Explain in detail how to design an optimal portfolio with N risky assets. What is an...

Explain in detail how to design an optimal portfolio with N risky assets. What is an efficient frontier?

Homework Answers

Designing an optimal portfolio with N risky assets

An optimal portfolio is the one that maximizes your returns for a given level of risk, or minimizes the risk for a given return(expected).

It implies that both the risk and return cannot be seen in isolation. Both of them are positively co-related, higher the risk, higher would be the returns associated.

Firstly, diversify into more asset classes having low correlations to stocks and bonds. Also, diversification into active strategies can be done.

An investor is interested in investing capital in number of available assets(n) so that the expected return is maximized.

With a set of n assets, with asset j ∈ {1 . . . n} having a return of Rj at the end of the investment period.

Let xj be the percentage of capital invested in asset j

Let x = (x1, . . . , xn) denote the portfolio choice

The portfolio’s return is given as

Rx = x1R1 + . . . + xnRn (Rj - Random variable)

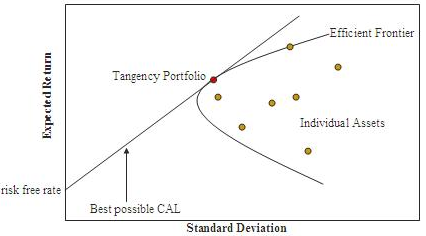

Efficient Frontier

An efficient frontier is a set of optimal portfolios that offer the highest returns(expected) with a defined level of lowest risk.

Portfolios that lie below the efficient frontier are considered sub-optimal, as for the given risk, they offer lower returns. Refer to the graph above.

Add Answer to:

Explain in detail how to design an optimal portfolio with N

risky assets. What is an...

(Note: select all correct answers) The optimal risky portfolio can be identified by finding the minimum...

(Note: select all correct answers) The optimal risky portfolio can be identified by finding the minimum variance point on the efficient frontier the maximum return point on the efficient frontier the tangency point of the capital market line and the efficient frontier the line with the steepest slope that connects the risk free rate to the efficient frontier

(Note: select all correct answers) The optimal risky portfolio can be identified by finding the minimum variance point on the efficient frontier the maximum return point on the efficient frontier the tangency point of the capital market line and the efficient frontier the line with the steepest slope that connects the risk free rate to the efficient frontier

II. Essays/Calculations (60%) 1. (a) Please draw the efficient frontier for a portfolio of N>2 risky...

II. Essays/Calculations (60%) 1. (a) Please draw the efficient frontier for a portfolio of N>2 risky assets (with x-axis and y-axis properly labeled). (b) When the risk-free asset is included into the portfolio, what happened to the optimal feasible set?

II. Essays/Calculations (60%) 1. (a) Please draw the efficient frontier for a portfolio of N>2 risky assets (with x-axis and y-axis properly labeled). (b) When the risk-free asset is included into the portfolio, what happened to the optimal feasible set?

2. (Understanding optimal portfolio choice) Consider two risky assets, the expected return of asset one is...

2. (Understanding optimal portfolio choice) Consider two risky assets, the expected return of asset one is μ-0.1, the expected return of asset two is μ2-0.15, the risk or standard deviation of asset one is σ1-0.1, the risk or standard deviation of asset two is σ2-02. The two assets also happen to have zero correlation. An investor plans to build a portfolio by investing w of his investment to asset one and the rest of his investment to asset two. Calculate...

2. (Understanding optimal portfolio choice) Consider two risky assets, the expected return of asset one is μ-0.1, the expected return of asset two is μ2-0.15, the risk or standard deviation of asset one is σ1-0.1, the risk or standard deviation of asset two is σ2-02. The two assets also happen to have zero correlation. An investor plans to build a portfolio by investing w of his investment to asset one and the rest of his investment to asset two. Calculate...

Which of the following is a TRUE statement? A The tangent portfolio is the risky portfolio...

Which of the following is a TRUE statement? A The tangent portfolio is the risky portfolio on the efficient frontier whose tangent line cuts the horizontal axis at the risk-free rate. B The new (or super) efficient frontier represents the portfolios composed of the risk-free rate and the tangent portfolio that offers the highest expected rate of return for any given level or risk. C The separation theorem states that the investment decision, (how to construct the portfolio of risky...

3. (a) In the case of multiple risky assets, explain the concepts of efficient frontier and...

3. (a) In the case of multiple risky assets, explain the concepts of efficient frontier and feasible region. 5 points] (b) Suppose there are n risky assets (e.g. stocks) and a risk-free asset in the market. Explain how a mean-variance investor allocates his wealth across these assets. [10 points

3. (a) In the case of multiple risky assets, explain the concepts of efficient frontier and feasible region. 5 points] (b) Suppose there are n risky assets (e.g. stocks) and a risk-free asset in the market. Explain how a mean-variance investor allocates his wealth across these assets. [10 points

Suppose the optimal risky portfolio has an expected return of 13.25% and a standard deviation of...

Suppose the optimal risky portfolio has an expected return of 13.25% and a standard deviation of 24.57%. Mr. Jones wants an efficient portfolio with an expected return of 12%. If the optimal risky portfolio consists of 70.75% in stocks and 29.25% in bonds, what is the proportion of Mr. Jones' portfolio invested in the stock fund. the risk-free rate is 5.5%.

An investor's risk aversion determines her a. optimal mix of assets in her risky portfolio b....

An investor's risk aversion determines her a. optimal mix of assets in her risky portfolio b. risk-free rate on borrowing c. Sharpe ratio d. capital allocation line e. optimal risky portfolio f. risk-free rate on lending

) What does the indifference curve represent? ii) What is CAL(P)? iii) What is the efficient...

) What does the indifference curve represent?

ii) What is CAL(P)?

iii) What is the efficient frontier of risky assets?

iv) Explain what the point C represents.

v) How can an investor access pointK?

(c) Outline and discuss three limitations of the CAPM.

(b) Consider the following graph: CAL(P) E(R) Indifference curve Efficient frontier of risky assets Optimal risky portfolio Expected return (%) Standard deviation (%)

) What does the indifference curve represent?

ii) What is CAL(P)?

iii) What is the efficient frontier of risky assets?

iv) Explain what the point C represents.

v) How can an investor access pointK?

(c) Outline and discuss three limitations of the CAPM.

(b) Consider the following graph: CAL(P) E(R) Indifference curve Efficient frontier of risky assets Optimal risky portfolio Expected return (%) Standard deviation (%)

The difference between the optimal risky portfolio and optimal complete portfolio?

The difference between the optimal risky portfolio and optimal complete portfolio?

Q5. Discuss the followings in the context of portfolio theory, developed by Harry Markowitz: a) What...

Q5. Discuss the followings in the context of portfolio theory, developed by Harry Markowitz: a) What is meant by a risk-averse investor? b) What is meant by a Markowitz efficient frontier? c) Explain why not all feasible portfolios are on the Markwitz frontier. d) What is meant by an optimal portfolio, and how it is related to an efficient portfolio? e) How does an investor select an optimal portfolio? Explain the role of an investor's preference in selecting an optimal...

Q5. Discuss the followings in the context of portfolio theory, developed by Harry Markowitz: a) What is meant by a risk-averse investor? b) What is meant by a Markowitz efficient frontier? c) Explain why not all feasible portfolios are on the Markwitz frontier. d) What is meant by an optimal portfolio, and how it is related to an efficient portfolio? e) How does an investor select an optimal portfolio? Explain the role of an investor's preference in selecting an optimal...

(Note: select all correct answers) The optimal risky portfolio can be identified by finding the minimum variance point on the efficient frontier the maximum return point on the efficient frontier the tangency point of the capital market line and the efficient frontier the line with the steepest slope that connects the risk free rate to the efficient frontier

(Note: select all correct answers) The optimal risky portfolio can be identified by finding the minimum variance point on the efficient frontier the maximum return point on the efficient frontier the tangency point of the capital market line and the efficient frontier the line with the steepest slope that connects the risk free rate to the efficient frontier

II. Essays/Calculations (60%) 1. (a) Please draw the efficient frontier for a portfolio of N>2 risky assets (with x-axis and y-axis properly labeled). (b) When the risk-free asset is included into the portfolio, what happened to the optimal feasible set?

II. Essays/Calculations (60%) 1. (a) Please draw the efficient frontier for a portfolio of N>2 risky assets (with x-axis and y-axis properly labeled). (b) When the risk-free asset is included into the portfolio, what happened to the optimal feasible set?

2. (Understanding optimal portfolio choice) Consider two risky assets, the expected return of asset one is μ-0.1, the expected return of asset two is μ2-0.15, the risk or standard deviation of asset one is σ1-0.1, the risk or standard deviation of asset two is σ2-02. The two assets also happen to have zero correlation. An investor plans to build a portfolio by investing w of his investment to asset one and the rest of his investment to asset two. Calculate...

2. (Understanding optimal portfolio choice) Consider two risky assets, the expected return of asset one is μ-0.1, the expected return of asset two is μ2-0.15, the risk or standard deviation of asset one is σ1-0.1, the risk or standard deviation of asset two is σ2-02. The two assets also happen to have zero correlation. An investor plans to build a portfolio by investing w of his investment to asset one and the rest of his investment to asset two. Calculate...

3. (a) In the case of multiple risky assets, explain the concepts of efficient frontier and feasible region. 5 points] (b) Suppose there are n risky assets (e.g. stocks) and a risk-free asset in the market. Explain how a mean-variance investor allocates his wealth across these assets. [10 points

3. (a) In the case of multiple risky assets, explain the concepts of efficient frontier and feasible region. 5 points] (b) Suppose there are n risky assets (e.g. stocks) and a risk-free asset in the market. Explain how a mean-variance investor allocates his wealth across these assets. [10 points

) What does the indifference curve represent?

ii) What is CAL(P)?

iii) What is the efficient frontier of risky assets?

iv) Explain what the point C represents.

v) How can an investor access pointK?

(c) Outline and discuss three limitations of the CAPM.

(b) Consider the following graph: CAL(P) E(R) Indifference curve Efficient frontier of risky assets Optimal risky portfolio Expected return (%) Standard deviation (%)

) What does the indifference curve represent?

ii) What is CAL(P)?

iii) What is the efficient frontier of risky assets?

iv) Explain what the point C represents.

v) How can an investor access pointK?

(c) Outline and discuss three limitations of the CAPM.

(b) Consider the following graph: CAL(P) E(R) Indifference curve Efficient frontier of risky assets Optimal risky portfolio Expected return (%) Standard deviation (%)

Q5. Discuss the followings in the context of portfolio theory, developed by Harry Markowitz: a) What is meant by a risk-averse investor? b) What is meant by a Markowitz efficient frontier? c) Explain why not all feasible portfolios are on the Markwitz frontier. d) What is meant by an optimal portfolio, and how it is related to an efficient portfolio? e) How does an investor select an optimal portfolio? Explain the role of an investor's preference in selecting an optimal...

Q5. Discuss the followings in the context of portfolio theory, developed by Harry Markowitz: a) What is meant by a risk-averse investor? b) What is meant by a Markowitz efficient frontier? c) Explain why not all feasible portfolios are on the Markwitz frontier. d) What is meant by an optimal portfolio, and how it is related to an efficient portfolio? e) How does an investor select an optimal portfolio? Explain the role of an investor's preference in selecting an optimal...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago