Please solve and show work fully for a rating. Thank you.

Homework Answers

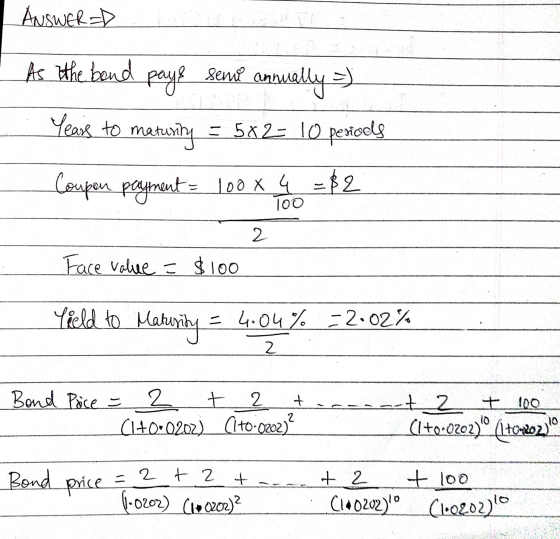

Answer - $99.8129

The solution is provided in the images attached.

Add Answer to:

Please solve and show work fully for a rating. Thank you.

129 12 65 Consider a...

12 Consider a 5-year bond with a face value of 100 USD/bond that pays coupons ev-...

12 Consider a 5-year bond with a face value of 100 USD/bond that pays coupons ev- ery six months. It has a yield to maturity of 4.0400% and an annual coupon rate of 4.0000%. What is the bond's price if there are no arbitrage opportunities? (Input your answer with 4 decimals)

12 Consider a 5-year bond with a face value of 100 USD/bond that pays coupons ev- ery six months. It has a yield to maturity of 4.0400% and an annual coupon rate of 4.0000%. What is the bond's price if there are no arbitrage opportunities? (Input your answer with 4 decimals)

Consider a 5-year bond with a face value of 100 USD/bond that pays coupons every six...

Consider a 5-year bond with a face value of 100 USD/bond that pays coupons every six months. It has a yield to maturity of 4.0400% and an annual coupon rate of 4.0000%. What is the bond’s price if there are no arbitrage opportunities? (Input your answer with 4 decimals)

Question 12 6 pts Consider a 4-year bond with a face value of 100 USD/bond that...

Question 12 6 pts Consider a 4-year bond with a face value of 100 USD/bond that pays coupons every six months. It has a yield to maturity of 3.0225% and an annual coupon rate of 3.0000%. What is the bond's price if there are no arbitrage opportunities? (Input your answer with 4 decimals) --

Question 12 6 pts Consider a 4-year bond with a face value of 100 USD/bond that pays coupons every six months. It has a yield to maturity of 3.0225% and an annual coupon rate of 3.0000%. What is the bond's price if there are no arbitrage opportunities? (Input your answer with 4 decimals) --

Please solve and show work fully for a rating. Thank you. 12 10 79 Suppose that...

Please solve and show work fully for a rating. Thank you.

12 10 79 Suppose that you buy a 3-month call for 100,000 widgets with a strike price of 7.26990 USD/Widget and pay a premium of 5 cents/Widget. Additionally, you enter into a short sale of 100,000 widgets at 6.64720 USD/Widget. At the time of maturity, the spot price is trading at 6.7137 USD/Widget. What are your profits/losses? 21,990.00 USD 15,340.00 USD -11,650.00 USD -18,360.00 USD

Please solve and show work fully for a rating. Thank you.

12 10 79 Suppose that you buy a 3-month call for 100,000 widgets with a strike price of 7.26990 USD/Widget and pay a premium of 5 cents/Widget. Additionally, you enter into a short sale of 100,000 widgets at 6.64720 USD/Widget. At the time of maturity, the spot price is trading at 6.7137 USD/Widget. What are your profits/losses? 21,990.00 USD 15,340.00 USD -11,650.00 USD -18,360.00 USD

Please solve and show work fully for a rating. Thank you. 09 8$ Suppose you do...

Please solve and show work fully for a rating. Thank you.

09 8$ Suppose you do a carry trade for one semester in USDMXN in which you make a short sale of 1,000,000 USD at 22.10 MXN/USD. If you closed this trade at 22.05 MXN/USD and the effective 3-month rates for loans and deposits is 1.2500% for MXN and 0.0625% for USD, what are your profits? (Use six decimals for your calculations but round your final answer to the nearest...

Please solve and show work fully for a rating. Thank you.

09 8$ Suppose you do a carry trade for one semester in USDMXN in which you make a short sale of 1,000,000 USD at 22.10 MXN/USD. If you closed this trade at 22.05 MXN/USD and the effective 3-month rates for loans and deposits is 1.2500% for MXN and 0.0625% for USD, what are your profits? (Use six decimals for your calculations but round your final answer to the nearest...

Please solve and show work fully for a rating. Thank you. Suppose that today's annual market...

Please solve and show work fully for a rating. Thank you.

Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

Please solve and show work fully for a rating. Thank you.

Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

Please solve and show work fully for a rating. Thank you. Suppose a credit card charges...

Please solve and show work fully for a rating. Thank you.

Suppose a credit card charges a 10% annual interest rate and recognizes the out- standing balance at the end of every month. How much would you end up paying for a 10,000 USD outstanding balance for three months? (Round the the nearest decimal) If the answer is A,B, C, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct...

Please solve and show work fully for a rating. Thank you.

Suppose a credit card charges a 10% annual interest rate and recognizes the out- standing balance at the end of every month. How much would you end up paying for a 10,000 USD outstanding balance for three months? (Round the the nearest decimal) If the answer is A,B, C, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct...

Please solve and show work fully for a rating. Thank you. You sold an option whose...

Please solve and show work fully for a rating. Thank you.

You sold an option whose MTM profits look like the picture below. What is the premium per unit that you charged your client? If the answer is A,BC, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct answer and the unit of measurement. 240,000.00 172.452.00 -175,512.00 Page 9 56.84660 59.74630 A. 3.0 USD/unit B.2.5 USD/unit C. 1.2 USD/unit...

Please solve and show work fully for a rating. Thank you.

You sold an option whose MTM profits look like the picture below. What is the premium per unit that you charged your client? If the answer is A,BC, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct answer and the unit of measurement. 240,000.00 172.452.00 -175,512.00 Page 9 56.84660 59.74630 A. 3.0 USD/unit B.2.5 USD/unit C. 1.2 USD/unit...

Please solve and show work fully for a rating. Thank you. You sold an option whose...

Please solve and show work fully for a rating. Thank you.

You sold an option whose MTM profits look like the picture below. What is the premium per unit that you charged your client? If the answer is A,BC, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct answer and the unit of measurement. 240,000.00 172.452.00 -175,512.00 Page 9 56.84660 59.74630 A. 3.0 USD/unit B.2.5 USD/unit C. 1.2 USD/unit...

Please solve and show work fully for a rating. Thank you.

You sold an option whose MTM profits look like the picture below. What is the premium per unit that you charged your client? If the answer is A,BC, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct answer and the unit of measurement. 240,000.00 172.452.00 -175,512.00 Page 9 56.84660 59.74630 A. 3.0 USD/unit B.2.5 USD/unit C. 1.2 USD/unit...

Solve the problem. Show your work and equations! Please do not show screenshots of Excel as...

Solve the problem. Show your work and equations! Please do not

show screenshots of Excel as your work shown.

1. A bond with a coupon rate of 7.30% has a price that today equals $868.92. The $1.000 face value bond pays coupon every 6 months, 30 coupons remain, and a coupon was paid yesterday. Suppose you buy this bond at today's price and hold it so that you receive 20 coupons. You sell the bond upon receiving that last coupon....

Solve the problem. Show your work and equations! Please do not

show screenshots of Excel as your work shown.

1. A bond with a coupon rate of 7.30% has a price that today equals $868.92. The $1.000 face value bond pays coupon every 6 months, 30 coupons remain, and a coupon was paid yesterday. Suppose you buy this bond at today's price and hold it so that you receive 20 coupons. You sell the bond upon receiving that last coupon....

12 Consider a 5-year bond with a face value of 100 USD/bond that pays coupons ev- ery six months. It has a yield to maturity of 4.0400% and an annual coupon rate of 4.0000%. What is the bond's price if there are no arbitrage opportunities? (Input your answer with 4 decimals)

12 Consider a 5-year bond with a face value of 100 USD/bond that pays coupons ev- ery six months. It has a yield to maturity of 4.0400% and an annual coupon rate of 4.0000%. What is the bond's price if there are no arbitrage opportunities? (Input your answer with 4 decimals)

Question 12 6 pts Consider a 4-year bond with a face value of 100 USD/bond that pays coupons every six months. It has a yield to maturity of 3.0225% and an annual coupon rate of 3.0000%. What is the bond's price if there are no arbitrage opportunities? (Input your answer with 4 decimals) --

Question 12 6 pts Consider a 4-year bond with a face value of 100 USD/bond that pays coupons every six months. It has a yield to maturity of 3.0225% and an annual coupon rate of 3.0000%. What is the bond's price if there are no arbitrage opportunities? (Input your answer with 4 decimals) --

Please solve and show work fully for a rating. Thank you.

12 10 79 Suppose that you buy a 3-month call for 100,000 widgets with a strike price of 7.26990 USD/Widget and pay a premium of 5 cents/Widget. Additionally, you enter into a short sale of 100,000 widgets at 6.64720 USD/Widget. At the time of maturity, the spot price is trading at 6.7137 USD/Widget. What are your profits/losses? 21,990.00 USD 15,340.00 USD -11,650.00 USD -18,360.00 USD

Please solve and show work fully for a rating. Thank you.

12 10 79 Suppose that you buy a 3-month call for 100,000 widgets with a strike price of 7.26990 USD/Widget and pay a premium of 5 cents/Widget. Additionally, you enter into a short sale of 100,000 widgets at 6.64720 USD/Widget. At the time of maturity, the spot price is trading at 6.7137 USD/Widget. What are your profits/losses? 21,990.00 USD 15,340.00 USD -11,650.00 USD -18,360.00 USD

Please solve and show work fully for a rating. Thank you.

09 8$ Suppose you do a carry trade for one semester in USDMXN in which you make a short sale of 1,000,000 USD at 22.10 MXN/USD. If you closed this trade at 22.05 MXN/USD and the effective 3-month rates for loans and deposits is 1.2500% for MXN and 0.0625% for USD, what are your profits? (Use six decimals for your calculations but round your final answer to the nearest...

Please solve and show work fully for a rating. Thank you.

09 8$ Suppose you do a carry trade for one semester in USDMXN in which you make a short sale of 1,000,000 USD at 22.10 MXN/USD. If you closed this trade at 22.05 MXN/USD and the effective 3-month rates for loans and deposits is 1.2500% for MXN and 0.0625% for USD, what are your profits? (Use six decimals for your calculations but round your final answer to the nearest...

Please solve and show work fully for a rating. Thank you.

Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

Please solve and show work fully for a rating. Thank you.

Suppose that today's annual market interest rates are 2.5% for a 2-year deposit/loan, 3.5% for a 3-year deposit/loan, and 4.5% for a 4-year deposit/loan. What is the forward interest rate for a 2-year deposit in 2-year's time. (Use six decimals for your computations) 3.50000% 2.00000% 6.03921% 7.06127% 6.5390%

Please solve and show work fully for a rating. Thank you.

Suppose a credit card charges a 10% annual interest rate and recognizes the out- standing balance at the end of every month. How much would you end up paying for a 10,000 USD outstanding balance for three months? (Round the the nearest decimal) If the answer is A,B, C, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct...

Please solve and show work fully for a rating. Thank you.

Suppose a credit card charges a 10% annual interest rate and recognizes the out- standing balance at the end of every month. How much would you end up paying for a 10,000 USD outstanding balance for three months? (Round the the nearest decimal) If the answer is A,B, C, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct...

Please solve and show work fully for a rating. Thank you.

You sold an option whose MTM profits look like the picture below. What is the premium per unit that you charged your client? If the answer is A,BC, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct answer and the unit of measurement. 240,000.00 172.452.00 -175,512.00 Page 9 56.84660 59.74630 A. 3.0 USD/unit B.2.5 USD/unit C. 1.2 USD/unit...

Please solve and show work fully for a rating. Thank you.

You sold an option whose MTM profits look like the picture below. What is the premium per unit that you charged your client? If the answer is A,BC, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct answer and the unit of measurement. 240,000.00 172.452.00 -175,512.00 Page 9 56.84660 59.74630 A. 3.0 USD/unit B.2.5 USD/unit C. 1.2 USD/unit...

Please solve and show work fully for a rating. Thank you.

You sold an option whose MTM profits look like the picture below. What is the premium per unit that you charged your client? If the answer is A,BC, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct answer and the unit of measurement. 240,000.00 172.452.00 -175,512.00 Page 9 56.84660 59.74630 A. 3.0 USD/unit B.2.5 USD/unit C. 1.2 USD/unit...

Please solve and show work fully for a rating. Thank you.

You sold an option whose MTM profits look like the picture below. What is the premium per unit that you charged your client? If the answer is A,BC, or D, simply type the respective letter in the answer box. If the answer is E, write down the correct answer and the unit of measurement. 240,000.00 172.452.00 -175,512.00 Page 9 56.84660 59.74630 A. 3.0 USD/unit B.2.5 USD/unit C. 1.2 USD/unit...

Solve the problem. Show your work and equations! Please do not

show screenshots of Excel as your work shown.

1. A bond with a coupon rate of 7.30% has a price that today equals $868.92. The $1.000 face value bond pays coupon every 6 months, 30 coupons remain, and a coupon was paid yesterday. Suppose you buy this bond at today's price and hold it so that you receive 20 coupons. You sell the bond upon receiving that last coupon....

Solve the problem. Show your work and equations! Please do not

show screenshots of Excel as your work shown.

1. A bond with a coupon rate of 7.30% has a price that today equals $868.92. The $1.000 face value bond pays coupon every 6 months, 30 coupons remain, and a coupon was paid yesterday. Suppose you buy this bond at today's price and hold it so that you receive 20 coupons. You sell the bond upon receiving that last coupon....

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago