Homework Answers

b).According to IAS 36 impairment of assets, If the carrying amount exceeds the recoverable amount, the asset is described as impaired. The entity must reduce the carrying amount of the asset to its recoverable amount, and recognise an impairment loss.

Recoverable amount is the higher of (a) fair value less costs to sell and (b) value in use.

Fair value less costs to sell is the arm’s length sale price between knowledgeable willing parties less costs of disposal.

Here, Fair value less cost to sell =

240000-5000=235000

The value in use of an asset is the expected future cash flows that the asset in its current condition will produce, discounted to present value using an appropriate discount rate.

| Year | Amount(A) | Discounting factor @ 10%(B) | Net present Value(A*B) |

| 1 | 150000 | 0.909 | 136350 |

| 2 | 100000 | 0.826 | 82600 |

| 3 | 50000 | 0.751 | 37550 |

| Scrap sale at end of year 3 | 25000 | 0.751 | 18775 |

| Total | 275275 |

-

Therefore recoverable amount = higher of fair value less cost to sell or value in use =2,75,275

So impairment loss = carrying value - recoverable amount = 300000-275275= 24,725

Treatment :The impairment loss is recognised as an expense (unless it relates to a revalued asset where the impairment loss is treated as a revaluation decrease).

1.If treated as expense :

Impairment loss a/c Dr 24725

To fixed asset a/c 24725

2.If it is related to an asset which was revalued earlier( to the extend of revaluation surplus relating to that asset)

Revaluation surplus a/c Dr 24725

To fixed aaset a/c 24725

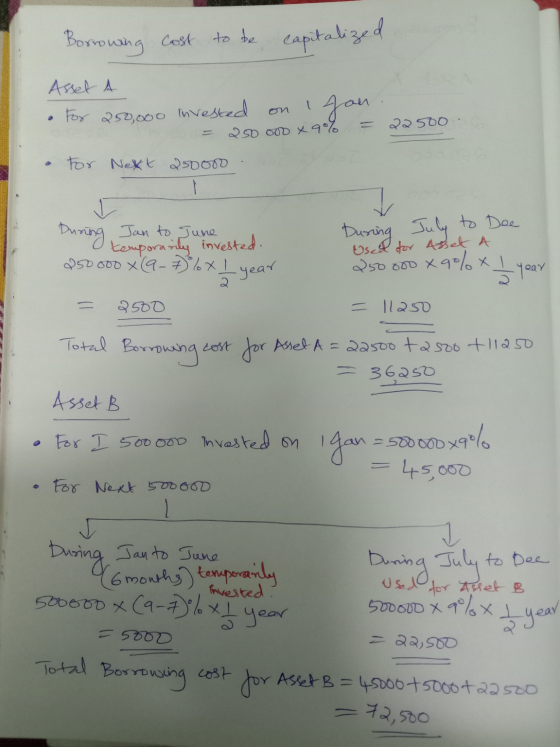

C.) According to IAS 23 - Borrowing cost,

Borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset form part of the cost of that asset and, therefore, should be capitalised. Other borrowing costs are recognised as an expense

A qualifying asset is an asset that takes a substantial period of time to get ready for its intended use or sale.Here 2 assets take 1 year to complete and hence are considered as qualifying assets.

Where funds are borrowed specifically, costs eligible for capitalisation are the actual costs incurred less any income earned on the temporary investment of such borrowings.Here loan is taken specifically to build these 2 assets and idle funds are temporarily invested during first 6 months.Hence net interest expense idle funds during first 6 months is 2%,ie, ( 9-7)%

Calculation of borrowing cost is as under

Therefore borrowing cost to be capitalized for

Asset A= 36250

Asset B = 72500

So total cost of assets on 31 Dec 2016

Asset A= 250,000+250,000+36,250=5,36,250

Asset B = 500,000+500,000+72,500=10,72,500

Add Answer to:

120 marks b) A company has a machine in its statement of financial position at a...

SECTION A (40 marks): Answer ALL Questions in this section. QUESTION ONE a) Aseda Ltd incurred...

SECTION A (40 marks): Answer ALL Questions in this section. QUESTION ONE a) Aseda Ltd incurred the following cost in its manufacturing operations GH¢ Cost of material purchase 20,000 Import duties 400 Trade discount @10% of purchase cost Cash discount 500 Irrecoverable taxes 1,000 Salary of factory plant operator 2,500 Direct labour 5,000 Salary of factory supervisor 4,000 Cost of expected production losses 800 Administrative overhead (Note) 16,000 Cost of storage of raw material for further processing 2,000 Marketing cost...

SECTION A (40 marks): Answer ALL Questions in this section. QUESTION ONE a) Aseda Ltd incurred the following cost in its manufacturing operations GH¢ Cost of material purchase 20,000 Import duties 400 Trade discount @10% of purchase cost Cash discount 500 Irrecoverable taxes 1,000 Salary of factory plant operator 2,500 Direct labour 5,000 Salary of factory supervisor 4,000 Cost of expected production losses 800 Administrative overhead (Note) 16,000 Cost of storage of raw material for further processing 2,000 Marketing cost...

26 marks Question #7 Rich Ltd was incorporated on 1 July 2015. The accounting profit and...

26 marks Question #7 Rich Ltd was incorporated on 1 July 2015. The accounting profit and other relevant information of Rich Ltd for the year to 30 June 2016 and 30 June 2017 are as follows: 2016 2017 Profit before tax $1 200 000 $1 500 000 Warranty expense 500 000 Depreciation expense- plant 20 000 20 000 Gain on sale of plant for accounting Warranty paid 250 000 Tax depreciation- plant 30 000 30 000 Gain on sale of...

26 marks Question #7 Rich Ltd was incorporated on 1 July 2015. The accounting profit and other relevant information of Rich Ltd for the year to 30 June 2016 and 30 June 2017 are as follows: 2016 2017 Profit before tax $1 200 000 $1 500 000 Warranty expense 500 000 Depreciation expense- plant 20 000 20 000 Gain on sale of plant for accounting Warranty paid 250 000 Tax depreciation- plant 30 000 30 000 Gain on sale of...

The statement of financial statement is based on the following equation: Assets = Liabilities + Equity...

The statement of financial statement is based on the following equation: Assets = Liabilities + Equity The above mentioned equation can be expanded as follows Non-current assets + current assets = non-current liabilities + current liabilities + equity Your accountant provides you with the following trial balance as at 1 March 2017 Description Balance Property, plant, equipment $350 000 Share capital $250 000 Inventory $54 000 Trade Payables $67 000 Motor vehicles -Cost $120 000 Motor vehicle – Acc Depreciation...

d. Polycarp Ltd adopts revaluation model for subsequent measurement of its intangible assets in accordance with...

d. Polycarp Ltd adopts revaluation model for subsequent measurement of its intangible assets in accordance with IAS 38: Intangible assets. The policy of Polycarp is to revalue its intangible asset at the end of each year. An intangible asset with an estimated useful life of 9 years was acquired on 1 January 2018 for GH€45,000. It was revalued to GH¢54,400 on 31 December 2018 and the revaluation surplus was correctly recognized on that date. As at 31 December 2019, the...

d. Polycarp Ltd adopts revaluation model for subsequent measurement of its intangible assets in accordance with IAS 38: Intangible assets. The policy of Polycarp is to revalue its intangible asset at the end of each year. An intangible asset with an estimated useful life of 9 years was acquired on 1 January 2018 for GH€45,000. It was revalued to GH¢54,400 on 31 December 2018 and the revaluation surplus was correctly recognized on that date. As at 31 December 2019, the...

Question 2 (8 marks) Petersen Ltd has the following land and building in its financial statements...

Question 2 (8 marks) Petersen Ltd has the following land and building in its financial statements as at 30 June 2018: 1 000 000 900 000 800 000 (100 000) Residential land, at cost actory land, at valuation 2016 Buildings, at valuation 2016 Accumulated depreciation At 30 June 2018, the balance of the revaluation surplus is $400 000, of which $300 000 relates to the factory land and $100 000 to the buildings. On this same date, independent valuations of...

Question 2 (8 marks) Petersen Ltd has the following land and building in its financial statements as at 30 June 2018: 1 000 000 900 000 800 000 (100 000) Residential land, at cost actory land, at valuation 2016 Buildings, at valuation 2016 Accumulated depreciation At 30 June 2018, the balance of the revaluation surplus is $400 000, of which $300 000 relates to the factory land and $100 000 to the buildings. On this same date, independent valuations of...

You have been appointed as a financial consultant cost of capital of the company, (25 Marks)...

You have been appointed as a financial consultant cost of capital of the company, (25 Marks) the directors of ABC Limited. They require you to calculate the The following information is available available on the capital structure of the company 1 500 000 Ordinary shares, with a market price and the return on the market is 15%. price of R3 per share. The beta of the company is 1.8, a risk-free rate of 1 000 000 12%, R1 Preference share...

You have been appointed as a financial consultant cost of capital of the company, (25 Marks) the directors of ABC Limited. They require you to calculate the The following information is available available on the capital structure of the company 1 500 000 Ordinary shares, with a market price and the return on the market is 15%. price of R3 per share. The beta of the company is 1.8, a risk-free rate of 1 000 000 12%, R1 Preference share...

On 30 June 2020, the statement of financial position of Wolfe Ltd showed the following non-...

On 30 June 2020, the statement of financial position of Wolfe Ltd showed the following non- current assets after charging depreciation: Land $400,000 Buildings $200,000 Accum. depn. - buildings (100,000) $100,000 Equipment $150,000 Accum. depn. - equipment (50.000) $100,000 Goodwill $40,000 The company has adopted fair value for the valuation of non-current assets. In the previous year, the company had valued land down from its original value of $410,000 to $400,000. On 30 June 2020, and independent valuer assessed the...

On 30 June 2020, the statement of financial position of Wolfe Ltd showed the following non- current assets after charging depreciation: Land $400,000 Buildings $200,000 Accum. depn. - buildings (100,000) $100,000 Equipment $150,000 Accum. depn. - equipment (50.000) $100,000 Goodwill $40,000 The company has adopted fair value for the valuation of non-current assets. In the previous year, the company had valued land down from its original value of $410,000 to $400,000. On 30 June 2020, and independent valuer assessed the...

(25 Marks) Adjustments and Additional Information QUESTION 6 FINANCIAL STATEMENT AND DISPOSAL OF ASSET A. Rent...

(25 Marks) Adjustments and Additional Information QUESTION 6 FINANCIAL STATEMENT AND DISPOSAL OF ASSET A. Rent for March 2017 has been received in advance. 6.1 STATEMENT OF COMPREHENSIVE INCOME (20 marks) Use the following information extracted from the accounting records of IBHUBESI TRADING to prepare the Statement of Comprehensive Income for the year ended 28 February 2017. B. Write off a debtor's outstanding account of R430 as irrecoverable. C. Adjust the provision for bad debts to 5% of trade debtors....

(25 Marks) Adjustments and Additional Information QUESTION 6 FINANCIAL STATEMENT AND DISPOSAL OF ASSET A. Rent for March 2017 has been received in advance. 6.1 STATEMENT OF COMPREHENSIVE INCOME (20 marks) Use the following information extracted from the accounting records of IBHUBESI TRADING to prepare the Statement of Comprehensive Income for the year ended 28 February 2017. B. Write off a debtor's outstanding account of R430 as irrecoverable. C. Adjust the provision for bad debts to 5% of trade debtors....

Consolidated financial statements, rationale for &n

Consolidated financial statements, rationale for adjustments Lead beaters Ltd acquired all the issued shares (cum div.) of Possum Ltd on 1 July 2014. At this date the shareholders’ equity of Possum Ltd was: Share capital – 100 000 shares General reserve Asset revaluation surplus Retained earnings $ 450 000 45 000 45 000 15 000 At 1 July 2014, the accounting records of Possum Ltd contained a dividend payable of $15 000. This dividend was paid in...

930 The directors of Silberman Ltd are considering a proposal for a new machine that is...

930 The directors of Silberman Ltd are considering a proposal for a new machine that is estimated to cost £2,500,000. This would enable the company to manufacture a superior, additional new product, product Z. The accountant has prepared the following profit forecast on the assumption that the funds will be borrowed and the loan repaid at the end of the project: Profit forecast Year 1 Year 2 Year 3 Year 4 £000 £000 £000 £000 Sales 3.125 3.750 5,000 6.250...

930 The directors of Silberman Ltd are considering a proposal for a new machine that is estimated to cost £2,500,000. This would enable the company to manufacture a superior, additional new product, product Z. The accountant has prepared the following profit forecast on the assumption that the funds will be borrowed and the loan repaid at the end of the project: Profit forecast Year 1 Year 2 Year 3 Year 4 £000 £000 £000 £000 Sales 3.125 3.750 5,000 6.250...

SECTION A (40 marks): Answer ALL Questions in this section. QUESTION ONE a) Aseda Ltd incurred the following cost in its manufacturing operations GH¢ Cost of material purchase 20,000 Import duties 400 Trade discount @10% of purchase cost Cash discount 500 Irrecoverable taxes 1,000 Salary of factory plant operator 2,500 Direct labour 5,000 Salary of factory supervisor 4,000 Cost of expected production losses 800 Administrative overhead (Note) 16,000 Cost of storage of raw material for further processing 2,000 Marketing cost...

SECTION A (40 marks): Answer ALL Questions in this section. QUESTION ONE a) Aseda Ltd incurred the following cost in its manufacturing operations GH¢ Cost of material purchase 20,000 Import duties 400 Trade discount @10% of purchase cost Cash discount 500 Irrecoverable taxes 1,000 Salary of factory plant operator 2,500 Direct labour 5,000 Salary of factory supervisor 4,000 Cost of expected production losses 800 Administrative overhead (Note) 16,000 Cost of storage of raw material for further processing 2,000 Marketing cost...

26 marks Question #7 Rich Ltd was incorporated on 1 July 2015. The accounting profit and other relevant information of Rich Ltd for the year to 30 June 2016 and 30 June 2017 are as follows: 2016 2017 Profit before tax $1 200 000 $1 500 000 Warranty expense 500 000 Depreciation expense- plant 20 000 20 000 Gain on sale of plant for accounting Warranty paid 250 000 Tax depreciation- plant 30 000 30 000 Gain on sale of...

26 marks Question #7 Rich Ltd was incorporated on 1 July 2015. The accounting profit and other relevant information of Rich Ltd for the year to 30 June 2016 and 30 June 2017 are as follows: 2016 2017 Profit before tax $1 200 000 $1 500 000 Warranty expense 500 000 Depreciation expense- plant 20 000 20 000 Gain on sale of plant for accounting Warranty paid 250 000 Tax depreciation- plant 30 000 30 000 Gain on sale of...

d. Polycarp Ltd adopts revaluation model for subsequent measurement of its intangible assets in accordance with IAS 38: Intangible assets. The policy of Polycarp is to revalue its intangible asset at the end of each year. An intangible asset with an estimated useful life of 9 years was acquired on 1 January 2018 for GH€45,000. It was revalued to GH¢54,400 on 31 December 2018 and the revaluation surplus was correctly recognized on that date. As at 31 December 2019, the...

d. Polycarp Ltd adopts revaluation model for subsequent measurement of its intangible assets in accordance with IAS 38: Intangible assets. The policy of Polycarp is to revalue its intangible asset at the end of each year. An intangible asset with an estimated useful life of 9 years was acquired on 1 January 2018 for GH€45,000. It was revalued to GH¢54,400 on 31 December 2018 and the revaluation surplus was correctly recognized on that date. As at 31 December 2019, the...

Question 2 (8 marks) Petersen Ltd has the following land and building in its financial statements as at 30 June 2018: 1 000 000 900 000 800 000 (100 000) Residential land, at cost actory land, at valuation 2016 Buildings, at valuation 2016 Accumulated depreciation At 30 June 2018, the balance of the revaluation surplus is $400 000, of which $300 000 relates to the factory land and $100 000 to the buildings. On this same date, independent valuations of...

Question 2 (8 marks) Petersen Ltd has the following land and building in its financial statements as at 30 June 2018: 1 000 000 900 000 800 000 (100 000) Residential land, at cost actory land, at valuation 2016 Buildings, at valuation 2016 Accumulated depreciation At 30 June 2018, the balance of the revaluation surplus is $400 000, of which $300 000 relates to the factory land and $100 000 to the buildings. On this same date, independent valuations of...

You have been appointed as a financial consultant cost of capital of the company, (25 Marks) the directors of ABC Limited. They require you to calculate the The following information is available available on the capital structure of the company 1 500 000 Ordinary shares, with a market price and the return on the market is 15%. price of R3 per share. The beta of the company is 1.8, a risk-free rate of 1 000 000 12%, R1 Preference share...

You have been appointed as a financial consultant cost of capital of the company, (25 Marks) the directors of ABC Limited. They require you to calculate the The following information is available available on the capital structure of the company 1 500 000 Ordinary shares, with a market price and the return on the market is 15%. price of R3 per share. The beta of the company is 1.8, a risk-free rate of 1 000 000 12%, R1 Preference share...

On 30 June 2020, the statement of financial position of Wolfe Ltd showed the following non- current assets after charging depreciation: Land $400,000 Buildings $200,000 Accum. depn. - buildings (100,000) $100,000 Equipment $150,000 Accum. depn. - equipment (50.000) $100,000 Goodwill $40,000 The company has adopted fair value for the valuation of non-current assets. In the previous year, the company had valued land down from its original value of $410,000 to $400,000. On 30 June 2020, and independent valuer assessed the...

On 30 June 2020, the statement of financial position of Wolfe Ltd showed the following non- current assets after charging depreciation: Land $400,000 Buildings $200,000 Accum. depn. - buildings (100,000) $100,000 Equipment $150,000 Accum. depn. - equipment (50.000) $100,000 Goodwill $40,000 The company has adopted fair value for the valuation of non-current assets. In the previous year, the company had valued land down from its original value of $410,000 to $400,000. On 30 June 2020, and independent valuer assessed the...

(25 Marks) Adjustments and Additional Information QUESTION 6 FINANCIAL STATEMENT AND DISPOSAL OF ASSET A. Rent for March 2017 has been received in advance. 6.1 STATEMENT OF COMPREHENSIVE INCOME (20 marks) Use the following information extracted from the accounting records of IBHUBESI TRADING to prepare the Statement of Comprehensive Income for the year ended 28 February 2017. B. Write off a debtor's outstanding account of R430 as irrecoverable. C. Adjust the provision for bad debts to 5% of trade debtors....

(25 Marks) Adjustments and Additional Information QUESTION 6 FINANCIAL STATEMENT AND DISPOSAL OF ASSET A. Rent for March 2017 has been received in advance. 6.1 STATEMENT OF COMPREHENSIVE INCOME (20 marks) Use the following information extracted from the accounting records of IBHUBESI TRADING to prepare the Statement of Comprehensive Income for the year ended 28 February 2017. B. Write off a debtor's outstanding account of R430 as irrecoverable. C. Adjust the provision for bad debts to 5% of trade debtors....

930 The directors of Silberman Ltd are considering a proposal for a new machine that is estimated to cost £2,500,000. This would enable the company to manufacture a superior, additional new product, product Z. The accountant has prepared the following profit forecast on the assumption that the funds will be borrowed and the loan repaid at the end of the project: Profit forecast Year 1 Year 2 Year 3 Year 4 £000 £000 £000 £000 Sales 3.125 3.750 5,000 6.250...

930 The directors of Silberman Ltd are considering a proposal for a new machine that is estimated to cost £2,500,000. This would enable the company to manufacture a superior, additional new product, product Z. The accountant has prepared the following profit forecast on the assumption that the funds will be borrowed and the loan repaid at the end of the project: Profit forecast Year 1 Year 2 Year 3 Year 4 £000 £000 £000 £000 Sales 3.125 3.750 5,000 6.250...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago