Question 1 Under GAAP, a corporation that recognizes bad debt expense for accounts receivable using the...

Question 1

Under GAAP, a corporation that recognizes bad debt expense for accounts receivable using the allowance method. These estimated receivables that cannot yet be written off for tax purposes result in a deferred tax asset.

a. True or false? Explain.

b. If these debts actually become worthless, what is the reversing effect?

Question 2

Read IRC §448(a) and (c)(1) and IRC §471(c). The $25 million has been adjusted for inflation to $26 million.

In your own words, consulting your text, explain these provisions. Limit your answer to 100 words.

You can find the Code sections at Cornell Law School LII using any search engine.

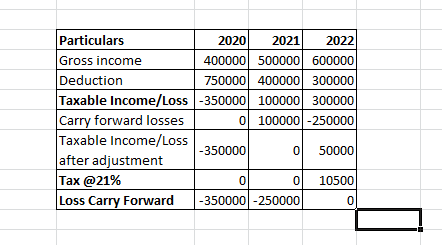

Question 3

Phyllis Corporation has gross income and deductions as follows:

2020 2021 2022

Gross income 400,000 500,000 600,000

Deductions 750,000 400,000 300,000

How much is the corporations gross tax for each year 2020 – 2022. Recall that the corporate tax rate is 21%.

Homework Answers

Answer 1 (a) True as in Income Tax Act Bad debts is allowed as per ICDS (Income Computation and Disclosure Standard). In accounting bad debt is enter but income tax alowed them when they are permanently bad debt.

Answer 1 (b) When bad debt are permanent then it will be allowed to the amount disallowed earlier and DTA created will be adjusted.

Answer 3 Corporate tax will be:

Under ncome tax Act Carry forward of losses is allowed only for 8 Assessment Years.

Add Answer to:

Question 1

Under GAAP, a corporation that recognizes bad debt expense for

accounts receivable using the...

LOL (the “Company”), an SEC registrant with a calendar year-end, is a manufacturer and distributor of sports equipment....

LOL (the “Company”), an SEC registrant with a calendar year-end,

is a manufacturer and distributor of sports equipment. The Company

was created in 1989 and is headquartered in Southern California.

The Company has manufacturing operations and numerous sales and

administrative locations in the United States. LOL files a

consolidated U.S. federal tax return. (This case will not consider

the evaluation of the state jurisdictions; it will only consider

the federal jurisdiction.)

As LOL’s auditors, you are now performing the Company’s...

LOL (the “Company”), an SEC registrant with a calendar year-end,

is a manufacturer and distributor of sports equipment. The Company

was created in 1989 and is headquartered in Southern California.

The Company has manufacturing operations and numerous sales and

administrative locations in the United States. LOL files a

consolidated U.S. federal tax return. (This case will not consider

the evaluation of the state jurisdictions; it will only consider

the federal jurisdiction.)

As LOL’s auditors, you are now performing the Company’s...

LOL (the “Company”), an SEC registrant with a calendar year-end,

is a manufacturer and distributor of sports equipment. The Company

was created in 1989 and is headquartered in Southern California.

The Company has manufacturing operations and numerous sales and

administrative locations in the United States. LOL files a

consolidated U.S. federal tax return. (This case will not consider

the evaluation of the state jurisdictions; it will only consider

the federal jurisdiction.)

As LOL’s auditors, you are now performing the Company’s...

LOL (the “Company”), an SEC registrant with a calendar year-end,

is a manufacturer and distributor of sports equipment. The Company

was created in 1989 and is headquartered in Southern California.

The Company has manufacturing operations and numerous sales and

administrative locations in the United States. LOL files a

consolidated U.S. federal tax return. (This case will not consider

the evaluation of the state jurisdictions; it will only consider

the federal jurisdiction.)

As LOL’s auditors, you are now performing the Company’s...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago