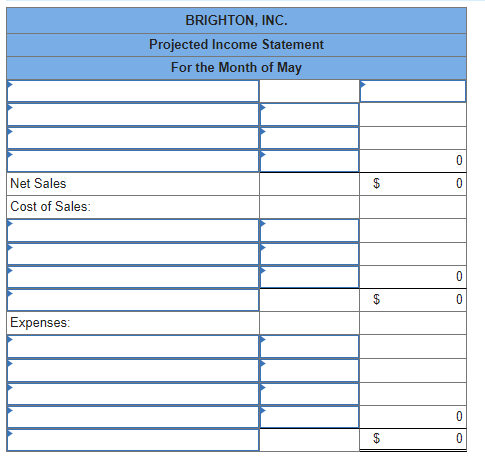

Prepare a projected income statement for May. The cost of goods sold should equal the variable manufacturing cost per unit times the number of units sold plus the total fixed manufacturing cost budgeted for the period. When calculating net sales assume cash discounts of 1 percent and bad debt expense of 0.50 percent. (Do not round intermediate calculations.)

Homework Answers

| Please give positive ratings so I can keep answering. It would help me a lot. Please comment if you have any query. Thanks! |

| Brighton Inc. | |||||

| Workings | |||||

| Production Budget | April | May | June | July | Note |

| Budgeted Sales units | 600,000.00 | 450,000.00 | 600,000.00 | 600,000.00 | See A |

| Add: Closing | 112,500.00 | 150,000.00 | 150,000.00 | B= 25% of A of next month. | |

| Total needs | 712,500.00 | 600,000.00 | 750,000.00 | ||

| Less: Opening | 150,000.00 | 112,500.00 | 150,000.00 | C= 25% of A of same month. | |

| Production Budget- Units | 562,500.00 | 487,500.00 | 600,000.00 | D |

| Answer a- 2 | ||||

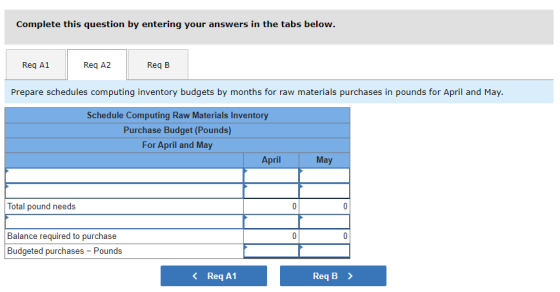

| Inventory Budget | April | May | June | Note |

| Production Budget- Units | 562,500.00 | 487,500.00 | 600,000.00 | See D |

| Material required per tile | 0.25 | 0.25 | 0.25 | E |

| Material required for production | 140,625.00 | 121,875.00 | 150,000.00 | F=D*E |

| Add: Closing | 36,563.00 | 45,000.00 | G= 50% of F of next month. | |

| Total pound needs | 177,188.00 | 166,875.00 | ||

| Less: Opening | 42,188.00 | 44,563.00 | H= For April its given in question. For May see N of April. | |

| Material Purchase Budget (pounds) | 135,000.00 | 122,312.00 | I | |

| Pounds per batch | 71,500.00 | 68,500.00 | J | |

| Number of batches | 1.89 | 1.79 | K=I/J | |

| Batches should be whole figure so it should be | 2.00 | 2.00 | L | |

| Material Purchase Budget (pounds) | 143,000.00 | 137,000.00 | M=J*L | |

| Calculation of closing quantity | April | May | ||

| Opening | 42,188.00 | 44,563.00 | See H | |

| Add: Purchases | 143,000.00 | 137,000.00 | See M | |

| Less: Used in production | 140,625.00 | 121,875.00 | See F | |

| Closing quantity | 44,563.00 | 59,688.00 | N |

| Ans b | ||

| Workings for Income Statement | ||

| Sales Budget | May | Note |

| Sales (units) | 450,000.00 | See A |

| Sell Price | 4.00 | O |

| Sales Budget | 1,800,000.00 | P=A*O |

| Cash discounts at 1 % | 18,000.00 | Q=P*1% |

| Bad debt expense at 0.50 % | 9,000.00 | R=P*0.5% |

| Selling expenses at 10 % | 180,000.00 | S=P*10% |

| Material usages Budget | May | |

| Sales (units) | 450,000.00 | See A |

| Material required per unit | 0.25 | See E |

| Material needed | 112,500.00 | T=A*E |

| Cost per pound | 4.00 | U |

| Material usages Budget ($) | 450,000.00 | V=T*U |

| Direct Labor Budget | May | |

| Normal production | 500,000.00 | W |

| Labor cost | 390,000.00 | X |

| Labor cost per unit | 0.78 | Y=X/W |

| Sales (units) | 450,000.00 | See A |

| Direct Labor cost | 351,000.00 | Z=Y*A |

| Manufacturing Overhead Budget | May | |

| Normal production | 500,000.00 | See W |

| Variable Overhead | 190,000.00 | AA |

| Variable Overhead rate per unit | 0.38 | AB=AA/W |

| Variable Overhead Budget | 171,000.00 | AC=AB*A |

| Fixed Overhead Budget | 390,000.00 | AD |

| Manufacturing Overhead Budget | 561,000.00 | AE=AC+AD |

| Income Statement | May | |

| Sales Revenues | 1,800,000.00 | See P |

| Less: Cash discounts | 18,000.00 | See Q |

| Net Sales | 1,782,000.00 | |

| Less: Cost of goods sold | ||

| Material usages |

Know the answer?

Add Answer to:

|

Brighton, Inc., manufactures kitchen tiles. The company recently expanded, and the controller believes that it will need to borrow cash to continue operations. It began negotiating for a one-month bank loan of $400,000 starting May 1. The bank would charge interest at the rate of 0.75 percent per month and require the company to repay interest and principal on May 31. In considering the loan, the bank requested a projected income statement and cash budget for May. The following information...

Brighton, Inc., manufactures kitchen tiles. The company recently expanded, and the controller believes that it will need to borrow cash to continue operations. It began negotiating for a one-month bank loan of $400,000 starting May 1. The bank would charge interest at the rate of 0.75 percent per month and require the company to repay interest and principal on May 31. In considering the loan, the bank requested a projected income statement and cash budget for May. The following information...

Brighton, Inc., manufactures kitchen tiles. The company recently expanded, and the controller believes that it will need to borrow cash to continue operations. It began negotiating for a one-month bank loan of $500,000 starting May 1. The bank would charge interest at the rate of 0.75 percent per month and require the company to repay interest and principal on May 31. In considering the loan, the bank requested a projected income statement and cash budget for May. The following information...

Brighton, Inc., manufactures kitchen tiles. The company recently expanded, and the controller believes that it will need to borrow cash to continue operations. It began negotiating for a one-month bank loan of $500,000 starting May 1. The bank would charge interest at the rate of 0.75 percent per month and require the company to repay interest and principal on May 31. In considering the loan, the bank requested a projected income statement and cash budget for May. The following information...

Brighton, Inc., manufactures kitchen tiles. The company recently

expanded, and the controller believes that it will need to borrow

cash to continue operations. It began negotiating for a one-month

bank loan of $500,000 starting May 1. The bank would charge

interest at the rate of 0.75 percent per month and require the

company to repay interest and principal on May 31. In considering

the loan, the bank requested a projected income statement and cash

budget for May.

The following information...

Brighton, Inc., manufactures kitchen tiles. The company recently

expanded, and the controller believes that it will need to borrow

cash to continue operations. It began negotiating for a one-month

bank loan of $500,000 starting May 1. The bank would charge

interest at the rate of 0.75 percent per month and require the

company to repay interest and principal on May 31. In considering

the loan, the bank requested a projected income statement and cash

budget for May.

The following information...

Brighton, Inc., manufactures kitchen tiles. The company recently expanded, and the controller believes that it will need to borrow cash to continue operations. It began negotiating for a one-month bank loan of $500,000 starting May 1. The bank would charge interest at the rate of 1.00 percent per month and require the company to repay interest and principal on May 31. In considering the loan, the bank requested a projected income statement and cash budget for May. The following information...

Brighton, Inc., manufactures kitchen tiles. The company recently expanded, and the controller believes that it will need to borrow cash to continue operations. It began negotiating for a one-month bank loan of $500,000 starting May 1. The bank would charge interest at the rate of 1.00 percent per month and require the company to repay interest and principal on May 31. In considering the loan, the bank requested a projected income statement and cash budget for May. The following information...

Brighton, Inc., manufactures kitchen tiles. The company recently expanded, and the controller believes that it will need to borrow cash to continue operations. It began negotiating for a one-month bank loan of $500,000 starting May 1. The bank would charge interest at the rate of 1.00 percent per month and require the company to repay interest and principal on May 31. In considering the loan, the bank requested a projected income statement and cash budget for May. The following information...

Brighton, Inc., manufactures kitchen tiles. The company recently expanded, and the controller believes that it will need to borrow cash to continue operations. It began negotiating for a one-month bank loan of $500,000 starting May 1. The bank would charge interest at the rate of 1.00 percent per month and require the company to repay interest and principal on May 31. In considering the loan, the bank requested a projected income statement and cash budget for May. The following information...

Please help with explanation. Thank you in advance.

Brighton, Inc., manufactures kitchen tiles. The company recently expanded, and the controller believes that it will need to borrow cash to continue operations. It began negotiating for a one-month bank loan of $500,000 starting May 1. The bank would charge interest at the rate of 1.00 percent per month and require the company to repay interest and principal on May 31. In considering the loan, the bank requested a projected income statement...

Please help with explanation. Thank you in advance.

Brighton, Inc., manufactures kitchen tiles. The company recently expanded, and the controller believes that it will need to borrow cash to continue operations. It began negotiating for a one-month bank loan of $500,000 starting May 1. The bank would charge interest at the rate of 1.00 percent per month and require the company to repay interest and principal on May 31. In considering the loan, the bank requested a projected income statement...