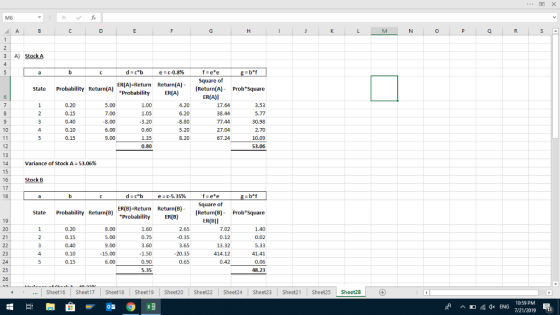

A) What is the variance of each stock?

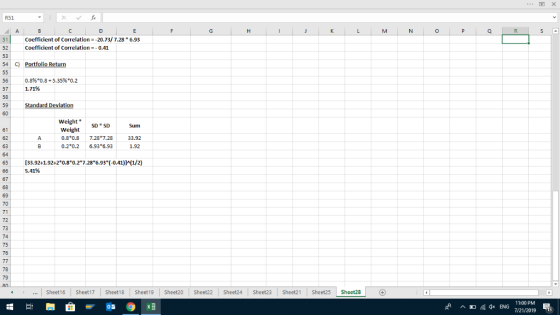

B) What is the coefficient of correlation between stock A and B?

C) If you invest 80% of your money in A and 20% in B, what would be your portfolio's expected rate of return and standard deviation?

Homework Answers

Add Answer to:

A) What is the variance of each stock?

B) What is the coefficient of correlation between...

Probability of State of Economy State of Economy Return of Stock A Return of Stock B...

Probability of State of Economy State of Economy Return of Stock A Return of Stock B 0.20 Bear 0.05 -0.05 0.40 Normal 0.07 0.10 0.40 Bull 0.10 0.20 A) Calculate the expected return for each stock. B) What is the correlation between the returns of the two stocks? C) Assume the market has an expected return of 10% and a standard deviation of 20%. Also, ρB,M = 0.8. Calculate Beta for Stock B.

find the expected return of a stock if the correlation coefficient between the stock return and...

find the expected return of a stock if the correlation coefficient between the stock return and market return is .678, the variance of the stocks returns is .0456, the variance of markets return is .0567. assume a risk free rate of 2% and a market risk premium of 11%

6. Calculating a beta coefficient for a single stock Suppose that the standard deviation of returns...

6. Calculating a beta coefficient for a single stock Suppose that the standard deviation of returns for a single stock A IS A = 25%, and the standard deviation of the market return is on = 15%. If the correlation between stock A and the market is PAM - 0.6, then the stock's beta is prns against the market returns will equal the true value of Is it reasonable to expect that the beta value estimated via the regression of...

6. Calculating a beta coefficient for a single stock Suppose that the standard deviation of returns for a single stock A IS A = 25%, and the standard deviation of the market return is on = 15%. If the correlation between stock A and the market is PAM - 0.6, then the stock's beta is prns against the market returns will equal the true value of Is it reasonable to expect that the beta value estimated via the regression of...

Use the following yearly rate of return valoes for Questions 1, 2, 3, and4. Market Risk-frre...

Use the following yearly rate of return valoes for Questions 1, 2, 3, and4. Market Risk-frre Year Stock A Stock B Stock C retura return 2008 9.0% 8.0% 11.0% 10.0% 1.0% 2009 10.0% 11.0% 3.0% 9.0% 10% 2010 -3.0% 6.0% -6.0% 8.0% 10% 2011 -3.0% -110% -11.0% -15.0% 1.0n% 2012 9.0 % 3.0% 6.% 6.0% 10% 2013 -8.0% -4.0% -2.0% 20% 10% 2014 11.0% 15.% 13.0% 6.0% 10% -2.0% 10% 2015 -9.0% -5.0% -5.0% 2016 3.0% 1.0% 10.0% 14.0% 14.0%...

Use the following yearly rate of return valoes for Questions 1, 2, 3, and4. Market Risk-frre Year Stock A Stock B Stock C retura return 2008 9.0% 8.0% 11.0% 10.0% 1.0% 2009 10.0% 11.0% 3.0% 9.0% 10% 2010 -3.0% 6.0% -6.0% 8.0% 10% 2011 -3.0% -110% -11.0% -15.0% 1.0n% 2012 9.0 % 3.0% 6.% 6.0% 10% 2013 -8.0% -4.0% -2.0% 20% 10% 2014 11.0% 15.% 13.0% 6.0% 10% -2.0% 10% 2015 -9.0% -5.0% -5.0% 2016 3.0% 1.0% 10.0% 14.0% 14.0%...

step by step solutions please. no excel solutions 1. Consider the following probability distribution for stocks...

step by step solutions please. no excel solutions

1. Consider the following probability distribution for stocks A and B: (Hint: Use five decimal places for the numbers in your calculations.) B Returns - 2 % A Returns 12% Probability 0.30 State Boom 2% 8% 0.60 Normal 6% 4% 0.10 Bust What are the expected rates of return for stocks A and B? b. What are the variances for A and B? a. c. What are the standard deviations for A...

step by step solutions please. no excel solutions

1. Consider the following probability distribution for stocks A and B: (Hint: Use five decimal places for the numbers in your calculations.) B Returns - 2 % A Returns 12% Probability 0.30 State Boom 2% 8% 0.60 Normal 6% 4% 0.10 Bust What are the expected rates of return for stocks A and B? b. What are the variances for A and B? a. c. What are the standard deviations for A...

Using the data in the following table, calculate: A. Average return and standard deviation for each...

Using the data in the following table, calculate: A. Average return and standard deviation for each stock B. Covariance between the stocks C. Correlation between the stocks D. Compute average return and standard deviation of the portfolio that maintains a 50% weight in Stock A and 50% in stock B Year 2010 2011 2012 2013 2014 2015 Stock A -10.0% 20.0% 5.0% -5.0% 2.0% 9.0% Stock B 21.0% 7.0% 30.0% -3.0% -8.0% 25.0%

Rate of Return if State Occurs State of Economy Probability Stock A Stock B Stock C...

Rate of Return if State Occurs State of Economy Probability Stock A Stock B Stock C Boom 0.15 0.30 0.45 0.33 Good 0.45 0.12 0.10 0.15 Poor 0.35 0.01 -0.15 -0.05 Bust 0.05 -0.20 -0.30 -0.09 Your portfolio is invested 30% each in A and C and 40% in B. What is the expected return of the portfolio? What is the variance of this portfolio? The standard deviation?

a. If Mary invests half her money in each of the two commonstocks, what is the portfolio's expected rate of return and...

a. If Mary invests half her money in each of the two

commonstocks, what is the portfolio's expected rate of return and

standard deviation in portfolio return?

b. Answer part a where the correlation between the two common

stock investments is equal to zero.

c. Answer part a where the correlation between the two common

stock investments is equal to plus+1.

d. Answer part a where the correlation between the two common

stock investments is equal to minus−1.

e. Using...

a. If Mary invests half her money in each of the two

commonstocks, what is the portfolio's expected rate of return and

standard deviation in portfolio return?

b. Answer part a where the correlation between the two common

stock investments is equal to zero.

c. Answer part a where the correlation between the two common

stock investments is equal to plus+1.

d. Answer part a where the correlation between the two common

stock investments is equal to minus−1.

e. Using...

a. If Mary invests half her money in each of the two common stocks, what is...

a. If Mary invests half her money in each of the two common

stocks, what is the portfolio's expected rate of return and

standard deviation in portfolio return?

b. Answer part a where the correlation between the two common

stock investments is equal to zero.

c. Answer part a where the correlation between the two common

stock investments is equal to +1

d. Answer part a where the correlation between the two common

stock investments is equal to -1

e....

a. If Mary invests half her money in each of the two common

stocks, what is the portfolio's expected rate of return and

standard deviation in portfolio return?

b. Answer part a where the correlation between the two common

stock investments is equal to zero.

c. Answer part a where the correlation between the two common

stock investments is equal to +1

d. Answer part a where the correlation between the two common

stock investments is equal to -1

e....

Assume an investment manager is considering to invest in a portfolio composed of Stock (A) and Stock (B). Stock (A) has an expected return of 10% and a Variance of 100 (Standard Deviation=10), while Stock (B) has an expected return of

Assume an investment manager is considering to invest in a portfolio composed of Stock (A) and Stock (B). Stock (A) has an expected return of 10% and a Variance of 100 (Standard Deviation=10), while Stock (B) has an expected return of 20% and a Variance of 900 (Standard deviation=30).1- Calculate the expected return and variance of the portfolio if the proportion invested in Sock (A) is (0, .2, .3,.5. .6,.7,1) .The Correlation Coefficient is .4.2- If the Correlation Coefficient is...

6. Calculating a beta coefficient for a single stock Suppose that the standard deviation of returns for a single stock A IS A = 25%, and the standard deviation of the market return is on = 15%. If the correlation between stock A and the market is PAM - 0.6, then the stock's beta is prns against the market returns will equal the true value of Is it reasonable to expect that the beta value estimated via the regression of...

6. Calculating a beta coefficient for a single stock Suppose that the standard deviation of returns for a single stock A IS A = 25%, and the standard deviation of the market return is on = 15%. If the correlation between stock A and the market is PAM - 0.6, then the stock's beta is prns against the market returns will equal the true value of Is it reasonable to expect that the beta value estimated via the regression of...

Use the following yearly rate of return valoes for Questions 1, 2, 3, and4. Market Risk-frre Year Stock A Stock B Stock C retura return 2008 9.0% 8.0% 11.0% 10.0% 1.0% 2009 10.0% 11.0% 3.0% 9.0% 10% 2010 -3.0% 6.0% -6.0% 8.0% 10% 2011 -3.0% -110% -11.0% -15.0% 1.0n% 2012 9.0 % 3.0% 6.% 6.0% 10% 2013 -8.0% -4.0% -2.0% 20% 10% 2014 11.0% 15.% 13.0% 6.0% 10% -2.0% 10% 2015 -9.0% -5.0% -5.0% 2016 3.0% 1.0% 10.0% 14.0% 14.0%...

Use the following yearly rate of return valoes for Questions 1, 2, 3, and4. Market Risk-frre Year Stock A Stock B Stock C retura return 2008 9.0% 8.0% 11.0% 10.0% 1.0% 2009 10.0% 11.0% 3.0% 9.0% 10% 2010 -3.0% 6.0% -6.0% 8.0% 10% 2011 -3.0% -110% -11.0% -15.0% 1.0n% 2012 9.0 % 3.0% 6.% 6.0% 10% 2013 -8.0% -4.0% -2.0% 20% 10% 2014 11.0% 15.% 13.0% 6.0% 10% -2.0% 10% 2015 -9.0% -5.0% -5.0% 2016 3.0% 1.0% 10.0% 14.0% 14.0%...

step by step solutions please. no excel solutions

1. Consider the following probability distribution for stocks A and B: (Hint: Use five decimal places for the numbers in your calculations.) B Returns - 2 % A Returns 12% Probability 0.30 State Boom 2% 8% 0.60 Normal 6% 4% 0.10 Bust What are the expected rates of return for stocks A and B? b. What are the variances for A and B? a. c. What are the standard deviations for A...

step by step solutions please. no excel solutions

1. Consider the following probability distribution for stocks A and B: (Hint: Use five decimal places for the numbers in your calculations.) B Returns - 2 % A Returns 12% Probability 0.30 State Boom 2% 8% 0.60 Normal 6% 4% 0.10 Bust What are the expected rates of return for stocks A and B? b. What are the variances for A and B? a. c. What are the standard deviations for A...

a. If Mary invests half her money in each of the two

commonstocks, what is the portfolio's expected rate of return and

standard deviation in portfolio return?

b. Answer part a where the correlation between the two common

stock investments is equal to zero.

c. Answer part a where the correlation between the two common

stock investments is equal to plus+1.

d. Answer part a where the correlation between the two common

stock investments is equal to minus−1.

e. Using...

a. If Mary invests half her money in each of the two

commonstocks, what is the portfolio's expected rate of return and

standard deviation in portfolio return?

b. Answer part a where the correlation between the two common

stock investments is equal to zero.

c. Answer part a where the correlation between the two common

stock investments is equal to plus+1.

d. Answer part a where the correlation between the two common

stock investments is equal to minus−1.

e. Using...

a. If Mary invests half her money in each of the two common

stocks, what is the portfolio's expected rate of return and

standard deviation in portfolio return?

b. Answer part a where the correlation between the two common

stock investments is equal to zero.

c. Answer part a where the correlation between the two common

stock investments is equal to +1

d. Answer part a where the correlation between the two common

stock investments is equal to -1

e....

a. If Mary invests half her money in each of the two common

stocks, what is the portfolio's expected rate of return and

standard deviation in portfolio return?

b. Answer part a where the correlation between the two common

stock investments is equal to zero.

c. Answer part a where the correlation between the two common

stock investments is equal to +1

d. Answer part a where the correlation between the two common

stock investments is equal to -1

e....

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago