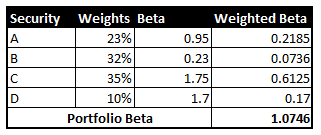

Based on the data below, what is the portfolio beta? (format xx.xx as needed) Weight: A...

Based on the data below, what is the portfolio beta? (format xx.xx as needed)

Weight:

A 23.00%

B 32.00%

C 35.00%

D 10.00%

Beta (b)

A 0.95

B 0.23

C 1.75

D 1.70

Homework Answers

Portolio Beta = Wtd avg beta of securities in that portolio

Pls comment, if any further assistance is required

Add Answer to:

Based on the data below, what is the portfolio beta? (format

xx.xx as needed)

Weight:

A...

1. A portfolio contains 3 stocks as outlined below. What is the beta of the portfolio?...

1. A portfolio contains 3 stocks as outlined below. What is the beta of the portfolio? Stock Weight Beta A 70% 0.77 B 10% 1.17 C 20% 1.77 A. 1.24 B. 1.10 C. 1.07 D. 1.01 2. Two stocks have the following returns. What is their correlation? Year Stock A Stock B 2010 8.00% -8.00% 2011 9.00% -9.00% 2012 10.00% -10.00% 2013 12.00% -12.00% 2014 14.00% -14.00% 2015 16.00% -16.00% A. -1.00 B. 1.00 C. 0.00 D. -.23

Create a portfolio using the four stocks and information below: Stock A Stock B Stock C...

Create a portfolio using the four stocks and information below: Stock A Stock B Stock C Stock D Expected Return 31.00% 13.00% 32.00% 11.00% Standard Deviation 35.00% 31.00% 11.00% 29.00% Weight in Portfolio 11 .00% 28.00% 10.00% 51.00% Correlation (A,B) Correlation (A,C) Correlation (A,D) Correlation (B,C) Correlation (B,D) Correlation (C,D) 0.0100 0.0700 0.9400 0.2500 0.1900 0.8600

Create a portfolio using the four stocks and information below: Stock A Stock B Stock C Stock D Expected Return 31.00% 13.00% 32.00% 11.00% Standard Deviation 35.00% 31.00% 11.00% 29.00% Weight in Portfolio 11 .00% 28.00% 10.00% 51.00% Correlation (A,B) Correlation (A,C) Correlation (A,D) Correlation (B,C) Correlation (B,D) Correlation (C,D) 0.0100 0.0700 0.9400 0.2500 0.1900 0.8600

What is the beta of a 5-asset portfolio consisting of the following? Stock Weight Beta Tesla...

What is the beta of a 5-asset portfolio consisting of the following? Stock Weight Beta Tesla 0.23 1.55 Apple 0.19 1.66 ATT 0.38 1.23 Google 0.15 0.98 Adobe 0.05 0.11

Based on this portfolio what is the portfolios beta? Portfolio standard deviation? And portfolios expected return?...

Based on this portfolio what is the portfolios beta? Portfolio standard deviation? And portfolios expected return? Beta Expected Rate of Return (CAPM) Portfolio Weight SPY 1 9.00% 0.2 LQD -0.02 0.59% 0.05 HYG 0.38 3.89% 0.15 IBM 0.86 7.85% 0.1 KO 0.66 6.20% 0.2 BIG 1.04 9.33% 0.1 NFLX 1.57 13.70% 0.2 What is the Portfolio Beta? And formula to calculate it? What is the Portfolio Standard Deviation and formula to find it? Portfolio Expected Return? And formula to calculate...

A portfolio is comprised of the following stocks. What is the portfolio beta? Stock Market Value...

A portfolio is comprised of the following stocks. What is the portfolio beta? Stock Market Value of Shares Beta A $ 14,000 1.79 B $ 17,500 .98 C $ 8,600 1.16 1.18 1.45 1.30 1.37 You own a $25,000 portfolio that is invested in a risk-free security and Stock A. The beta of Stock A is 1.70 and the portfolio beta is .95. What is the amount of the investment in Stock A? $14,791 $11,331 $13,971 $16,531

8. What is the portfolio weight of Microsoft (MSFT)? US Airways (AAL)? Beta Number of Shares...

8. What is the portfolio weight of Microsoft (MSFT)? US Airways (AAL)? Beta Number of Shares 750 220 460 Stock Price S33 $20 $30 Stock Microsoft US Airwa 1.35 0.57 1.21 Citi A. wmT 52.4%, WAAL-15.4% B. Wmsft-39.8%, WAAL-10.2% C. Wmsft-57.6%, WAAL-10.2% D. wrnsft-39.8%, WAAL-15.4% E. Wmsft-59.1%, wAAL-12.9% 9. What is the beta of this portfolio (given in the previous question)? A. 1.18 B. 1.22 C. 1.31 D. 1.27 E. 1.12

8. What is the portfolio weight of Microsoft (MSFT)? US Airways (AAL)? Beta Number of Shares 750 220 460 Stock Price S33 $20 $30 Stock Microsoft US Airwa 1.35 0.57 1.21 Citi A. wmT 52.4%, WAAL-15.4% B. Wmsft-39.8%, WAAL-10.2% C. Wmsft-57.6%, WAAL-10.2% D. wrnsft-39.8%, WAAL-15.4% E. Wmsft-59.1%, wAAL-12.9% 9. What is the beta of this portfolio (given in the previous question)? A. 1.18 B. 1.22 C. 1.31 D. 1.27 E. 1.12

Rene owns the following portfolio of securities. What is the beta for the portfolio? Company Beta...

Rene owns the following portfolio of securities. What is the beta for the portfolio? Company Beta Percent of Portfolio Microsoft 1.82 50% GM 0.53 30% Dullco 0.67 20% A) 1.20 B) 1.50 C) 1.74 D) 1.98 PLEASE SHOW WORK !

b) calculate the standard deviation of the portfolio. c) calculate the beta of the portfolio. d)...

b) calculate the standard deviation of the portfolio.

c) calculate the beta of the portfolio.

d) is the systematic risk of the portfolio is more or less than

the market?

Question 7 (15 pts): retums for There are three states of economy and you are given the following probabilities and each stock for each state of economy. You invest 30% in stock X and 70% in stock Y. The betas for cach stock are also given below Returns if State...

b) calculate the standard deviation of the portfolio.

c) calculate the beta of the portfolio.

d) is the systematic risk of the portfolio is more or less than

the market?

Question 7 (15 pts): retums for There are three states of economy and you are given the following probabilities and each stock for each state of economy. You invest 30% in stock X and 70% in stock Y. The betas for cach stock are also given below Returns if State...

What is the Treynor ratio of a portfolio comprised of 40 percent portfolio A, 25 percent...

What is the Treynor ratio of a portfolio comprised of 40 percent portfolio A, 25 percent portfolio B, and 35 percent portfolio C? Asset Weight Avg Return Std Dev Beta A 40 % 15.30 % 17.20 % 1.56 B 25 % 10.50 % 9.80 % 0.95 C 35 % 13.30 % 14.10 % 1.25 The risk-free rate is 2.9 percent and the market risk premium is 8.6 percent. Multiple Choice 0.070 0.102 0.054 0.062 0.081

What is the Treynor ratio of a portfolio comprised of 40 percent portfolio A, 25 percent...

What is the Treynor ratio of a portfolio comprised of 40 percent portfolio A, 25 percent portfolio B, and The risk-free rate is 2.5 percent and the market risk premium is 8.4 percent. Asset Weight Avg Return Std Dev Beta A 40 % 15.30 % 17.20 % 1.25 B 25 % 10.50 % 9.80 % 1.3 C 35 % 13.30 % 14.10 % 0.95 Group of answer choices 0.094 0.057 0.081 0.076 0.063

Create a portfolio using the four stocks and information below: Stock A Stock B Stock C Stock D Expected Return 31.00% 13.00% 32.00% 11.00% Standard Deviation 35.00% 31.00% 11.00% 29.00% Weight in Portfolio 11 .00% 28.00% 10.00% 51.00% Correlation (A,B) Correlation (A,C) Correlation (A,D) Correlation (B,C) Correlation (B,D) Correlation (C,D) 0.0100 0.0700 0.9400 0.2500 0.1900 0.8600

Create a portfolio using the four stocks and information below: Stock A Stock B Stock C Stock D Expected Return 31.00% 13.00% 32.00% 11.00% Standard Deviation 35.00% 31.00% 11.00% 29.00% Weight in Portfolio 11 .00% 28.00% 10.00% 51.00% Correlation (A,B) Correlation (A,C) Correlation (A,D) Correlation (B,C) Correlation (B,D) Correlation (C,D) 0.0100 0.0700 0.9400 0.2500 0.1900 0.8600

8. What is the portfolio weight of Microsoft (MSFT)? US Airways (AAL)? Beta Number of Shares 750 220 460 Stock Price S33 $20 $30 Stock Microsoft US Airwa 1.35 0.57 1.21 Citi A. wmT 52.4%, WAAL-15.4% B. Wmsft-39.8%, WAAL-10.2% C. Wmsft-57.6%, WAAL-10.2% D. wrnsft-39.8%, WAAL-15.4% E. Wmsft-59.1%, wAAL-12.9% 9. What is the beta of this portfolio (given in the previous question)? A. 1.18 B. 1.22 C. 1.31 D. 1.27 E. 1.12

8. What is the portfolio weight of Microsoft (MSFT)? US Airways (AAL)? Beta Number of Shares 750 220 460 Stock Price S33 $20 $30 Stock Microsoft US Airwa 1.35 0.57 1.21 Citi A. wmT 52.4%, WAAL-15.4% B. Wmsft-39.8%, WAAL-10.2% C. Wmsft-57.6%, WAAL-10.2% D. wrnsft-39.8%, WAAL-15.4% E. Wmsft-59.1%, wAAL-12.9% 9. What is the beta of this portfolio (given in the previous question)? A. 1.18 B. 1.22 C. 1.31 D. 1.27 E. 1.12

b) calculate the standard deviation of the portfolio.

c) calculate the beta of the portfolio.

d) is the systematic risk of the portfolio is more or less than

the market?

Question 7 (15 pts): retums for There are three states of economy and you are given the following probabilities and each stock for each state of economy. You invest 30% in stock X and 70% in stock Y. The betas for cach stock are also given below Returns if State...

b) calculate the standard deviation of the portfolio.

c) calculate the beta of the portfolio.

d) is the systematic risk of the portfolio is more or less than

the market?

Question 7 (15 pts): retums for There are three states of economy and you are given the following probabilities and each stock for each state of economy. You invest 30% in stock X and 70% in stock Y. The betas for cach stock are also given below Returns if State...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago