Homework Answers

Add Answer to:

Question 16 9 pts Suppose that today's annual market interest rates are 2% for a 2-year...

16 Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for...

16 Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

16 Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

Please solve and show work fully for a rating. Thank you. Suppose that today's annual market...

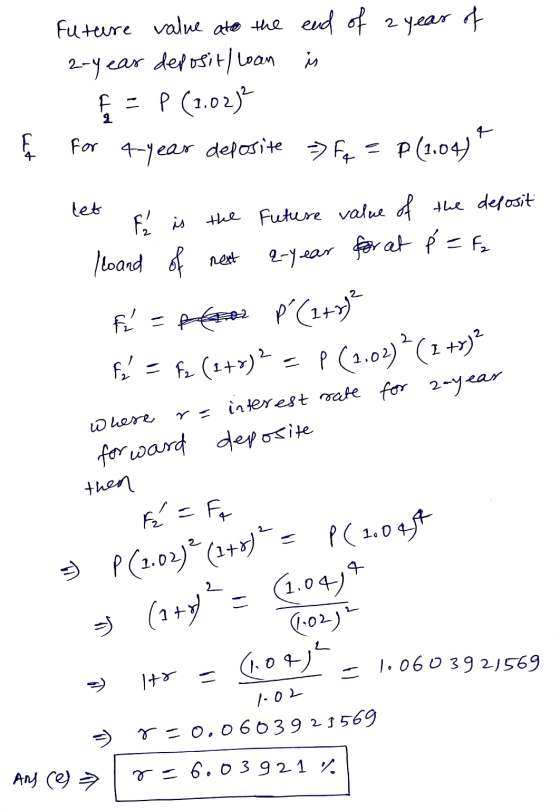

Please solve and show work fully for a rating. Thank you.

Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

Please solve and show work fully for a rating. Thank you.

Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

Suppose that today’s annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a...

Suppose that today’s annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year’s time. (Use six decimals for your computations) A) 3.50000% B) 2.00000% C) 6.03921% D) 7.06127% E) 6.5390%

All interest and inflation rates are stated as annual rates. Unbiased forward rate (forward expectation parity)...

All interest and inflation rates are stated as annual rates. Unbiased forward rate (forward expectation parity) 1. If the spot market exchange rate for the euro is 1.1427 and the 6-month forward quote is 178, what is the expected exchange rate for the euro in six months? 2. If the spot market exchange rate for the Hong Kong dollar is 7.8461 and the 1-year forward quote is -616, what is the expected exchange rate for the Hong Kong dollar in...

Can i get it solved step by step please (not on excel if applicable 15. Suppose today's 10-year rate is 9 percent. Today's 4-year rate is 7 percent. Estimate the 6-year forward rate in fou...

Can i get it solved step by step

please (not on excel if applicable

15. Suppose today's 10-year rate is 9 percent. Today's 4-year rate is 7 percent. Estimate the 6-year forward rate in four years if the 10-year rate has a .3 percent liquidity premium 5 points)

15. Suppose today's 10-year rate is 9 percent. Today's 4-year rate is 7 percent. Estimate the 6-year forward rate in four years if the 10-year rate has a .3 percent liquidity premium...

Can i get it solved step by step

please (not on excel if applicable

15. Suppose today's 10-year rate is 9 percent. Today's 4-year rate is 7 percent. Estimate the 6-year forward rate in four years if the 10-year rate has a .3 percent liquidity premium 5 points)

15. Suppose today's 10-year rate is 9 percent. Today's 4-year rate is 7 percent. Estimate the 6-year forward rate in four years if the 10-year rate has a .3 percent liquidity premium...

BF2207 Question 2 Suppose that, six months ago, you sold a call option on 1,000,000 euros...

BF2207 Question 2 Suppose that, six months ago, you sold a call option on 1,000,000 euros (EUR) with an expiration date of six months and an exercise price of 1.1780 United States dollars (USD). You received a premium on the call option of 0.045 USD per unit. Assume the following: • Money market interest rates for EUR are constant through time and equal 5% for all maturities. • Money market interest rates for USD are constant through time and equal...

BF2207 Question 2 Suppose that, six months ago, you sold a call option on 1,000,000 euros (EUR) with an expiration date of six months and an exercise price of 1.1780 United States dollars (USD). You received a premium on the call option of 0.045 USD per unit. Assume the following: • Money market interest rates for EUR are constant through time and equal 5% for all maturities. • Money market interest rates for USD are constant through time and equal...

Question 27 1 pts A 12-year bond has an annual coupon of 9%. The coupon rate...

Question 27 1 pts A 12-year bond has an annual coupon of 9%. The coupon rate will remain fixed until the bond matures. The bond has a yield to maturity of 7%. Which of the following statements is CORRECT? O If market interest rates decline, the price of the bond will O The bond is currently selling at a price below its par O If market interest rates remain unchanged, the bond's also decline. value. price one year from now...

Question 27 1 pts A 12-year bond has an annual coupon of 9%. The coupon rate will remain fixed until the bond matures. The bond has a yield to maturity of 7%. Which of the following statements is CORRECT? O If market interest rates decline, the price of the bond will O The bond is currently selling at a price below its par O If market interest rates remain unchanged, the bond's also decline. value. price one year from now...

2. You want to know what 2-year spot rates will be one year from now. According...

2. You want to know what 2-year spot rates will be one year from now. According to the pure expecta- tions theory, this unknown forward rate of interest is implied by current spot rates. The simplest method of calculating this forward rate is to use today's 1-year and 3-year spot rates; i.e., the spot rates that take you out to the start of, and to the end of the forward period of time you are interested in. Thus: (1 +...

2. You want to know what 2-year spot rates will be one year from now. According to the pure expecta- tions theory, this unknown forward rate of interest is implied by current spot rates. The simplest method of calculating this forward rate is to use today's 1-year and 3-year spot rates; i.e., the spot rates that take you out to the start of, and to the end of the forward period of time you are interested in. Thus: (1 +...

Question 16 1.5 pts A 5-year 5.8% annual coupon bond currently trades at 103. If interest...

Question 16 1.5 pts A 5-year 5.8% annual coupon bond currently trades at 103. If interest rates decline by 25 basis points (bps) you estimate the bond will be worth 104. If interest rates increase by 25 bps you estimate the bond will be worth 102. Based on this information what is the duration of this bond? duration s 2.0 2.0 < duration s 4.0 4.0 < duration s 6.0 6.0 < duration s 8.0 O 8.0 < duration

Question 16 1.5 pts A 5-year 5.8% annual coupon bond currently trades at 103. If interest rates decline by 25 basis points (bps) you estimate the bond will be worth 104. If interest rates increase by 25 bps you estimate the bond will be worth 102. Based on this information what is the duration of this bond? duration s 2.0 2.0 < duration s 4.0 4.0 < duration s 6.0 6.0 < duration s 8.0 O 8.0 < duration

1a) Suppose the 1-year effective annual interest rate is 4.9% and the 2-year effective rate is...

1a) Suppose the 1-year effective annual interest rate is 4.9% and the 2-year effective rate is 6.5%. Compute the fixed rate in a 2-year amortizing interest rate swap based on $460,000 of notional principal in the first year and $390,000 in the second year. Answers: a. 5.67% b. 6.62% c. 6.32% d. 5.60% e. 6.45% 1b) Suppose that 1-year, 2-year, and 3-year forward prices for the British pound are $1.76/£, $1.67/£, and $1.37/£, respectively. The 1-year, 2-year, and 3-year effective...

16 Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

16 Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

Please solve and show work fully for a rating. Thank you.

Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

Please solve and show work fully for a rating. Thank you.

Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

Can i get it solved step by step

please (not on excel if applicable

15. Suppose today's 10-year rate is 9 percent. Today's 4-year rate is 7 percent. Estimate the 6-year forward rate in four years if the 10-year rate has a .3 percent liquidity premium 5 points)

15. Suppose today's 10-year rate is 9 percent. Today's 4-year rate is 7 percent. Estimate the 6-year forward rate in four years if the 10-year rate has a .3 percent liquidity premium...

Can i get it solved step by step

please (not on excel if applicable

15. Suppose today's 10-year rate is 9 percent. Today's 4-year rate is 7 percent. Estimate the 6-year forward rate in four years if the 10-year rate has a .3 percent liquidity premium 5 points)

15. Suppose today's 10-year rate is 9 percent. Today's 4-year rate is 7 percent. Estimate the 6-year forward rate in four years if the 10-year rate has a .3 percent liquidity premium...

BF2207 Question 2 Suppose that, six months ago, you sold a call option on 1,000,000 euros (EUR) with an expiration date of six months and an exercise price of 1.1780 United States dollars (USD). You received a premium on the call option of 0.045 USD per unit. Assume the following: • Money market interest rates for EUR are constant through time and equal 5% for all maturities. • Money market interest rates for USD are constant through time and equal...

BF2207 Question 2 Suppose that, six months ago, you sold a call option on 1,000,000 euros (EUR) with an expiration date of six months and an exercise price of 1.1780 United States dollars (USD). You received a premium on the call option of 0.045 USD per unit. Assume the following: • Money market interest rates for EUR are constant through time and equal 5% for all maturities. • Money market interest rates for USD are constant through time and equal...

Question 27 1 pts A 12-year bond has an annual coupon of 9%. The coupon rate will remain fixed until the bond matures. The bond has a yield to maturity of 7%. Which of the following statements is CORRECT? O If market interest rates decline, the price of the bond will O The bond is currently selling at a price below its par O If market interest rates remain unchanged, the bond's also decline. value. price one year from now...

Question 27 1 pts A 12-year bond has an annual coupon of 9%. The coupon rate will remain fixed until the bond matures. The bond has a yield to maturity of 7%. Which of the following statements is CORRECT? O If market interest rates decline, the price of the bond will O The bond is currently selling at a price below its par O If market interest rates remain unchanged, the bond's also decline. value. price one year from now...

2. You want to know what 2-year spot rates will be one year from now. According to the pure expecta- tions theory, this unknown forward rate of interest is implied by current spot rates. The simplest method of calculating this forward rate is to use today's 1-year and 3-year spot rates; i.e., the spot rates that take you out to the start of, and to the end of the forward period of time you are interested in. Thus: (1 +...

2. You want to know what 2-year spot rates will be one year from now. According to the pure expecta- tions theory, this unknown forward rate of interest is implied by current spot rates. The simplest method of calculating this forward rate is to use today's 1-year and 3-year spot rates; i.e., the spot rates that take you out to the start of, and to the end of the forward period of time you are interested in. Thus: (1 +...

Question 16 1.5 pts A 5-year 5.8% annual coupon bond currently trades at 103. If interest rates decline by 25 basis points (bps) you estimate the bond will be worth 104. If interest rates increase by 25 bps you estimate the bond will be worth 102. Based on this information what is the duration of this bond? duration s 2.0 2.0 < duration s 4.0 4.0 < duration s 6.0 6.0 < duration s 8.0 O 8.0 < duration

Question 16 1.5 pts A 5-year 5.8% annual coupon bond currently trades at 103. If interest rates decline by 25 basis points (bps) you estimate the bond will be worth 104. If interest rates increase by 25 bps you estimate the bond will be worth 102. Based on this information what is the duration of this bond? duration s 2.0 2.0 < duration s 4.0 4.0 < duration s 6.0 6.0 < duration s 8.0 O 8.0 < duration

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago