Homework Answers

Add Answer to:

Consider the following two banks: Bank 1 has assets composed solely of a 10-year, 12.50 percent...

Consider the following two banks: Bank 1 has assets composed solely of a 10-year, 13.25 percent...

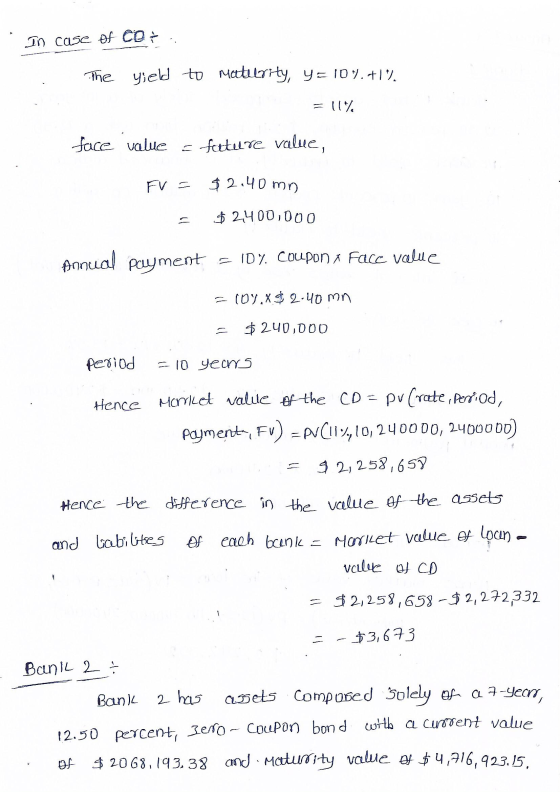

Consider the following two banks: Bank 1 has assets composed solely of a 10-year, 13.25 percent coupon, $2.7 million loan with a 13.25 percent yield to maturity. It is financed with a 10-year, 10 percent coupon, $2.7 million CD with a 10 percent yield to maturity. Bank 2 has assets composed solely of a 7-year, 13.25 percent, zero-coupon bond with a current value of $2,285,241.72 and a maturity value of $5,460,087.71. It is financed by a 10-year, 7.50 percent coupon,...

Consider the following two banks: Bank 1 has assets composed solely of a 10-year, 13.25 percent coupon, $2.7 million loan with a 13.25 percent yield to maturity. It is financed with a 10-year, 10 percent coupon, $2.7 million CD with a 10 percent yield to maturity. Bank 2 has assets composed solely of a 7-year, 13.25 percent, zero-coupon bond with a current value of $2,285,241.72 and a maturity value of $5,460,087.71. It is financed by a 10-year, 7.50 percent coupon,...

Q1) Two banks are being examined by regulators to determine the interest rate sensitivity of their...

Q1) Two banks are being examined by regulators to determine the interest rate sensitivity of their balance sheets. Bank A has assets composed solely of a 10-year $1 million loan with a coupon rate and yield of 12 percent. The loan is financed with a 10-year $1 million CD with a coupon rate and yield of 10 percent. Bank B has assets composed solely of a 7-year, 12 percent zero-coupon bond with a current (market) value of $894,006.20 $1,976,362.88. The...

Q1) Two banks are being examined by regulators to determine the interest rate sensitivity of their balance sheets. Bank A has assets composed solely of a 10-year $1 million loan with a coupon rate and yield of 12 percent. The loan is financed with a 10-year $1 million CD with a coupon rate and yield of 10 percent. Bank B has assets composed solely of a 7-year, 12 percent zero-coupon bond with a current (market) value of $894,006.20 $1,976,362.88. The...

If the required rate of return on the stock is 15 percent, what should the fair...

If the required rate of return on the stock is 15 percent, what should the fair value be four years from today? 4 Consider the following two banks: Bank 1 has assets composed solely of a 10-year, 12 percent coupon, $1 million loan with a 12 percent yield to maturity. It is financed with a 10-year, 10 percent coupon, $1 million CD with a 10 percent yield to maturity. Bank 2 has assets composed solely of a 7-year, 12 percent,...

A bank has issued a six-month, $1.6 million negotiable CD with a 0.45 percent quoted annual...

A bank has issued a six-month, $1.6 million negotiable CD with a 0.45 percent quoted annual interest rate fico, sp). a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $2 million CD falls to $1,598,900. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $1.6 million...

A bank has issued a six-month, $1.6 million negotiable CD with a 0.45 percent quoted annual interest rate fico, sp). a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $2 million CD falls to $1,598,900. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $1.6 million...

A bank has issued a six-month, $2.8 million negotiable CD with a 0.55 percent quoted annual...

A bank has issued a six-month, $2.8 million negotiable CD with a 0.55 percent quoted annual interest rate lico, spl a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $3 million CD falls to $2799.000. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $2.8 million...

A bank has issued a six-month, $2.8 million negotiable CD with a 0.55 percent quoted annual interest rate lico, spl a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $3 million CD falls to $2799.000. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $2.8 million...

A bank has issued a six-month, $2.8 million negotiable CD with a 0.55 percent quoted annual...

A bank has issued a six-month, $2.8 million negotiable CD with a 0.55 percent quoted annual interest rate lico, spl a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $3 million CD falls to $2799.000. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $2.8 million...

A bank has issued a six-month, $2.8 million negotiable CD with a 0.55 percent quoted annual interest rate lico, spl a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $3 million CD falls to $2799.000. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $2.8 million...

(a) A Bank has a bond with a maturity of 4 years. The coupon rate of...

(a) A Bank has a bond with a maturity of 4 years. The coupon rate of the bond is 8%, the yield to maturity is 9%, and the face value is 1 million dollars. Interest payment will be paid annually. Determine the price (present value) and duration of the bond. (9 marks) (b) Predict the change in the bond price if interest rates rise by 100 basis points based on the duration of the bond that you have calculated in...

A five-year 2.4% defaultable coupon bond is selling to yield 3% (Annual Percent Rate and semi-annual...

A five-year 2.4% defaultable coupon bond is selling to yield 3% (Annual Percent Rate and semi-annual compounding). The bond pays interest semi-annually. The risk-free yield is 2.4%. Therefore, its current credit spread is 3% -2.4% = 0.6%. Two years later its credit spread increases from 0.6% to 1% while the risk-free yield doesn’t change. Assuming the face value of the coupon bond and risk-free bond is 100. a)What is the return of investing in this bond over the two year?...

Q3. Follow Bank has a S1 million position in a five-year, zero-coupon bond with a face...

Q3. Follow Bank has a S1 million position in a five-year, zero-coupon bond with a face value of $1,402,552. The bond is trading at a yield to maturity of 7.00 percent. The historical mean change in daily yields is 0.0 percent and the standard deviation is 12 basis points a. What is the modified duration of the bond? What is the maximum adverse daily yield move given that we desire no more than a 5 percent chance that yield changes...

Q3. Follow Bank has a S1 million position in a five-year, zero-coupon bond with a face value of $1,402,552. The bond is trading at a yield to maturity of 7.00 percent. The historical mean change in daily yields is 0.0 percent and the standard deviation is 12 basis points a. What is the modified duration of the bond? What is the maximum adverse daily yield move given that we desire no more than a 5 percent chance that yield changes...

An insurance company must make payments to a customer of 10$ million in one year and...

An insurance company must make payments to a customer of 10$ million in one year and 5$ million in five years. The yield curve is flat at 10%. a. If it wants to fully find and immunize its obligation to this customer with a single issue of a zero-coupon bond, what maturity bond must it purchase? b. What amount should be invested in the zero-coupon bonds? What will be the maturity value of the zero-coupon bonds? c. What will be...

Consider the following two banks: Bank 1 has assets composed solely of a 10-year, 13.25 percent coupon, $2.7 million loan with a 13.25 percent yield to maturity. It is financed with a 10-year, 10 percent coupon, $2.7 million CD with a 10 percent yield to maturity. Bank 2 has assets composed solely of a 7-year, 13.25 percent, zero-coupon bond with a current value of $2,285,241.72 and a maturity value of $5,460,087.71. It is financed by a 10-year, 7.50 percent coupon,...

Consider the following two banks: Bank 1 has assets composed solely of a 10-year, 13.25 percent coupon, $2.7 million loan with a 13.25 percent yield to maturity. It is financed with a 10-year, 10 percent coupon, $2.7 million CD with a 10 percent yield to maturity. Bank 2 has assets composed solely of a 7-year, 13.25 percent, zero-coupon bond with a current value of $2,285,241.72 and a maturity value of $5,460,087.71. It is financed by a 10-year, 7.50 percent coupon,...

Q1) Two banks are being examined by regulators to determine the interest rate sensitivity of their balance sheets. Bank A has assets composed solely of a 10-year $1 million loan with a coupon rate and yield of 12 percent. The loan is financed with a 10-year $1 million CD with a coupon rate and yield of 10 percent. Bank B has assets composed solely of a 7-year, 12 percent zero-coupon bond with a current (market) value of $894,006.20 $1,976,362.88. The...

Q1) Two banks are being examined by regulators to determine the interest rate sensitivity of their balance sheets. Bank A has assets composed solely of a 10-year $1 million loan with a coupon rate and yield of 12 percent. The loan is financed with a 10-year $1 million CD with a coupon rate and yield of 10 percent. Bank B has assets composed solely of a 7-year, 12 percent zero-coupon bond with a current (market) value of $894,006.20 $1,976,362.88. The...

A bank has issued a six-month, $1.6 million negotiable CD with a 0.45 percent quoted annual interest rate fico, sp). a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $2 million CD falls to $1,598,900. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $1.6 million...

A bank has issued a six-month, $1.6 million negotiable CD with a 0.45 percent quoted annual interest rate fico, sp). a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $2 million CD falls to $1,598,900. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $1.6 million...

A bank has issued a six-month, $2.8 million negotiable CD with a 0.55 percent quoted annual interest rate lico, spl a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $3 million CD falls to $2799.000. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $2.8 million...

A bank has issued a six-month, $2.8 million negotiable CD with a 0.55 percent quoted annual interest rate lico, spl a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $3 million CD falls to $2799.000. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $2.8 million...

A bank has issued a six-month, $2.8 million negotiable CD with a 0.55 percent quoted annual interest rate lico, spl a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $3 million CD falls to $2799.000. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $2.8 million...

A bank has issued a six-month, $2.8 million negotiable CD with a 0.55 percent quoted annual interest rate lico, spl a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $3 million CD falls to $2799.000. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $2.8 million...

Q3. Follow Bank has a S1 million position in a five-year, zero-coupon bond with a face value of $1,402,552. The bond is trading at a yield to maturity of 7.00 percent. The historical mean change in daily yields is 0.0 percent and the standard deviation is 12 basis points a. What is the modified duration of the bond? What is the maximum adverse daily yield move given that we desire no more than a 5 percent chance that yield changes...

Q3. Follow Bank has a S1 million position in a five-year, zero-coupon bond with a face value of $1,402,552. The bond is trading at a yield to maturity of 7.00 percent. The historical mean change in daily yields is 0.0 percent and the standard deviation is 12 basis points a. What is the modified duration of the bond? What is the maximum adverse daily yield move given that we desire no more than a 5 percent chance that yield changes...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago