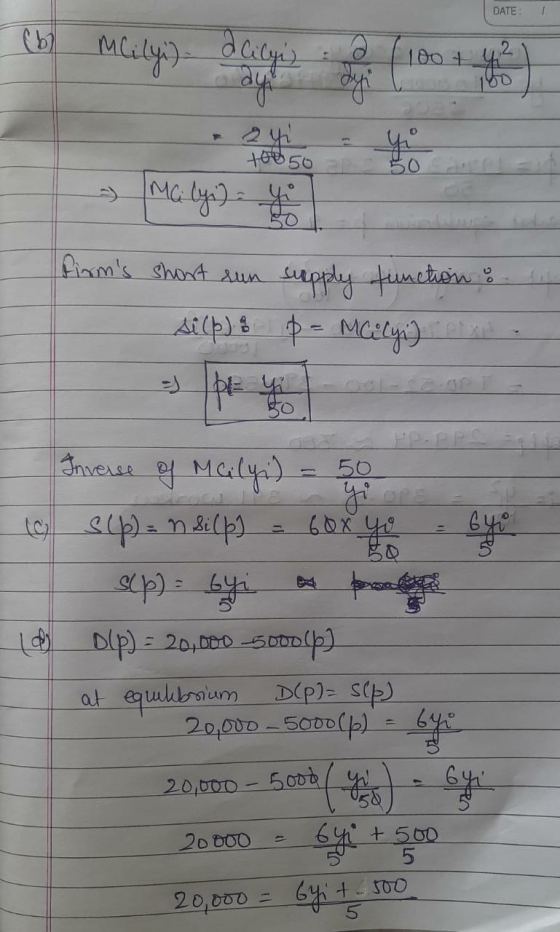

Consider a perfectly competitive market with many identical firms. Each firm has a long-run marginal cost function given by LRMC(y) = y ^2 + 1. We do not know the firms’ LRAT C function, but we know that at a quantity of 3 it is equal to LRMC. In other words: LRAT C(3) = LRMC(3). (a) Find an expression for an individual firm’s long-run inverse supply curve: this will be p as a function of y. Note that it will...

In a perfectly competitive market, a firm has the following short-run total cost function: C(q)=16+4q+q2 The...

In a perfectly competitive market, a firm has the following short-run total cost function: C(q)=16+4q+q2 The market demand is Q(p)=220-p a. Show that marginal cost curve passes through the minimum point of average cost curve. Draw a figure to show it. b. Find the firm’s individual short-run supply function. Draw it on the above figure. For the following questions, suppose that there are currently 10 identical firms in this market. c. What is the market supply curve? What are the...

Suppose the market for canola oil is perfectly competitive. There are 1,000 firms in the market,...

Suppose the market for canola oil is perfectly competitive. There are 1,000 firms in the market, each of which have a fixed cost of FC=2 and a marginal cost of MC= 1+Q, where q is quantity produced by an individual firm. Let QS denote the total quantity supplied in the market. The market demand is QD= 15,250-250P A) Find the market supply equation, that is write QS as a function of price P B)What is the equilibrium price? What is...

There are 100 firms in a perfectly competitive industry. Each firm has the short-run supply curve...

There are 100 firms in a perfectly competitive industry. Each firm has the short-run supply curve q = P−2 for P > 2, and q = 0 for P≤2. The market supply curve for this industry is Q =100P − 200 for P > 2 and Q = 0 for P ≤ 2. If the market price is $8, the firms in the industry will supply a total of 600 units. Total producer surplus is $____________________ (enter as integer)

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

The long-run supply curve for a perfectly competitive, constant-cost industry O is horizontal at minimum ATC....

The long-run supply curve for a perfectly competitive, constant-cost industry O is horizontal at minimum ATC. O is upward-sloping. O is horizontal at minimum AVC. O is found by adding up the marginal cost curves for all firms in the industry. As more firms enter the market: O the short-run market demand curve shifts to the left. O the short-run market supply curve shifts to the right. O the short-run market supply curve shifts to the left. O the short-run...

The long-run supply curve for a perfectly competitive, constant-cost industry O is horizontal at minimum ATC. O is upward-sloping. O is horizontal at minimum AVC. O is found by adding up the marginal cost curves for all firms in the industry. As more firms enter the market: O the short-run market demand curve shifts to the left. O the short-run market supply curve shifts to the right. O the short-run market supply curve shifts to the left. O the short-run...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q)...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Suppose the market for wheat is perfectly competitive. Suppose further the long-run supply curve in this...

Suppose the market for wheat is perfectly competitive. Suppose further the long-run supply curve in this market is increasing. Explain briefly if and how each of the following varies as market quantity increases: i) The number of firms ii) Input prices iii) Long-run profits Suppose firms in a monopoly competitive market produce their profit-maximizing quantity, and their average total cost equals their marginal revenue. Should firm entry or exit in the long run?

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

The long-run supply curve for a perfectly competitive, constant-cost industry O is horizontal at minimum ATC. O is upward-sloping. O is horizontal at minimum AVC. O is found by adding up the marginal cost curves for all firms in the industry. As more firms enter the market: O the short-run market demand curve shifts to the left. O the short-run market supply curve shifts to the right. O the short-run market supply curve shifts to the left. O the short-run...

The long-run supply curve for a perfectly competitive, constant-cost industry O is horizontal at minimum ATC. O is upward-sloping. O is horizontal at minimum AVC. O is found by adding up the marginal cost curves for all firms in the industry. As more firms enter the market: O the short-run market demand curve shifts to the left. O the short-run market supply curve shifts to the right. O the short-run market supply curve shifts to the left. O the short-run...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago