Just need help with required A, Required B is correct

Homework Answers

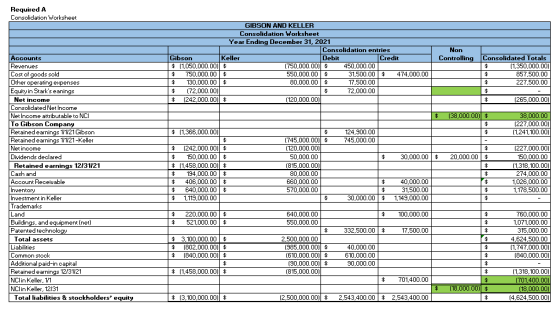

Mistake is mainly in Non Controlling Interest, -38000 should be mentioned in Non Controlling Interest, instaed of Earning in Equity of Keller

Further, non controlling interest on 12/31/21 is correct. An alternate presentation for the same is shown below. Answer might match by doing this as follows Changes are highlighted in Green-

.

Add Answer to:

Just need help with required A, Required B is correct

The Individual financial statements for Gibson...

The Individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The Individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2021, follow. Gibson acquired a 60 percent Interest in Keller on January 1, 2020, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling Interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value $350,000. This Intangible asset...

The Individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2021, follow. Gibson acquired a 60 percent Interest in Keller on January 1, 2020, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling Interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value $350,000. This Intangible asset...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $350,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $350,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2021, follow.

Gibson acquired a 60 percent interest in Keller on January 1, 2020, in exchange for various considerations totaling $810,000. At the acquisition date, the fair value of the noncontrolling interest was $540,000 and Keller’s book value was $1,080,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $270,000. This intangible asset is being amortized over 20 years. Gibson uses the partial equity method to account for its investment...

Gibson acquired a 60 percent interest in Keller on January 1, 2020, in exchange for various considerations totaling $810,000. At the acquisition date, the fair value of the noncontrolling interest was $540,000 and Keller’s book value was $1,080,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $270,000. This intangible asset is being amortized over 20 years. Gibson uses the partial equity method to account for its investment...

Problem 5-35 (LO 5-1, 5-2, 5-3, 5-4, 5-5, 5-6, 5-7) The individual financial statements for Gibson Company and Keller C...

Problem 5-35 (LO 5-1, 5-2, 5-3, 5-4, 5-5, 5-6, 5-7) The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $420,000. At the acquisition date, the fair value of the noncontrolling interest was $280,000 and Keller's book value was $550,000. Keller had developed internally a customer list that was not recorded on its books...

Problem 5-35 (LO 5-1, 5-2, 5-3, 5-4, 5-5, 5-6, 5-7) The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $420,000. At the acquisition date, the fair value of the noncontrolling interest was $280,000 and Keller's book value was $550,000. Keller had developed internally a customer list that was not recorded on its books...

Problem 5-35 (LO 5-1, 5-2, 5-3, 5-4, 5-5, 5-6, 5-7) The individual financial statements for Gibson...

Problem 5-35 (LO 5-1, 5-2, 5-3, 5-4, 5-5, 5-6, 5-7) The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $780,000. At the acquisition date, the fair value of the noncontrolling interest was $520,000 and Keller’s book value was $1,040,000. Keller had developed internally a customer list that was not recorded on its books...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $510,000. At the acquisition date, the fair value of the noncontrolling interest was $340,000 and Keller's book value was $670,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $180,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $510,000. At the acquisition date, the fair value of the noncontrolling interest was $340,000 and Keller's book value was $670,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $180,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $420,000. At the acquisition date, the fair value of the noncontrolling interest was $280,000 and Keller’s book value was $550,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $150,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $570,000. At the acquisition date, the fair value of the noncontrolling interest was $380,000 and Keller’s book value was $850,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $100,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

a. Prepare a worksheet to consolidate the separate 2021 financial statements for Gibson and Keller.

b. How would the consolidation entries in requirement (a) have differed if Gibson had sold a building on January 2, 2020, with a

$155,000 book value (cost of $330,000) to Keller for $290,000 instead of land, as the problem reports? Assume that the building

had a 10-year remaining life at the date of transfer.

Complete this question by entering your answers in the tabs below.The...

a. Prepare a worksheet to consolidate the separate 2021 financial statements for Gibson and Keller.

b. How would the consolidation entries in requirement (a) have differed if Gibson had sold a building on January 2, 2020, with a

$155,000 book value (cost of $330,000) to Keller for $290,000 instead of land, as the problem reports? Assume that the building

had a 10-year remaining life at the date of transfer.

Complete this question by entering your answers in the tabs below.The...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $450,000. At the acquisition date, the fair value of the noncontrolling interest was $300,000 and Keller’s book value was $590,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $160,000. This intangible...

The Individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2021, follow. Gibson acquired a 60 percent Interest in Keller on January 1, 2020, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling Interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value $350,000. This Intangible asset...

The Individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2021, follow. Gibson acquired a 60 percent Interest in Keller on January 1, 2020, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling Interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value $350,000. This Intangible asset...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $350,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $350,000. This intangible...

Problem 5-35 (LO 5-1, 5-2, 5-3, 5-4, 5-5, 5-6, 5-7) The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $420,000. At the acquisition date, the fair value of the noncontrolling interest was $280,000 and Keller's book value was $550,000. Keller had developed internally a customer list that was not recorded on its books...

Problem 5-35 (LO 5-1, 5-2, 5-3, 5-4, 5-5, 5-6, 5-7) The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $420,000. At the acquisition date, the fair value of the noncontrolling interest was $280,000 and Keller's book value was $550,000. Keller had developed internally a customer list that was not recorded on its books...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $510,000. At the acquisition date, the fair value of the noncontrolling interest was $340,000 and Keller's book value was $670,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $180,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $510,000. At the acquisition date, the fair value of the noncontrolling interest was $340,000 and Keller's book value was $670,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $180,000. This intangible...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago