Hi...

The question is complete and it consistis

A and B

B has I and II

In overall the question is about 2 pages that has been attage.

full answer work in excel is prefered..

Homework Answers

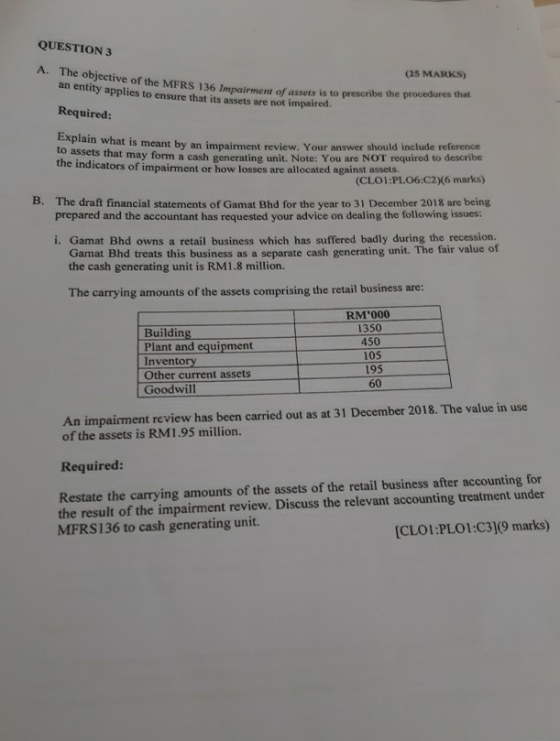

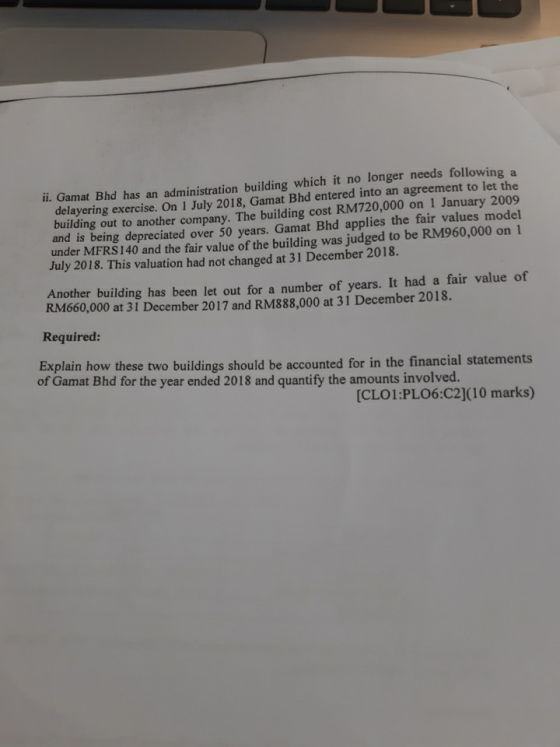

An Impairment review compares the carrying amount of an asset with the higher of existing use value/ depreciated replacement cost and net relisable value.However,if an asset cannot be used or is surplus to its requirements the Impairment review compares the carrying amount of asset with net realisable value only,Since thhere is no value in use.

Net realisable value it is the amount for which an asset can be disposed of less any direct selling costs

Direct Selling Cost include legal cost and the cost of removing a tenant

If the asset is overspecified for its current use,impairment reveiw compares the carrying amount of asset with the higher of net realisable value and the existing use value\depreciated replacement cost of an asset of the lower specification.

If there is any indication that an asset may be impaired, the recoverable amount shall be estimated for the individual asset. If it is not possible to estimate the recoverable amount of the individual asset, an entity shall determine the recoverable amount of the cash-generating unit to which the asset belongs (the asset’s cash-generating unit)

Recognition of Cash generating Unit

An asset or a group of assets which produced an output in an active market should be identified as CGU

When an entity estimates future cash Flows to determine the value in use of a CGU using the output . an asset or a group of assets which produced an output in an active market should be identified as a CGU.

MFRS 136/ FRS 136 requires that the cash inflows generated by an asset or CGU are affected by internal transfer pricing , an entity should use managements best etimate of future prices that could be achevied in arms length transactions .

Add Answer to:

Hi...

The question is complete and it consistis

A and B

B has I and II...

How is this calculated step-by-step The draft financial statements for Candelle plc for the year to...

How is this calculated step-by-step

The draft financial statements for Candelle plc for the year to December 31 2016 are being prepared and the accountant had asked your advice on the following issues. A. Candelle plc has an administration building which it no longer needs. On 1 July 2016 Candelle plc entered into an agreement to lease the building out to another company. The building cost 600,000 on 1 January 2007 and is being depreciated over 50 years, based on...

How is this calculated step-by-step

The draft financial statements for Candelle plc for the year to December 31 2016 are being prepared and the accountant had asked your advice on the following issues. A. Candelle plc has an administration building which it no longer needs. On 1 July 2016 Candelle plc entered into an agreement to lease the building out to another company. The building cost 600,000 on 1 January 2007 and is being depreciated over 50 years, based on...

a) At 31 December 2017, Senyum Sdn Bhd had a deferred tax liability of RM38,000. At...

a) At 31 December 2017, Senyum Sdn Bhd had a deferred tax liability of RM38,000. At 31 December 2018, the deferred tax liability is RM45,000. The company's 2018 current tax payable is RM50,000. Required: i) Compute the tax expense for Senyum Sdn Bhd for the year 2018. (5 marks) (CLO1:PLO1:C3) ii) Briefly explain what deferred tax is. (2 marks) (CLO1:PLO1:C1) b) Murni Berhad recognised a deferred tax liability for the year ended 31 March 2017 which was related solely to...

a) At 31 December 2017, Senyum Sdn Bhd had a deferred tax liability of RM38,000. At 31 December 2018, the deferred tax liability is RM45,000. The company's 2018 current tax payable is RM50,000. Required: i) Compute the tax expense for Senyum Sdn Bhd for the year 2018. (5 marks) (CLO1:PLO1:C3) ii) Briefly explain what deferred tax is. (2 marks) (CLO1:PLO1:C1) b) Murni Berhad recognised a deferred tax liability for the year ended 31 March 2017 which was related solely to...

Problem 1 The Faris Corporation has determined that there may be indicators of impairment for one...

Problem 1 The Faris Corporation has determined that there may be indicators of impairment for one of their assets - an office building that is currently leased out and a cash generating unit (CGU) representing a business unit. Data for the building and CGU follow. The year end is December 31, 20x4. Building Carrying value (20 years remaining, $500,000 residual value) Fair value Costs to sell Future cash flows generated by building (each year to the end of its useful...

Problem 1 The Faris Corporation has determined that there may be indicators of impairment for one of their assets - an office building that is currently leased out and a cash generating unit (CGU) representing a business unit. Data for the building and CGU follow. The year end is December 31, 20x4. Building Carrying value (20 years remaining, $500,000 residual value) Fair value Costs to sell Future cash flows generated by building (each year to the end of its useful...

This is BBM206/05 Business Accounting II subject Question 2 Kopi Sdn Bhd's statement of profit or...

This is BBM206/05 Business Accounting

II subject

Question 2 Kopi Sdn Bhd's statement of profit or loss for the year ended 31 December 2018 and statements of financial position at 31 December 2017 and 31 December 2018 were as following: STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED 31 DECEMBER 2018 RM'000 RM'000 Revenue 720 Raw materials consumed 70 Staff costs 94 Depreciation 118 Loss on disposal of non-current asset 18 Interest payable (28) Profit before tax Taxation (124)...

This is BBM206/05 Business Accounting

II subject

Question 2 Kopi Sdn Bhd's statement of profit or loss for the year ended 31 December 2018 and statements of financial position at 31 December 2017 and 31 December 2018 were as following: STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED 31 DECEMBER 2018 RM'000 RM'000 Revenue 720 Raw materials consumed 70 Staff costs 94 Depreciation 118 Loss on disposal of non-current asset 18 Interest payable (28) Profit before tax Taxation (124)...

Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandaph Corporation purchased a...

Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandaph Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $ 75,000...

Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandaph Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $ 75,000...

Question #5-Asset Impairment: The recording unit of Turner Technologies Inc. (TTI) has been suffering a decline in its...

Question #5-Asset Impairment: The recording unit of Turner Technologies Inc. (TTI) has been suffering a decline in its business, due to new product introductions by competitors. At 31 December 2018, the assets of the abrasives cash- generating unit are shown as follows (in millions) on the company's SFP: Cost Accumulated Net Book Depreciation Value S 470 Equipment (10-year life) Fixtures (10-year life) 950 480 430 340 90 120 Patent rights (40-year life) 280 160 S1,660 $680 $980 An impairment test...

Question #5-Asset Impairment: The recording unit of Turner Technologies Inc. (TTI) has been suffering a decline in its business, due to new product introductions by competitors. At 31 December 2018, the assets of the abrasives cash- generating unit are shown as follows (in millions) on the company's SFP: Cost Accumulated Net Book Depreciation Value S 470 Equipment (10-year life) Fixtures (10-year life) 950 480 430 340 90 120 Patent rights (40-year life) 280 160 S1,660 $680 $980 An impairment test...

The following scenario refers to questions 20-23 Colander Co is preparing its financial statements for the...

The following scenario refers to questions 20-23 Colander Co is preparing its financial statements for the year ended 31 December 2018 and has a number of issues to deal with regarding non-current assets. (1) Colander has suffered an impairment loss of €90,000 to one of its cash-generating units. The carrying amounts of the assets in the cash-generating unit prior to adjusting for impairment are: €'000 Goodwill 60 100 Land and buildings Plant and machinery 50 Net current assets 10 (2)...

The following scenario refers to questions 20-23 Colander Co is preparing its financial statements for the year ended 31 December 2018 and has a number of issues to deal with regarding non-current assets. (1) Colander has suffered an impairment loss of €90,000 to one of its cash-generating units. The carrying amounts of the assets in the cash-generating unit prior to adjusting for impairment are: €'000 Goodwill 60 100 Land and buildings Plant and machinery 50 Net current assets 10 (2)...

Tuesday, December 2018 REVIEW QUESTION 2 A cash generating unit (CGU) comprising a factory, plant and...

Tuesday, December 2018 REVIEW QUESTION 2 A cash generating unit (CGU) comprising a factory, plant and equipment etc and associated purchased goodwill becomes impaired because the product it makes is overtaken by a technologically more advanced model produced by a competitor. The recoverable amount of the cash generating unit falls to Tshs. 60m, resulting in an impairment loss of Tshs.80m, allocated as follows: CA before impairment CA after impairment Tshs. (m) Tshs. (m) Goodwill 10 Patent (with no market value)...

Tuesday, December 2018 REVIEW QUESTION 2 A cash generating unit (CGU) comprising a factory, plant and equipment etc and associated purchased goodwill becomes impaired because the product it makes is overtaken by a technologically more advanced model produced by a competitor. The recoverable amount of the cash generating unit falls to Tshs. 60m, resulting in an impairment loss of Tshs.80m, allocated as follows: CA before impairment CA after impairment Tshs. (m) Tshs. (m) Goodwill 10 Patent (with no market value)...

Header Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandaph Corporation purchased...

Header Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandaph Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $...

Header Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandaph Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $...

Header Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandach Corporation purchased...

Header Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandach Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $...

Header Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandach Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $...

How is this calculated step-by-step

The draft financial statements for Candelle plc for the year to December 31 2016 are being prepared and the accountant had asked your advice on the following issues. A. Candelle plc has an administration building which it no longer needs. On 1 July 2016 Candelle plc entered into an agreement to lease the building out to another company. The building cost 600,000 on 1 January 2007 and is being depreciated over 50 years, based on...

How is this calculated step-by-step

The draft financial statements for Candelle plc for the year to December 31 2016 are being prepared and the accountant had asked your advice on the following issues. A. Candelle plc has an administration building which it no longer needs. On 1 July 2016 Candelle plc entered into an agreement to lease the building out to another company. The building cost 600,000 on 1 January 2007 and is being depreciated over 50 years, based on...

a) At 31 December 2017, Senyum Sdn Bhd had a deferred tax liability of RM38,000. At 31 December 2018, the deferred tax liability is RM45,000. The company's 2018 current tax payable is RM50,000. Required: i) Compute the tax expense for Senyum Sdn Bhd for the year 2018. (5 marks) (CLO1:PLO1:C3) ii) Briefly explain what deferred tax is. (2 marks) (CLO1:PLO1:C1) b) Murni Berhad recognised a deferred tax liability for the year ended 31 March 2017 which was related solely to...

a) At 31 December 2017, Senyum Sdn Bhd had a deferred tax liability of RM38,000. At 31 December 2018, the deferred tax liability is RM45,000. The company's 2018 current tax payable is RM50,000. Required: i) Compute the tax expense for Senyum Sdn Bhd for the year 2018. (5 marks) (CLO1:PLO1:C3) ii) Briefly explain what deferred tax is. (2 marks) (CLO1:PLO1:C1) b) Murni Berhad recognised a deferred tax liability for the year ended 31 March 2017 which was related solely to...

Problem 1 The Faris Corporation has determined that there may be indicators of impairment for one of their assets - an office building that is currently leased out and a cash generating unit (CGU) representing a business unit. Data for the building and CGU follow. The year end is December 31, 20x4. Building Carrying value (20 years remaining, $500,000 residual value) Fair value Costs to sell Future cash flows generated by building (each year to the end of its useful...

Problem 1 The Faris Corporation has determined that there may be indicators of impairment for one of their assets - an office building that is currently leased out and a cash generating unit (CGU) representing a business unit. Data for the building and CGU follow. The year end is December 31, 20x4. Building Carrying value (20 years remaining, $500,000 residual value) Fair value Costs to sell Future cash flows generated by building (each year to the end of its useful...

This is BBM206/05 Business Accounting

II subject

Question 2 Kopi Sdn Bhd's statement of profit or loss for the year ended 31 December 2018 and statements of financial position at 31 December 2017 and 31 December 2018 were as following: STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED 31 DECEMBER 2018 RM'000 RM'000 Revenue 720 Raw materials consumed 70 Staff costs 94 Depreciation 118 Loss on disposal of non-current asset 18 Interest payable (28) Profit before tax Taxation (124)...

This is BBM206/05 Business Accounting

II subject

Question 2 Kopi Sdn Bhd's statement of profit or loss for the year ended 31 December 2018 and statements of financial position at 31 December 2017 and 31 December 2018 were as following: STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED 31 DECEMBER 2018 RM'000 RM'000 Revenue 720 Raw materials consumed 70 Staff costs 94 Depreciation 118 Loss on disposal of non-current asset 18 Interest payable (28) Profit before tax Taxation (124)...

Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandaph Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $ 75,000...

Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandaph Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $ 75,000...

Question #5-Asset Impairment: The recording unit of Turner Technologies Inc. (TTI) has been suffering a decline in its business, due to new product introductions by competitors. At 31 December 2018, the assets of the abrasives cash- generating unit are shown as follows (in millions) on the company's SFP: Cost Accumulated Net Book Depreciation Value S 470 Equipment (10-year life) Fixtures (10-year life) 950 480 430 340 90 120 Patent rights (40-year life) 280 160 S1,660 $680 $980 An impairment test...

Question #5-Asset Impairment: The recording unit of Turner Technologies Inc. (TTI) has been suffering a decline in its business, due to new product introductions by competitors. At 31 December 2018, the assets of the abrasives cash- generating unit are shown as follows (in millions) on the company's SFP: Cost Accumulated Net Book Depreciation Value S 470 Equipment (10-year life) Fixtures (10-year life) 950 480 430 340 90 120 Patent rights (40-year life) 280 160 S1,660 $680 $980 An impairment test...

The following scenario refers to questions 20-23 Colander Co is preparing its financial statements for the year ended 31 December 2018 and has a number of issues to deal with regarding non-current assets. (1) Colander has suffered an impairment loss of €90,000 to one of its cash-generating units. The carrying amounts of the assets in the cash-generating unit prior to adjusting for impairment are: €'000 Goodwill 60 100 Land and buildings Plant and machinery 50 Net current assets 10 (2)...

The following scenario refers to questions 20-23 Colander Co is preparing its financial statements for the year ended 31 December 2018 and has a number of issues to deal with regarding non-current assets. (1) Colander has suffered an impairment loss of €90,000 to one of its cash-generating units. The carrying amounts of the assets in the cash-generating unit prior to adjusting for impairment are: €'000 Goodwill 60 100 Land and buildings Plant and machinery 50 Net current assets 10 (2)...

Tuesday, December 2018 REVIEW QUESTION 2 A cash generating unit (CGU) comprising a factory, plant and equipment etc and associated purchased goodwill becomes impaired because the product it makes is overtaken by a technologically more advanced model produced by a competitor. The recoverable amount of the cash generating unit falls to Tshs. 60m, resulting in an impairment loss of Tshs.80m, allocated as follows: CA before impairment CA after impairment Tshs. (m) Tshs. (m) Goodwill 10 Patent (with no market value)...

Tuesday, December 2018 REVIEW QUESTION 2 A cash generating unit (CGU) comprising a factory, plant and equipment etc and associated purchased goodwill becomes impaired because the product it makes is overtaken by a technologically more advanced model produced by a competitor. The recoverable amount of the cash generating unit falls to Tshs. 60m, resulting in an impairment loss of Tshs.80m, allocated as follows: CA before impairment CA after impairment Tshs. (m) Tshs. (m) Goodwill 10 Patent (with no market value)...

Header Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandaph Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $...

Header Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandaph Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $...

Header Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandach Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $...

Header Q1. (25 marks) Calculation of and journal entries for impairment of goodwill Gandach Corporation purchased a division five years ago for $ 3 million. The division has been identified as a reporting unit that is cash-generating under IFRS. Management is reviewing the division for impairment of goodwill and has estimated the fair value of the reporting unit to be $ 3.2 million and the unit's value in use to be $ 3.3 million. In addition, there would be $...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago