Homework Answers

Add Answer to:

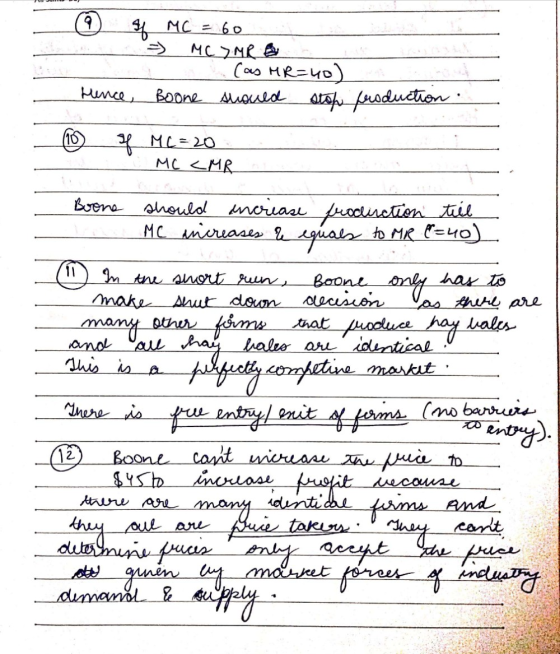

Boone's is a firm that produces hay bales. There are many other firms that produce hay...

need help with all of them Question 6 (1 point) In perfect competition, marginal revenue is the change in revenue from...

need help with all of them

Question 6 (1 point) In perfect competition, marginal revenue is the change in revenue from selling an additional unit of output the revenue in excess of what can be earned in the next-best alternative the last dollar needed to make zero economic profit the extra revenue generated by a $1 change in price the last dollar needed to make maximum profit Question 7 (1 point) In which of the following situations should a profit-maximizing...

need help with all of them

Question 6 (1 point) In perfect competition, marginal revenue is the change in revenue from selling an additional unit of output the revenue in excess of what can be earned in the next-best alternative the last dollar needed to make zero economic profit the extra revenue generated by a $1 change in price the last dollar needed to make maximum profit Question 7 (1 point) In which of the following situations should a profit-maximizing...

Suppose the bobby pin industry is perfectly competitive. The price of a packet of bobby pins...

Suppose the bobby pin industry is perfectly competitive. The price of a packet of bobby pins is $2.00. Pins and Needles, Inc. is a firm in this industry and is producing 1,000 packets of bobby pins per day at the point where the MC = MR. The average cost of production at this output level is $1.50 per packet. a. What is the marginal cost of the 1,000th packet? b. Is this firm making an economic profit, zero economic profit,...

|M4 Questions of the Week 1. Hayfever Farms is an 80-acre hay farm in Colorado. Due...

|M4 Questions of the Week 1. Hayfever Farms is an 80-acre hay farm in Colorado. Due to the legalization of marijuana in the state, the owners of the farm are considering changing the farm's name to Blissful Acres and growing marijuana instead of hay. Use the information presented in the table to answer three questions. Number of acres 10 20 30 40 50 60 70 80 MC$ 320 200 540 730 1,200 3,200 5,600 6,700 MR (hay) 730 730 730...

|M4 Questions of the Week 1. Hayfever Farms is an 80-acre hay farm in Colorado. Due to the legalization of marijuana in the state, the owners of the farm are considering changing the farm's name to Blissful Acres and growing marijuana instead of hay. Use the information presented in the table to answer three questions. Number of acres 10 20 30 40 50 60 70 80 MC$ 320 200 540 730 1,200 3,200 5,600 6,700 MR (hay) 730 730 730...

QUESTION ONE A. Suppose the marginal cost and marginal revenue (in ¢000) for a product produced...

QUESTION ONE A. Suppose the marginal cost and marginal revenue (in ¢000) for a product produced by a company is estimated to be MC = q +35 MR = 560 + 22q-q? Where q is the quantity produced and the firm's break-even is 5 units per week You are Required to 1. determine the total cost and the total revenue function in terms of q. (6 marks) II. estimate the output at which profit is maximize (6 marks) III. calculate...

QUESTION ONE A. Suppose the marginal cost and marginal revenue (in ¢000) for a product produced by a company is estimated to be MC = q +35 MR = 560 + 22q-q? Where q is the quantity produced and the firm's break-even is 5 units per week You are Required to 1. determine the total cost and the total revenue function in terms of q. (6 marks) II. estimate the output at which profit is maximize (6 marks) III. calculate...

Consider a perfectly competitive market with many identical firms. Each firm has a long-run marginal cost...

Consider a perfectly competitive market with many identical firms. Each firm has a long-run marginal cost function given by LRMC(y) = y ^2 + 1. We do not know the firms’ LRAT C function, but we know that at a quantity of 3 it is equal to LRMC. In other words: LRAT C(3) = LRMC(3). (a) Find an expression for an individual firm’s long-run inverse supply curve: this will be p as a function of y. Note that it will...

The following table represents a certain production function of what a certain facility can produce in...

The following table represents a certain production function of what a certain facility can produce in one day. Assume the firm has a fixed amount of physical capital that they rent for $500 a day. We will use this example to review CH. 7. [probably easiest to copy and paste the table and question parts into the submission box and then add your response. Make your text a different color for ease of viewing] L Q MPL FC VC TC AFC...

2. Consider an economy with many identical firms. Each firm produces according to a Cobb- Douglas...

2. Consider an economy with many identical firms. Each firm produces according to a Cobb- Douglas production function: y = AK α N 1−α where y is output, K is the amount of capital, N is the amount of labor and 0<α <1 is a parameter. (a) What is the marginal product of labor (MPN)? (Take a partial derivative with respect to N ) (b) What is the marginal product of labor when A = K = 1 , N...

23. A competitive firm can sell its product for a price of $3 in the market...

23. A competitive firm can sell its product for a price of $3 in the market (there is a reason the word competitive is underlined and in bold!). Total costs are given below. Fill in the following columns in the table: price, total revenue, marginal revenue, marginal costs, variable costs, fixed costs, profit, and average total cost. (Hint if you get stuck: what are variable costs at a quantity of 0? Therefore, what are fixed costs?). Quantity Price TR MR ...

2. Suppose the firm has the one variable production function Q=L?. Assume that the wage rate...

2. Suppose the firm has the one variable production function Q=L?. Assume that the wage rate is w= 20 and that the firm has fixed costs of 10. Finally, assume that the firm is a price taker and the market price is 2. a) Show that this production function exhibits increasing returns to scale. Show that the marginal product of labor is increasing. Illustrate the production function. Is it convex, concave or neither? b) Find the variable and total cost...

2. Suppose the firm has the one variable production function Q=L?. Assume that the wage rate is w= 20 and that the firm has fixed costs of 10. Finally, assume that the firm is a price taker and the market price is 2. a) Show that this production function exhibits increasing returns to scale. Show that the marginal product of labor is increasing. Illustrate the production function. Is it convex, concave or neither? b) Find the variable and total cost...

You are the manager of a firm that produces output in two plants. The demand for...

You are the manager of a firm that produces output in two plants. The demand for your firm's product is P = 120 - 6Q, where Q = Q 1 + Q 2. The marginal cost associated with producing in the two plants are MC 1 = 2Q 1 and MC 2 = 4Q 2. What price should be charged in order to maximize revenues? Please document each step

need help with all of them

Question 6 (1 point) In perfect competition, marginal revenue is the change in revenue from selling an additional unit of output the revenue in excess of what can be earned in the next-best alternative the last dollar needed to make zero economic profit the extra revenue generated by a $1 change in price the last dollar needed to make maximum profit Question 7 (1 point) In which of the following situations should a profit-maximizing...

need help with all of them

Question 6 (1 point) In perfect competition, marginal revenue is the change in revenue from selling an additional unit of output the revenue in excess of what can be earned in the next-best alternative the last dollar needed to make zero economic profit the extra revenue generated by a $1 change in price the last dollar needed to make maximum profit Question 7 (1 point) In which of the following situations should a profit-maximizing...

|M4 Questions of the Week 1. Hayfever Farms is an 80-acre hay farm in Colorado. Due to the legalization of marijuana in the state, the owners of the farm are considering changing the farm's name to Blissful Acres and growing marijuana instead of hay. Use the information presented in the table to answer three questions. Number of acres 10 20 30 40 50 60 70 80 MC$ 320 200 540 730 1,200 3,200 5,600 6,700 MR (hay) 730 730 730...

|M4 Questions of the Week 1. Hayfever Farms is an 80-acre hay farm in Colorado. Due to the legalization of marijuana in the state, the owners of the farm are considering changing the farm's name to Blissful Acres and growing marijuana instead of hay. Use the information presented in the table to answer three questions. Number of acres 10 20 30 40 50 60 70 80 MC$ 320 200 540 730 1,200 3,200 5,600 6,700 MR (hay) 730 730 730...

QUESTION ONE A. Suppose the marginal cost and marginal revenue (in ¢000) for a product produced by a company is estimated to be MC = q +35 MR = 560 + 22q-q? Where q is the quantity produced and the firm's break-even is 5 units per week You are Required to 1. determine the total cost and the total revenue function in terms of q. (6 marks) II. estimate the output at which profit is maximize (6 marks) III. calculate...

QUESTION ONE A. Suppose the marginal cost and marginal revenue (in ¢000) for a product produced by a company is estimated to be MC = q +35 MR = 560 + 22q-q? Where q is the quantity produced and the firm's break-even is 5 units per week You are Required to 1. determine the total cost and the total revenue function in terms of q. (6 marks) II. estimate the output at which profit is maximize (6 marks) III. calculate...

2. Suppose the firm has the one variable production function Q=L?. Assume that the wage rate is w= 20 and that the firm has fixed costs of 10. Finally, assume that the firm is a price taker and the market price is 2. a) Show that this production function exhibits increasing returns to scale. Show that the marginal product of labor is increasing. Illustrate the production function. Is it convex, concave or neither? b) Find the variable and total cost...

2. Suppose the firm has the one variable production function Q=L?. Assume that the wage rate is w= 20 and that the firm has fixed costs of 10. Finally, assume that the firm is a price taker and the market price is 2. a) Show that this production function exhibits increasing returns to scale. Show that the marginal product of labor is increasing. Illustrate the production function. Is it convex, concave or neither? b) Find the variable and total cost...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago