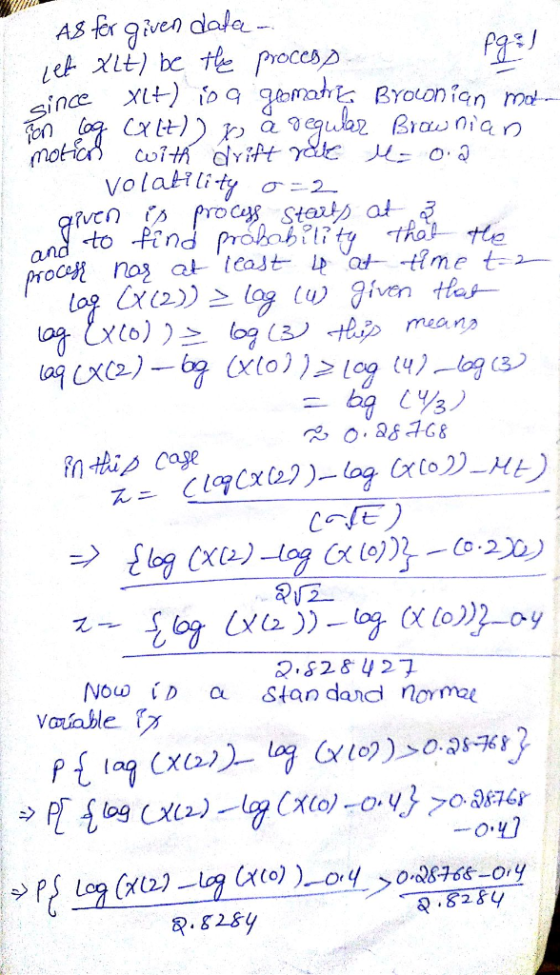

A geometric Brownian motion has parameters mu= 0.2 and sigma=2. What is the probability that the...

A geometric Brownian motion has parameters mu= 0.2 and sigma=2. What is the probability that the process is above 4 at time t=4, given that it starts at 3. Round answer to 3 decimals.

Homework Answers

I HOPE ITS HELP FUL TO YOU IF YOU HAVE ANY DOUBTS PLS COMMENTS BELOW..I WILL BE THERE TO HELP..ALL THE BEST...

I HOPE YOU UNDERSTAND...

PLS RATE THUMBS UP...ITS HELPS ME ALOT.....

THANK YOU....!!

Add Answer to:

A geometric Brownian motion has parameters mu= 0.2 and sigma=2.

What is the probability that the...

Let S(t), t >=0 be a Geometric Brownian motion process with drift mu = 0.1 and volatility sigma = 0.2. Find P(S(2) &g...

Let S(t), t >=0 be a Geometric Brownian motion process with drift mu = 0.1 and volatility sigma = 0.2. Find P(S(2) >S(1) > S(0))

If X(t), t>=0 is a Brownian motion process with drift mu and variance sigma squared for which X(0)=0, show that -X(t)...

If X(t), t>=0 is a Brownian motion process with drift mu and variance sigma squared for which X(0)=0, show that -X(t), t>=0 is a Brownian Motion process with drift negative mu and variance sigma squared.

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the...

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

Let x be an arithmetic brownian motion starting from 0 with drift parameter 0.2 Let X-(Xt...

Let x be an arithmetic brownian motion starting from 0 with

drift parameter 0.2

Let X-(Xt ,0 < t < 1} be an arithmetic Brownian motion starting from 0 with drift parameter μ-0.2 and variance parameter ơ2-0.125. 1. Calculate the probability that X2 is between 0.1 and 0.5 2. Given that X 0.6, find the probability that X2 is between 0.1 and 0.5 3. Given that Xi- 0.2, find the covariance between X2 and X3

Let x be an arithmetic brownian motion starting from 0 with

drift parameter 0.2

Let X-(Xt ,0 < t < 1} be an arithmetic Brownian motion starting from 0 with drift parameter μ-0.2 and variance parameter ơ2-0.125. 1. Calculate the probability that X2 is between 0.1 and 0.5 2. Given that X 0.6, find the probability that X2 is between 0.1 and 0.5 3. Given that Xi- 0.2, find the covariance between X2 and X3

2. Solving the generalized geometric Brownian motion equation. Let S(t) be a positive stochastic process that...

2. Solving the generalized geometric Brownian motion equation. Let S(t) be a positive stochastic process that satisfies the generalized geometric Brownian motion SDE dS(t) = u(t)S(t) dt + o(t)S(t) dW(t), where u(t) and o(t) are processes adapted to the filtration Ft, t > 0. (a) Use Itô’s lemma to compute d log S(t). Simplify so that you have a formula for d log S(t) that does not involve S(t). (b) Integrate the formula you obtained in (a), and then exponentiate...

2. Solving the generalized geometric Brownian motion equation. Let S(t) be a positive stochastic process that satisfies the generalized geometric Brownian motion SDE dS(t) = u(t)S(t) dt + o(t)S(t) dW(t), where u(t) and o(t) are processes adapted to the filtration Ft, t > 0. (a) Use Itô’s lemma to compute d log S(t). Simplify so that you have a formula for d log S(t) that does not involve S(t). (b) Integrate the formula you obtained in (a), and then exponentiate...

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the...

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

1) given mu = 20 and sigma = 3 a) probability(x<18) b)probability(x>21) 2) given mu =...

1) given mu = 20 and sigma = 3 a) probability(x<18) b)probability(x>21) 2) given mu = 50 and sigma = 4 a) find 90% confidence interval b) find 94%

Let X-(Xt ,0 < t < 1} be an arithmetic Brownian motion starting from 0 with...

Let X-(Xt ,0 < t < 1} be an arithmetic Brownian motion starting from 0 with drift parameter μ-0.2 and variance parameter ơ2-0.125. 1. Calculate the probability that X2 is between 0.1 and 0.5 2. Given that X 0.6, find the probability that X2 is between 0.1 and 0.5 3. Given that Xi- 0.2, find the covariance between X2 and X3

Let X-(Xt ,0 < t < 1} be an arithmetic Brownian motion starting from 0 with drift parameter μ-0.2 and variance parameter ơ2-0.125. 1. Calculate the probability that X2 is between 0.1 and 0.5 2. Given that X 0.6, find the probability that X2 is between 0.1 and 0.5 3. Given that Xi- 0.2, find the covariance between X2 and X3

Assume an asset price St follows the geometric Brownian motion, dSt = u Stdt+oS+dZt, So =s...

Assume an asset price St follows the geometric Brownian motion, dSt = u Stdt+oS+dZt, So =s > 0 where u and o are constants, r is the risk-free rate, and Zt is the Brownian motion. 1. Using the Ito's Lemma find to the stochastic differential equation satisfied by the process X+ = St. 2. Compute E[Xt] and Var[Xt]. 3. Using the Ito's Lemma find the stochastic differential equation satisfied by the process Y1 = Sert'. 4. Compute E[Y] and Var[Y].

Assume an asset price St follows the geometric Brownian motion, dSt = u Stdt+oS+dZt, So =s > 0 where u and o are constants, r is the risk-free rate, and Zt is the Brownian motion. 1. Using the Ito's Lemma find to the stochastic differential equation satisfied by the process X+ = St. 2. Compute E[Xt] and Var[Xt]. 3. Using the Ito's Lemma find the stochastic differential equation satisfied by the process Y1 = Sert'. 4. Compute E[Y] and Var[Y].

3. Brounian motion f(O)eR+ is a special case of a Gaussian process with mean zero and covariance C(s, t) = min(s, t) (a) What is the distribution of f(1), the Brownian motion at time t = 4? (Hint...

3. Brounian motion f(O)eR+ is a special case of a Gaussian process with mean zero and covariance C(s, t) = min(s, t) (a) What is the distribution of f(1), the Brownian motion at time t = 4? (Hint: it may be useful to function recall that for any random variable X, var(X)-(x, X) (b) Fix tE R. What is the distribution of f(t)? (c) What is the distribution of f(4)-f(2)? (Hint: it may be useful to utilize var(X-Y) = var(X)...

3. Brounian motion f(O)eR+ is a special case of a Gaussian process with mean zero and covariance C(s, t) = min(s, t) (a) What is the distribution of f(1), the Brownian motion at time t = 4? (Hint: it may be useful to function recall that for any random variable X, var(X)-(x, X) (b) Fix tE R. What is the distribution of f(t)? (c) What is the distribution of f(4)-f(2)? (Hint: it may be useful to utilize var(X-Y) = var(X)...

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

Let x be an arithmetic brownian motion starting from 0 with

drift parameter 0.2

Let X-(Xt ,0 < t < 1} be an arithmetic Brownian motion starting from 0 with drift parameter μ-0.2 and variance parameter ơ2-0.125. 1. Calculate the probability that X2 is between 0.1 and 0.5 2. Given that X 0.6, find the probability that X2 is between 0.1 and 0.5 3. Given that Xi- 0.2, find the covariance between X2 and X3

Let x be an arithmetic brownian motion starting from 0 with

drift parameter 0.2

Let X-(Xt ,0 < t < 1} be an arithmetic Brownian motion starting from 0 with drift parameter μ-0.2 and variance parameter ơ2-0.125. 1. Calculate the probability that X2 is between 0.1 and 0.5 2. Given that X 0.6, find the probability that X2 is between 0.1 and 0.5 3. Given that Xi- 0.2, find the covariance between X2 and X3

2. Solving the generalized geometric Brownian motion equation. Let S(t) be a positive stochastic process that satisfies the generalized geometric Brownian motion SDE dS(t) = u(t)S(t) dt + o(t)S(t) dW(t), where u(t) and o(t) are processes adapted to the filtration Ft, t > 0. (a) Use Itô’s lemma to compute d log S(t). Simplify so that you have a formula for d log S(t) that does not involve S(t). (b) Integrate the formula you obtained in (a), and then exponentiate...

2. Solving the generalized geometric Brownian motion equation. Let S(t) be a positive stochastic process that satisfies the generalized geometric Brownian motion SDE dS(t) = u(t)S(t) dt + o(t)S(t) dW(t), where u(t) and o(t) are processes adapted to the filtration Ft, t > 0. (a) Use Itô’s lemma to compute d log S(t). Simplify so that you have a formula for d log S(t) that does not involve S(t). (b) Integrate the formula you obtained in (a), and then exponentiate...

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

If s follows the geometric Brownian motion process ds - S dt+oS dz what is the process followed by (a) y = 2S, (b) y S 5.

Let X-(Xt ,0 < t < 1} be an arithmetic Brownian motion starting from 0 with drift parameter μ-0.2 and variance parameter ơ2-0.125. 1. Calculate the probability that X2 is between 0.1 and 0.5 2. Given that X 0.6, find the probability that X2 is between 0.1 and 0.5 3. Given that Xi- 0.2, find the covariance between X2 and X3

Let X-(Xt ,0 < t < 1} be an arithmetic Brownian motion starting from 0 with drift parameter μ-0.2 and variance parameter ơ2-0.125. 1. Calculate the probability that X2 is between 0.1 and 0.5 2. Given that X 0.6, find the probability that X2 is between 0.1 and 0.5 3. Given that Xi- 0.2, find the covariance between X2 and X3

Assume an asset price St follows the geometric Brownian motion, dSt = u Stdt+oS+dZt, So =s > 0 where u and o are constants, r is the risk-free rate, and Zt is the Brownian motion. 1. Using the Ito's Lemma find to the stochastic differential equation satisfied by the process X+ = St. 2. Compute E[Xt] and Var[Xt]. 3. Using the Ito's Lemma find the stochastic differential equation satisfied by the process Y1 = Sert'. 4. Compute E[Y] and Var[Y].

Assume an asset price St follows the geometric Brownian motion, dSt = u Stdt+oS+dZt, So =s > 0 where u and o are constants, r is the risk-free rate, and Zt is the Brownian motion. 1. Using the Ito's Lemma find to the stochastic differential equation satisfied by the process X+ = St. 2. Compute E[Xt] and Var[Xt]. 3. Using the Ito's Lemma find the stochastic differential equation satisfied by the process Y1 = Sert'. 4. Compute E[Y] and Var[Y].

3. Brounian motion f(O)eR+ is a special case of a Gaussian process with mean zero and covariance C(s, t) = min(s, t) (a) What is the distribution of f(1), the Brownian motion at time t = 4? (Hint: it may be useful to function recall that for any random variable X, var(X)-(x, X) (b) Fix tE R. What is the distribution of f(t)? (c) What is the distribution of f(4)-f(2)? (Hint: it may be useful to utilize var(X-Y) = var(X)...

3. Brounian motion f(O)eR+ is a special case of a Gaussian process with mean zero and covariance C(s, t) = min(s, t) (a) What is the distribution of f(1), the Brownian motion at time t = 4? (Hint: it may be useful to function recall that for any random variable X, var(X)-(x, X) (b) Fix tE R. What is the distribution of f(t)? (c) What is the distribution of f(4)-f(2)? (Hint: it may be useful to utilize var(X-Y) = var(X)...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago