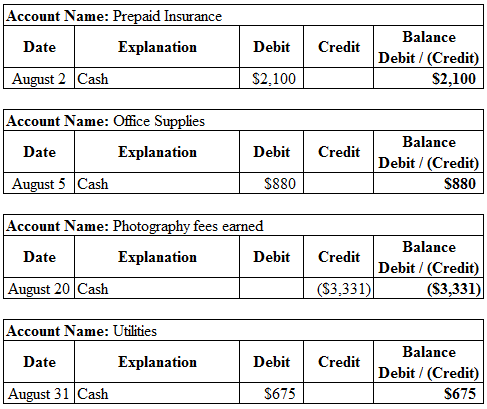

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the...

Following are the transactions of a new company called Pose-for-Pics.

Aug. 1

Madison Harris, the owner, invested $6,500 cash and $33,500 of

photography equipment in the company in exchange for common

stock.

2 The company paid $2,100 cash for an

insurance policy covering the next 24 months.

5 The company purchased office supplies for $880

cash.

20 The company received $3,331 cash in

photography fees earned.

31 The company paid $675 cash for August

utilities.

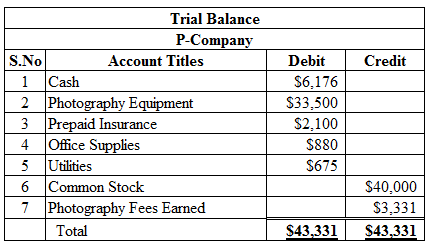

Prepare an August 31 trial balance for Pose-for-Pics.

Debit Credit

Cash

Offices

Prepaid insurance

Photography equipment

Common stock

Photography fees earned

Utilities expense

Totals

Dont have to caculate totals. Thank you!

Homework Answers

Journal entry: Journal is the book of original entry whereby all the financial transactions are recorded date-wise with the debit and credit entry to the respective accounts in transaction. Journal entry is the primary books of accounts for any entity to record the daily transactions and processed further till the presentation of the financial statements.

Accrual accounting: Accrual accounting refers to the accounting system, where revenues and expenditures are recorded when goods and services are sold or when the expenses are incurred, irrespective of the payment received or paid.

Accrued revenue: According to accrual, method of accounting, all accrued revenues must be recognized and recorded as the revenue of the accounting period, even if cash is not received in respect of those revenues.

Accrued expenses: Accrued expenses refer to the expense that is incurred during a particular period but has not been paid.

Accounting Equation: This is a mathematical equation which represents the association between assets, liabilities and stockholders’ equity. This is also called as balance sheet equation. It is represented as follows:

Asset (A): The source which is possessed or controlled to generate income in the future is known as an asset. Examples: Cash, prepaid expense, Machinery, Goodwill, and Supplies. (A+) indicates increase in asset and (A–) indicates decrease in asset.

Liability (L): Liability is an agreement made by the company to pay a certain amount for the goods or services received by the company in the past. Examples: Accounts Payable, Loans and Advances, and Outstanding Expenses. (L+) indicates increase in liability and (L–) indicates decrease in liability.

Stockholders’ equity (E): Stockholders’ equity refers to the shareholders claims on the assets or resources of a company, and so known also as net assets of the company, which are assets minus liabilities. Examples: Retained Earnings, Dividends, and Capital. . (E+) indicates increase in equity and (E–) indicates decrease in equity.

Revenue: Revenue is the total income earned by an organization by selling goods or rendering services.

Expense: Expense is the cost borne by a company to produce and sell the goods and services to the customers.

Rules of debit and credit: The category of accounts determines how the increases and decreases are recorded in the said account. In other words, the account category determines the rule of debit and credit for that particular account. The following are the rules of debit and credit:

Debit increases all asset accounts. Debit decreases all liabilities and stockholders’ equity account.

Credit increases all liabilities and stockholders’ equity account. Credit decreases all asset accounts.

T-Accounts: This is a format of account with two columns indicating a debit entry on the left and credit entry on the right.

The following is the accounting equation for the journal entry:

Journalise the transaction as follows:

The following is the accounting equation for the journal entry:

Journalise the transaction as follows:

The following is the accounting equation for the journal entry:

Journalise the transaction as follows:

The following is the accounting equation for the journal entry:

Journalise the transaction as follows:

The following is the accounting equation for the journal entry:

Journalise the transaction as follows:

The T-accounts can be prepared as follows:

The Trial balance of P Company is prepared as follows:

Add Answer to:

Following are the transactions of a new company called

Pose-for-Pics.

Aug. 1

Madison Harris, the...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner,...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $6,500 cash and $33,500 of photography equipment in the company in exchange for common stock. 2 The company paid $2,100 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $880 cash. 20 The company received $3,331 cash in photography fees earned. 31 The company paid $675 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $6,500 cash and $33,500 of photography equipment in the company in exchange for common stock. 2 The company paid $2,100 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $880 cash. 20 The company received $3,331 cash in photography fees earned. 31 The company paid $675 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner,...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $7,100 cash and $34,100 of photography equipment in the company in exchange for common stock. 2 The company paid $2,700 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $940 cash. 20 The company received $3,931 cash in photography fees earned. 31 The company paid $735 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $7,100 cash and $34,100 of photography equipment in the company in exchange for common stock. 2 The company paid $2,700 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $940 cash. 20 The company received $3,931 cash in photography fees earned. 31 The company paid $735 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner,...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $7,900 cash and $34,900 of photography equipment in the company in exchange for common stock. 2 The company paid $3,500 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,020 cash. 20 The company received $4,731 cash in photography fees earned. 31 The company paid $815 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $7,900 cash and $34,900 of photography equipment in the company in exchange for common stock. 2 The company paid $3,500 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,020 cash. 20 The company received $4,731 cash in photography fees earned. 31 The company paid $815 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner,...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $8,400 cash and $35,400 of photography equipment in the company in exchange for common stock. 2 The company paid $4,000 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,070 cash. 20 The company received $5,231 cash in photography fees earned. 31 The company paid $865 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $8,400 cash and $35,400 of photography equipment in the company in exchange for common stock. 2 The company paid $4,000 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,070 cash. 20 The company received $5,231 cash in photography fees earned. 31 The company paid $865 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner,...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $8,100 cash and $35,100 of photography equipment in the company. 2 The company paid $3,700 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,040 cash. 20 The company received $4,931 cash in photography fees earned. 31 The company paid $835 cash for August utilities. Required: 1. Post the transactions to the T-accounts. 2. Use...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $8,100 cash and $35,100 of photography equipment in the company. 2 The company paid $3,700 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,040 cash. 20 The company received $4,931 cash in photography fees earned. 31 The company paid $835 cash for August utilities. Required: 1. Post the transactions to the T-accounts. 2. Use...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner,...

Following are the transactions of a new company called

Pose-for-Pics.

Aug.

1

Madison Harris, the owner, invested $8,250 cash and $35,475 of

photography equipment in the company in exchange for common

stock.

2

The company paid $3,200 cash for an insurance policy covering

the next 24 months.

5

The company purchased office supplies for $1,568 cash.

20

The company received $3,300 cash in photography fees earned.

31

The company paid $870 cash for August utilities.

Prepare general journal entries for...

Following are the transactions of a new company called

Pose-for-Pics.

Aug.

1

Madison Harris, the owner, invested $8,250 cash and $35,475 of

photography equipment in the company in exchange for common

stock.

2

The company paid $3,200 cash for an insurance policy covering

the next 24 months.

5

The company purchased office supplies for $1,568 cash.

20

The company received $3,300 cash in photography fees earned.

31

The company paid $870 cash for August utilities.

Prepare general journal entries for...

Following are the transactions of a new company called Pose-for-Pics. Aug 1 Madison Harris, the owner,...

Following are the transactions of a new company called Pose-for-Pics. Aug 1 Madison Harris, the owner, invested $7,300 cash and $34,300 of photography equipment in the company in exchange for common stock. 2 The company paid $2,900 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $960 cash. 20 The company received $4,131 cash in photography fees earned. 31 The company paid $755 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug 1 Madison Harris, the owner, invested $7,300 cash and $34,300 of photography equipment in the company in exchange for common stock. 2 The company paid $2,900 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $960 cash. 20 The company received $4,131 cash in photography fees earned. 31 The company paid $755 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1Madison Harris, the owner, invested...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1Madison Harris, the owner, invested $6,500 cash and $33,s00 of photography equipment in the company. 2 The company paid $2,100 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $880 cash 20 The company received $3,331 cash in photography fees earned. 31 The company paid $675 cash for August utilities. Required: 1. Post the transactions to the T-accounts. 2. Use the...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1Madison Harris, the owner, invested $6,500 cash and $33,s00 of photography equipment in the company. 2 The company paid $2,100 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $880 cash 20 The company received $3,331 cash in photography fees earned. 31 The company paid $675 cash for August utilities. Required: 1. Post the transactions to the T-accounts. 2. Use the...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner,...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $9,750 cash and $41,925 of photography equipment in the company in exchange for common stock. 2 The company paid $2,300 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,853 cash. 20 The company received $2,150 cash in photography fees earned. 31 The company paid $878 cash for August utilities. Prepare general journal entries for...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $9,750 cash and $41,925 of photography equipment in the company in exchange for common stock. 2 The company paid $2,300 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,853 cash. 20 The company received $2,150 cash in photography fees earned. 31 The company paid $878 cash for August utilities. Prepare general journal entries for...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner,...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $13,500 cash and $58,050 of photography equipment in the company. 2 The company paid $2,500 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $2,565 cash. 20 The company received $2,300 cash in photography fees earned. 31 The company paid $867 cash for August utilities. Prepare general journal entries for the above transactions. View transaction...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $13,500 cash and $58,050 of photography equipment in the company. 2 The company paid $2,500 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $2,565 cash. 20 The company received $2,300 cash in photography fees earned. 31 The company paid $867 cash for August utilities. Prepare general journal entries for the above transactions. View transaction...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $6,500 cash and $33,500 of photography equipment in the company in exchange for common stock. 2 The company paid $2,100 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $880 cash. 20 The company received $3,331 cash in photography fees earned. 31 The company paid $675 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $6,500 cash and $33,500 of photography equipment in the company in exchange for common stock. 2 The company paid $2,100 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $880 cash. 20 The company received $3,331 cash in photography fees earned. 31 The company paid $675 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $7,100 cash and $34,100 of photography equipment in the company in exchange for common stock. 2 The company paid $2,700 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $940 cash. 20 The company received $3,931 cash in photography fees earned. 31 The company paid $735 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $7,100 cash and $34,100 of photography equipment in the company in exchange for common stock. 2 The company paid $2,700 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $940 cash. 20 The company received $3,931 cash in photography fees earned. 31 The company paid $735 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $7,900 cash and $34,900 of photography equipment in the company in exchange for common stock. 2 The company paid $3,500 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,020 cash. 20 The company received $4,731 cash in photography fees earned. 31 The company paid $815 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $7,900 cash and $34,900 of photography equipment in the company in exchange for common stock. 2 The company paid $3,500 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,020 cash. 20 The company received $4,731 cash in photography fees earned. 31 The company paid $815 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $8,400 cash and $35,400 of photography equipment in the company in exchange for common stock. 2 The company paid $4,000 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,070 cash. 20 The company received $5,231 cash in photography fees earned. 31 The company paid $865 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $8,400 cash and $35,400 of photography equipment in the company in exchange for common stock. 2 The company paid $4,000 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,070 cash. 20 The company received $5,231 cash in photography fees earned. 31 The company paid $865 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $8,100 cash and $35,100 of photography equipment in the company. 2 The company paid $3,700 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,040 cash. 20 The company received $4,931 cash in photography fees earned. 31 The company paid $835 cash for August utilities. Required: 1. Post the transactions to the T-accounts. 2. Use...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $8,100 cash and $35,100 of photography equipment in the company. 2 The company paid $3,700 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,040 cash. 20 The company received $4,931 cash in photography fees earned. 31 The company paid $835 cash for August utilities. Required: 1. Post the transactions to the T-accounts. 2. Use...

Following are the transactions of a new company called

Pose-for-Pics.

Aug.

1

Madison Harris, the owner, invested $8,250 cash and $35,475 of

photography equipment in the company in exchange for common

stock.

2

The company paid $3,200 cash for an insurance policy covering

the next 24 months.

5

The company purchased office supplies for $1,568 cash.

20

The company received $3,300 cash in photography fees earned.

31

The company paid $870 cash for August utilities.

Prepare general journal entries for...

Following are the transactions of a new company called

Pose-for-Pics.

Aug.

1

Madison Harris, the owner, invested $8,250 cash and $35,475 of

photography equipment in the company in exchange for common

stock.

2

The company paid $3,200 cash for an insurance policy covering

the next 24 months.

5

The company purchased office supplies for $1,568 cash.

20

The company received $3,300 cash in photography fees earned.

31

The company paid $870 cash for August utilities.

Prepare general journal entries for...

Following are the transactions of a new company called Pose-for-Pics. Aug 1 Madison Harris, the owner, invested $7,300 cash and $34,300 of photography equipment in the company in exchange for common stock. 2 The company paid $2,900 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $960 cash. 20 The company received $4,131 cash in photography fees earned. 31 The company paid $755 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug 1 Madison Harris, the owner, invested $7,300 cash and $34,300 of photography equipment in the company in exchange for common stock. 2 The company paid $2,900 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $960 cash. 20 The company received $4,131 cash in photography fees earned. 31 The company paid $755 cash for August utilities. Required: 1. Post the transactions...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1Madison Harris, the owner, invested $6,500 cash and $33,s00 of photography equipment in the company. 2 The company paid $2,100 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $880 cash 20 The company received $3,331 cash in photography fees earned. 31 The company paid $675 cash for August utilities. Required: 1. Post the transactions to the T-accounts. 2. Use the...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1Madison Harris, the owner, invested $6,500 cash and $33,s00 of photography equipment in the company. 2 The company paid $2,100 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $880 cash 20 The company received $3,331 cash in photography fees earned. 31 The company paid $675 cash for August utilities. Required: 1. Post the transactions to the T-accounts. 2. Use the...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $9,750 cash and $41,925 of photography equipment in the company in exchange for common stock. 2 The company paid $2,300 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,853 cash. 20 The company received $2,150 cash in photography fees earned. 31 The company paid $878 cash for August utilities. Prepare general journal entries for...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $9,750 cash and $41,925 of photography equipment in the company in exchange for common stock. 2 The company paid $2,300 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $1,853 cash. 20 The company received $2,150 cash in photography fees earned. 31 The company paid $878 cash for August utilities. Prepare general journal entries for...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $13,500 cash and $58,050 of photography equipment in the company. 2 The company paid $2,500 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $2,565 cash. 20 The company received $2,300 cash in photography fees earned. 31 The company paid $867 cash for August utilities. Prepare general journal entries for the above transactions. View transaction...

Following are the transactions of a new company called Pose-for-Pics. Aug. 1 Madison Harris, the owner, invested $13,500 cash and $58,050 of photography equipment in the company. 2 The company paid $2,500 cash for an insurance policy covering the next 24 months. 5 The company purchased office supplies for $2,565 cash. 20 The company received $2,300 cash in photography fees earned. 31 The company paid $867 cash for August utilities. Prepare general journal entries for the above transactions. View transaction...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago