Homework Answers

Add Answer to:

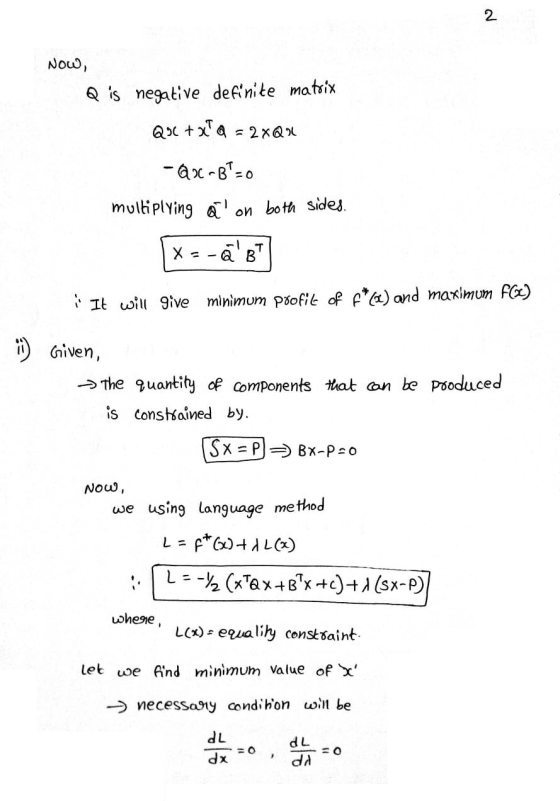

X is an n x 1 state vector with n decision variables. The n decision variables...

Find the steady state probability vector for the matrix. An eigenvector v of an n ×...

Find the steady state probability vector for the matrix. An

eigenvector v of an n × n matrix

A is a steady state probability vector when

Av = v and the

components of v sum to 1.

Find the steady state probability vector for the matrix. An eigenvector v of an n x n matrix A is a steady state probability vector when Av = v and the components of v sum to 1. 0.9 0.4 A = 0.1 0.6

Find the steady state probability vector for the matrix. An

eigenvector v of an n × n matrix

A is a steady state probability vector when

Av = v and the

components of v sum to 1.

Find the steady state probability vector for the matrix. An eigenvector v of an n x n matrix A is a steady state probability vector when Av = v and the components of v sum to 1. 0.9 0.4 A = 0.1 0.6

Exercise 5.2. This problem concerns the formulation of a model-based method for min imizing a twice-continuously...

Exercise 5.2. This problem concerns the formulation of a model-based method for min imizing a twice-continuously differentiable function f : Rn R. Let B be a symmetric positive-definite matrix. At a point xk, consider the quadratic model (a) Write the quadratic model in terms of the variables p -x - k and find pk such that PERn (b) Show that the vector pk of part (a) is a descent direction for f at xk (c) Show that if B is...

Exercise 5.2. This problem concerns the formulation of a model-based method for min imizing a twice-continuously differentiable function f : Rn R. Let B be a symmetric positive-definite matrix. At a point xk, consider the quadratic model (a) Write the quadratic model in terms of the variables p -x - k and find pk such that PERn (b) Show that the vector pk of part (a) is a descent direction for f at xk (c) Show that if B is...

Let P be the n*n transition matrix of a Markov chain with a finite state space...

Let P be the n*n transition matrix of a Markov chain with a finite state space S = {1, 2, ..., n}. Show that 7 is the stationary distribution of the Markov chain, i.e., P = , 2hTi = 1 if and only if (I – P+117) = 17 where I is the n*n identity matrix and 17 = [11...1) is a 1 * n row vector with all components being 1.

Let P be the n*n transition matrix of a Markov chain with a finite state space S = {1, 2, ..., n}. Show that 7 is the stationary distribution of the Markov chain, i.e., P = , 2hTi = 1 if and only if (I – P+117) = 17 where I is the n*n identity matrix and 17 = [11...1) is a 1 * n row vector with all components being 1.

The random vector Y = (Y1, ..., Yn)T is such that Y = Xβ + ε,...

The random vector Y = (Y1, ...,

Yn)T is such that Y = Xβ + ε, where X is an n

× p full-rank matrix of known constants, β is a p-length vector of

unknown parameters, and ε is an n-length vector of random

variables. A multiple linear regression model is fitted to the

data.

(a) Write down the multiple linear regression model assumptions in

matrix format.

(b) Derive the least squares estimator β^ of β.

(c) Using the data:...

The random vector Y = (Y1, ...,

Yn)T is such that Y = Xβ + ε, where X is an n

× p full-rank matrix of known constants, β is a p-length vector of

unknown parameters, and ε is an n-length vector of random

variables. A multiple linear regression model is fitted to the

data.

(a) Write down the multiple linear regression model assumptions in

matrix format.

(b) Derive the least squares estimator β^ of β.

(c) Using the data:...

Let βˆ = (X′X)−1X′y where y ∼ N(Xβ,σ2I), X is an n×(k+1) matrix, and β is a (k+1)×1 vector. Are βˆ′A′[A(X′X)−1A′]−1Aβˆ a...

Let βˆ = (X′X)−1X′y where y ∼

N(Xβ,σ2I), X is an n×(k+1) matrix, and β is a (k+1)×1 vector. Are

βˆ′A′[A(X′X)−1A′]−1Aβˆ and y′[I − X(X′X)−1X′]y independent?

Let B (X'X)-X'y where y ~ N(XB,02I), X is an n x (k+ 1) matrix, and B is a (k+1) x1 vector Are BA A (X'X)-A]-AB and yI - X(X'X)-xy independent?

Let B (X'X)-X'y where y ~ N(XB,02I), X is an n x (k+ 1) matrix, and B is a (k+1) x1 vector Are...

Let βˆ = (X′X)−1X′y where y ∼

N(Xβ,σ2I), X is an n×(k+1) matrix, and β is a (k+1)×1 vector. Are

βˆ′A′[A(X′X)−1A′]−1Aβˆ and y′[I − X(X′X)−1X′]y independent?

Let B (X'X)-X'y where y ~ N(XB,02I), X is an n x (k+ 1) matrix, and B is a (k+1) x1 vector Are BA A (X'X)-A]-AB and yI - X(X'X)-xy independent?

Let B (X'X)-X'y where y ~ N(XB,02I), X is an n x (k+ 1) matrix, and B is a (k+1) x1 vector Are...

4. a) Find a second order Taylor ser XN-[ 1]Tand then use it to find an approximate value of fX) at Note: the superscr...

4. a) Find a second order Taylor ser XN-[ 1]Tand then use it to find an approximate value of fX) at Note: the superscript "T" denotes the transpose of the vector) ies approximation of the following function about the point, a X - [0.8 1.2]. b) Consider the following multivariable cost function: f(X) (a x)(bx) where "a" and "b" denote nx1 constant vectors and X is a nx1 vector of decision variables. Find the gradient vector and Hessian matrix of...

4. a) Find a second order Taylor ser XN-[ 1]Tand then use it to find an approximate value of fX) at Note: the superscript "T" denotes the transpose of the vector) ies approximation of the following function about the point, a X - [0.8 1.2]. b) Consider the following multivariable cost function: f(X) (a x)(bx) where "a" and "b" denote nx1 constant vectors and X is a nx1 vector of decision variables. Find the gradient vector and Hessian matrix of...

1. Let Z = (Z1, Z2, Z3) be a vector with i.i.d. N(0, 1) components. Let...

1. Let Z = (Z1, Z2, Z3) be a vector with i.i.d. N(0, 1) components. Let r be a constant with 0 < r < 1. Define X1 = √ rZ1 + √ 1 − rZ2 and X2 = √ rZ1 + √ 1 − rZ3. (a) Give the distribution of X1 and the distribution of X2. Find Cov(X1, X2). (b) Give the matrix A so that the vector X = (X1, X2) is a transform X = AZ. Give...

Hello, please help solve problem and show all work thank you. (Linear models) Suppose we have a vector of n observations Y (response), which has distribution Nn(XB.ση where x is an n × p matrix of kn...

Hello, please help solve problem and show all work thank

you.

(Linear models) Suppose we have a vector of n observations Y (response), which has distribution Nn(XB.ση where x is an n × p matrix of known values (indepedent variables), which has full column rank p, and β is a p x 1 vector of unknown parameters. The least squares estimator of ß is 4. a. Determine the distribution of β. xB. Determine the distribution of Y b. Let Y...

Hello, please help solve problem and show all work thank

you.

(Linear models) Suppose we have a vector of n observations Y (response), which has distribution Nn(XB.ση where x is an n × p matrix of known values (indepedent variables), which has full column rank p, and β is a p x 1 vector of unknown parameters. The least squares estimator of ß is 4. a. Determine the distribution of β. xB. Determine the distribution of Y b. Let Y...

2) Suppose you have multiple regression set up Ynxi XnxpBpxi Sxl and f ~ N(0nx1, σ21.). P Po X(X,...

linear statistics modeling and regression

2) Suppose you have multiple regression set up Ynxi XnxpBpxi Sxl and f ~ N(0nx1, σ21.). P Po X(X,X)-X, be the projection matrix on the column space of X. a) Show residual vector, e = (1,-P)Y. Here e is the vector of residuals ei S. b) Show that the variance of e, is 1 - Pi, where P is the i, j th entry of the matrix P c) Show that the sample covariance of...

linear statistics modeling and regression

2) Suppose you have multiple regression set up Ynxi XnxpBpxi Sxl and f ~ N(0nx1, σ21.). P Po X(X,X)-X, be the projection matrix on the column space of X. a) Show residual vector, e = (1,-P)Y. Here e is the vector of residuals ei S. b) Show that the variance of e, is 1 - Pi, where P is the i, j th entry of the matrix P c) Show that the sample covariance of...

(a) Suppose we want to solve the linear vector-matrix equation Ax b for the vector x. Show that the Gauss elimination algorithm may be written bAbm,B where m 1, This process produces a matrix equa...

(a) Suppose we want to solve the linear vector-matrix equation Ax b for the vector x. Show that the Gauss elimination algorithm may be written bAbm,B where m 1, This process produces a matrix equation of the form Ux = g , in which matrix U is an upper-triangular matrix. Show that the solution vector x may be obtained by a back-substitution algorithm, in the form Jekel (b) Iterative methods for solving Ax-b work by splitting matrix A into two...

(a) Suppose we want to solve the linear vector-matrix equation Ax b for the vector x. Show that the Gauss elimination algorithm may be written bAbm,B where m 1, This process produces a matrix equation of the form Ux = g , in which matrix U is an upper-triangular matrix. Show that the solution vector x may be obtained by a back-substitution algorithm, in the form Jekel (b) Iterative methods for solving Ax-b work by splitting matrix A into two...

Find the steady state probability vector for the matrix. An

eigenvector v of an n × n matrix

A is a steady state probability vector when

Av = v and the

components of v sum to 1.

Find the steady state probability vector for the matrix. An eigenvector v of an n x n matrix A is a steady state probability vector when Av = v and the components of v sum to 1. 0.9 0.4 A = 0.1 0.6

Find the steady state probability vector for the matrix. An

eigenvector v of an n × n matrix

A is a steady state probability vector when

Av = v and the

components of v sum to 1.

Find the steady state probability vector for the matrix. An eigenvector v of an n x n matrix A is a steady state probability vector when Av = v and the components of v sum to 1. 0.9 0.4 A = 0.1 0.6

Exercise 5.2. This problem concerns the formulation of a model-based method for min imizing a twice-continuously differentiable function f : Rn R. Let B be a symmetric positive-definite matrix. At a point xk, consider the quadratic model (a) Write the quadratic model in terms of the variables p -x - k and find pk such that PERn (b) Show that the vector pk of part (a) is a descent direction for f at xk (c) Show that if B is...

Exercise 5.2. This problem concerns the formulation of a model-based method for min imizing a twice-continuously differentiable function f : Rn R. Let B be a symmetric positive-definite matrix. At a point xk, consider the quadratic model (a) Write the quadratic model in terms of the variables p -x - k and find pk such that PERn (b) Show that the vector pk of part (a) is a descent direction for f at xk (c) Show that if B is...

Let P be the n*n transition matrix of a Markov chain with a finite state space S = {1, 2, ..., n}. Show that 7 is the stationary distribution of the Markov chain, i.e., P = , 2hTi = 1 if and only if (I – P+117) = 17 where I is the n*n identity matrix and 17 = [11...1) is a 1 * n row vector with all components being 1.

Let P be the n*n transition matrix of a Markov chain with a finite state space S = {1, 2, ..., n}. Show that 7 is the stationary distribution of the Markov chain, i.e., P = , 2hTi = 1 if and only if (I – P+117) = 17 where I is the n*n identity matrix and 17 = [11...1) is a 1 * n row vector with all components being 1.

The random vector Y = (Y1, ...,

Yn)T is such that Y = Xβ + ε, where X is an n

× p full-rank matrix of known constants, β is a p-length vector of

unknown parameters, and ε is an n-length vector of random

variables. A multiple linear regression model is fitted to the

data.

(a) Write down the multiple linear regression model assumptions in

matrix format.

(b) Derive the least squares estimator β^ of β.

(c) Using the data:...

The random vector Y = (Y1, ...,

Yn)T is such that Y = Xβ + ε, where X is an n

× p full-rank matrix of known constants, β is a p-length vector of

unknown parameters, and ε is an n-length vector of random

variables. A multiple linear regression model is fitted to the

data.

(a) Write down the multiple linear regression model assumptions in

matrix format.

(b) Derive the least squares estimator β^ of β.

(c) Using the data:...

Let βˆ = (X′X)−1X′y where y ∼

N(Xβ,σ2I), X is an n×(k+1) matrix, and β is a (k+1)×1 vector. Are

βˆ′A′[A(X′X)−1A′]−1Aβˆ and y′[I − X(X′X)−1X′]y independent?

Let B (X'X)-X'y where y ~ N(XB,02I), X is an n x (k+ 1) matrix, and B is a (k+1) x1 vector Are BA A (X'X)-A]-AB and yI - X(X'X)-xy independent?

Let B (X'X)-X'y where y ~ N(XB,02I), X is an n x (k+ 1) matrix, and B is a (k+1) x1 vector Are...

Let βˆ = (X′X)−1X′y where y ∼

N(Xβ,σ2I), X is an n×(k+1) matrix, and β is a (k+1)×1 vector. Are

βˆ′A′[A(X′X)−1A′]−1Aβˆ and y′[I − X(X′X)−1X′]y independent?

Let B (X'X)-X'y where y ~ N(XB,02I), X is an n x (k+ 1) matrix, and B is a (k+1) x1 vector Are BA A (X'X)-A]-AB and yI - X(X'X)-xy independent?

Let B (X'X)-X'y where y ~ N(XB,02I), X is an n x (k+ 1) matrix, and B is a (k+1) x1 vector Are...

4. a) Find a second order Taylor ser XN-[ 1]Tand then use it to find an approximate value of fX) at Note: the superscript "T" denotes the transpose of the vector) ies approximation of the following function about the point, a X - [0.8 1.2]. b) Consider the following multivariable cost function: f(X) (a x)(bx) where "a" and "b" denote nx1 constant vectors and X is a nx1 vector of decision variables. Find the gradient vector and Hessian matrix of...

4. a) Find a second order Taylor ser XN-[ 1]Tand then use it to find an approximate value of fX) at Note: the superscript "T" denotes the transpose of the vector) ies approximation of the following function about the point, a X - [0.8 1.2]. b) Consider the following multivariable cost function: f(X) (a x)(bx) where "a" and "b" denote nx1 constant vectors and X is a nx1 vector of decision variables. Find the gradient vector and Hessian matrix of...

Hello, please help solve problem and show all work thank

you.

(Linear models) Suppose we have a vector of n observations Y (response), which has distribution Nn(XB.ση where x is an n × p matrix of known values (indepedent variables), which has full column rank p, and β is a p x 1 vector of unknown parameters. The least squares estimator of ß is 4. a. Determine the distribution of β. xB. Determine the distribution of Y b. Let Y...

Hello, please help solve problem and show all work thank

you.

(Linear models) Suppose we have a vector of n observations Y (response), which has distribution Nn(XB.ση where x is an n × p matrix of known values (indepedent variables), which has full column rank p, and β is a p x 1 vector of unknown parameters. The least squares estimator of ß is 4. a. Determine the distribution of β. xB. Determine the distribution of Y b. Let Y...

linear statistics modeling and regression

2) Suppose you have multiple regression set up Ynxi XnxpBpxi Sxl and f ~ N(0nx1, σ21.). P Po X(X,X)-X, be the projection matrix on the column space of X. a) Show residual vector, e = (1,-P)Y. Here e is the vector of residuals ei S. b) Show that the variance of e, is 1 - Pi, where P is the i, j th entry of the matrix P c) Show that the sample covariance of...

linear statistics modeling and regression

2) Suppose you have multiple regression set up Ynxi XnxpBpxi Sxl and f ~ N(0nx1, σ21.). P Po X(X,X)-X, be the projection matrix on the column space of X. a) Show residual vector, e = (1,-P)Y. Here e is the vector of residuals ei S. b) Show that the variance of e, is 1 - Pi, where P is the i, j th entry of the matrix P c) Show that the sample covariance of...

(a) Suppose we want to solve the linear vector-matrix equation Ax b for the vector x. Show that the Gauss elimination algorithm may be written bAbm,B where m 1, This process produces a matrix equation of the form Ux = g , in which matrix U is an upper-triangular matrix. Show that the solution vector x may be obtained by a back-substitution algorithm, in the form Jekel (b) Iterative methods for solving Ax-b work by splitting matrix A into two...

(a) Suppose we want to solve the linear vector-matrix equation Ax b for the vector x. Show that the Gauss elimination algorithm may be written bAbm,B where m 1, This process produces a matrix equation of the form Ux = g , in which matrix U is an upper-triangular matrix. Show that the solution vector x may be obtained by a back-substitution algorithm, in the form Jekel (b) Iterative methods for solving Ax-b work by splitting matrix A into two...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago