Two firms produce the same product in a local market where the demand of product is...

Two firms produce the same product in a local market where the demand of product is P = 780−2Q - P is the price of the product and Q is the total amount of product produced by these two firms. Each firm needs to decide the quantity that they are going to produce given the local demand, and the cost of producing one unit is $1.

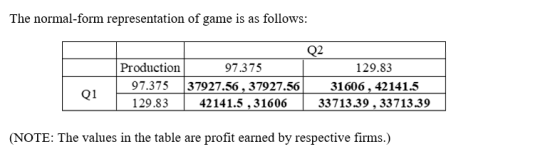

Write down the normal-form representation of the game.

Homework Answers

Add Answer to:

Two firms produce the same product in a local market where the

demand of product is...

The market demand curve for mineral water is P=15-Q. Suppose that there are two firms that...

The market demand curve for mineral water is P=15-Q. Suppose that there are two firms that produce mineral water, each with a constant marginal cost of 3 dollars per unit. Suppose that both firms make their production decisions simultaneously. How much each firm should produce to maximize its profit? Calculate the market price. The quantity produced by firm 1 is denoted by Q1 The quantity produced by firm 2 is denoted by Q2. The total quantity produced in the market...

Consider a market where N firms produce a homogeneous product and compete by simultaneously setting quantities....

Consider a market where N firms produce a homogeneous product and compete by simultaneously setting quantities. The inverse demand function has the general form P PO-P(qi +q2 +q3 + + qv), where Q is total quantity produced, qi is the quantity produced by firm i and P is the market price. The demand curve is downward sloping, so P10 < 0. The total cost of firm i is given by Cig). (0) Show that P- MC qi i , where...

Consider a market where N firms produce a homogeneous product and compete by simultaneously setting quantities. The inverse demand function has the general form P PO-P(qi +q2 +q3 + + qv), where Q is total quantity produced, qi is the quantity produced by firm i and P is the market price. The demand curve is downward sloping, so P10 < 0. The total cost of firm i is given by Cig). (0) Show that P- MC qi i , where...

Suppose that the (inverse) market demand function for wax paper is P=400-2Q where Q is total...

Suppose that the (inverse) market demand function for wax paper is P=400-2Q where Q is total industry output. There are only two firms, Firm1 and Firm 2, that produce wax paper. Thus, Q=q1+q2. Each firm has no fixed cost but a constant marginal cost of production equals $40. (a) Suppose that the two firms decide to form a cartel. Calculate the output quantity for Firm 1 (b) Suppose that the two firms decide to form a cartel. Calculate the profit...

please explain all details. Market demand curve for a good produced only by two firms is...

please explain all details.

Market demand curve for a good produced only by two

firms is given by P= 70- 20. Both firms produce with constant and

identical marginal cost of 3. 10, that is MC, = MC, = 10.

(P,Q.4-42,) in Cournot equilibrium. a) Find b) Find (P,Q,q1,92,,,

2) in Stackelberg equilibrium with Firm 1 acting as the leader. c)

Compare your findings with monopoly and competitive equilibria.

Market demand curve for a good produced only by two firms...

please explain all details.

Market demand curve for a good produced only by two

firms is given by P= 70- 20. Both firms produce with constant and

identical marginal cost of 3. 10, that is MC, = MC, = 10.

(P,Q.4-42,) in Cournot equilibrium. a) Find b) Find (P,Q,q1,92,,,

2) in Stackelberg equilibrium with Firm 1 acting as the leader. c)

Compare your findings with monopoly and competitive equilibria.

Market demand curve for a good produced only by two firms...

Question 2: Simultaneous quantity choiceTwo firms F1 and F2 produce a homogeneous product and compete on...

Question 2: Simultaneous quantity choiceTwo firms F1 and F2 produce a homogeneous product and compete on the same market. The market price is described by the inverse demand curveP= 11−2Q, where Q is total industry output andPis the market price. To keep things simple, suppose that each firm can produce either 1 or 2 units (these are the only possible choices of production).Further suppose that both firms have a constant marginal cost equal to 2, so that the total cost...

In a monopolistic competitive market for blood pressure monitor, suppose the market demand function for the monitor is P=160 – 3Q, where P is the price for monitor, Q and the quantity of monitor dema...

In a monopolistic competitive market for blood pressure monitor, suppose the market demand function for the monitor is P=160 – 3Q, where P is the price for monitor, Q and the quantity of monitor demanded. Marginal cost of producing it is MC: P = 20 + Q, where P is the price of the monitor and Q is the quantity of the monitor sold. Use the Twice as Steep Rule, form the marginal revenue function. What are the price and...

2. Two firms produce homogeneous products. Market demand is given by Q = 40-P, and each firm face...

2. Two firms produce homogeneous products. Market demand is given by Q = 40-P, and each firm faces a marginal cost of production of 4 per unit The timing of the game is as follows. In Period 1, firm 1 chooses the quantity q it will sell. In Period 2, firm 2 (who observed firm 1s choice in period 1) chooses whether or not to enter the market. If firm 2 chooses to enter it must pay an entry fee...

2. Two firms produce homogeneous products. Market demand is given by Q = 40-P, and each firm faces a marginal cost of production of 4 per unit The timing of the game is as follows. In Period 1, firm 1 chooses the quantity q it will sell. In Period 2, firm 2 (who observed firm 1s choice in period 1) chooses whether or not to enter the market. If firm 2 chooses to enter it must pay an entry fee...

imagine a market comprising two competing firms 1&2 which produce an identical product . the inverse...

imagine a market comprising two competing firms 1&2 which produce an identical product . the inverse demand function of the latter is p = 102 – Q, where Q = Q1 + Q2 , Qi = output of firm I (i=1,2) lastly , the cost of production equals TC(Qi)= 2 Qi . if the two firms choose Qi simultaneously , and only once , with a view to maximize their respective profit , find the nash equilibrium (Firm 1, firm...

1) Demand in a market is given by Q=9p-7.3 where p is the market price. What...

1) Demand in a market is given by Q=9p-7.3 where p is the market price. What is the elasticity of demand? Include the negative sign if necessary. 2) Demand in a market is given by Q=3p-3 where p is the market price. There are 18 identical firms in the market. What is the elasticity of the residual demand faced by each firm when the elasticity of supply of the other firms is 2.6? 3) Inverse demand in a market is...

Suppose there are two firms operating in a market. The firms produce identical products, and the...

Suppose there are two firms operating in a market. The firms produce identical products, and the total cost for each firm is given by C = 8qi, i = 1,2, where qi is the quantity of output produced by firm i. Therefore the marginal cost for each firm is constant at MC = 8. Also, the market demand is given by P = 56 –4Q, where Q= q1 + q2 is the total industry output. The following formulas will be...

Consider a market where N firms produce a homogeneous product and compete by simultaneously setting quantities. The inverse demand function has the general form P PO-P(qi +q2 +q3 + + qv), where Q is total quantity produced, qi is the quantity produced by firm i and P is the market price. The demand curve is downward sloping, so P10 < 0. The total cost of firm i is given by Cig). (0) Show that P- MC qi i , where...

Consider a market where N firms produce a homogeneous product and compete by simultaneously setting quantities. The inverse demand function has the general form P PO-P(qi +q2 +q3 + + qv), where Q is total quantity produced, qi is the quantity produced by firm i and P is the market price. The demand curve is downward sloping, so P10 < 0. The total cost of firm i is given by Cig). (0) Show that P- MC qi i , where...

please explain all details.

Market demand curve for a good produced only by two

firms is given by P= 70- 20. Both firms produce with constant and

identical marginal cost of 3. 10, that is MC, = MC, = 10.

(P,Q.4-42,) in Cournot equilibrium. a) Find b) Find (P,Q,q1,92,,,

2) in Stackelberg equilibrium with Firm 1 acting as the leader. c)

Compare your findings with monopoly and competitive equilibria.

Market demand curve for a good produced only by two firms...

please explain all details.

Market demand curve for a good produced only by two

firms is given by P= 70- 20. Both firms produce with constant and

identical marginal cost of 3. 10, that is MC, = MC, = 10.

(P,Q.4-42,) in Cournot equilibrium. a) Find b) Find (P,Q,q1,92,,,

2) in Stackelberg equilibrium with Firm 1 acting as the leader. c)

Compare your findings with monopoly and competitive equilibria.

Market demand curve for a good produced only by two firms...

2. Two firms produce homogeneous products. Market demand is given by Q = 40-P, and each firm faces a marginal cost of production of 4 per unit The timing of the game is as follows. In Period 1, firm 1 chooses the quantity q it will sell. In Period 2, firm 2 (who observed firm 1s choice in period 1) chooses whether or not to enter the market. If firm 2 chooses to enter it must pay an entry fee...

2. Two firms produce homogeneous products. Market demand is given by Q = 40-P, and each firm faces a marginal cost of production of 4 per unit The timing of the game is as follows. In Period 1, firm 1 chooses the quantity q it will sell. In Period 2, firm 2 (who observed firm 1s choice in period 1) chooses whether or not to enter the market. If firm 2 chooses to enter it must pay an entry fee...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago