The market demand and supply functions for a type of carpet known as KP-7 have been...

The market demand and supply functions for a type of carpet known as KP-7 have been estimated, respectively, as: QD =140–4P, QS =–100+20P. where P is the price (dollars per yard) and Q is the rate of sales (hundreds of yards per month). A typical firm in this market has a total cost function given as: TC = 50 – 20q + 3q2, and MC = 6q - 20 where q is the firm’s output level.

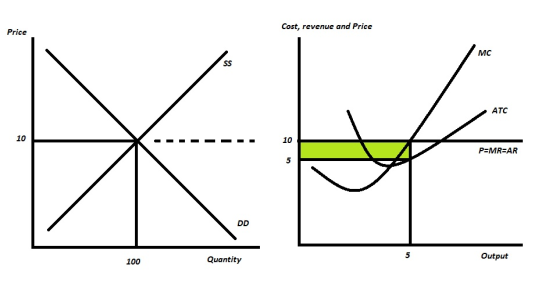

(a) What are the market price and quantity?

(b) What is the output rate of the typical firm? What is this typical firm’s profits? How many firms are in the industry? (assume all firms have the same cost functions and are identical)

(c) On two graphs, side-by-side, draw the market and individual firm curves, highlighting the price and output levels.

Homework Answers

QD =140–4P, QS =–100+20P are the demand and supply functions, we know that at the point of equilibrium the quantity demanded equals the quantity supplied.

Thus 140–4P =–100+20P

240 = 24P or P = 10, at P=10 (Market Price) , market quantity will be Q = 140-4*10 = 100 (Market Quantity)

The equilibrium for firm will be P=MC

10 = 6q-20

6q = 30 or q= 5 (output of a typical firm)

ATC =TC/q, at q = 5, = 50/q-20q/q+3q^2/q

= 50/q-20+3q, at q=5, ATC = 50/5-20+3*5 = 5

Profits = (P-ATC)*q = (10-5)*5 = 25 (for a typical firm)

The number of firms (N) = Q/q = 100/5 = 20 firms

Add Answer to:

The market demand and supply functions for a type of carpet

known as KP-7 have been...

1) Assume that the market demand and supply functions for Nice to See book factory shelves...

1) Assume that the market demand and supply functions for Nice to See book factory shelves are: QD = 720 - 12P (Market Demand) QS = -240 + 20P (Market Supply) where QD is the market demand of book shelves, QS is the quantity of book shelves produced and P is the market price per unit. (i) Calculate the equilibrium quantity and price for the book shelves before and after the imposition of a RM15 per unit tax. (12 marks)...

Question 5 (15 marks) Market demand is given as QD = 120 - P. Market supply...

Question 5 (15 marks) Market demand is given as QD = 120 - P. Market supply is given as QS = 4P. Each identical firm has MC = 6Q and ATC = 3Q. Showing your calculations, answer the following questions: A) What quantity of output will a typical firm produce? (5 marks) B) What is a typical firm's average total cost? (5 marks) C) What is a a typical firm's profit? (5 marks)

Question 5 (15 marks) Market demand is given as QD = 120 - P. Market supply is given as QS = 4P. Each identical firm has MC = 6Q and ATC = 3Q. Showing your calculations, answer the following questions: A) What quantity of output will a typical firm produce? (5 marks) B) What is a typical firm's average total cost? (5 marks) C) What is a a typical firm's profit? (5 marks)

4. The market for apples is perfectly competitive. The market demand for apples has been estimated...

4. The market for apples is perfectly competitive. The market demand for apples has been estimated as follows: Qd = 54,400 - 900P, where Q is measured in thousands of cases The market supply is Qs = 4000 + 800P Each apple producer has a total cost function given as: TC = 2400 +59 +0.0625q? Find the market price and quantity, firm output and profits. How many firms are there? Market price $ Market output Firm output Firm profits $...

4. The market for apples is perfectly competitive. The market demand for apples has been estimated as follows: Qd = 54,400 - 900P, where Q is measured in thousands of cases The market supply is Qs = 4000 + 800P Each apple producer has a total cost function given as: TC = 2400 +59 +0.0625q? Find the market price and quantity, firm output and profits. How many firms are there? Market price $ Market output Firm output Firm profits $...

4. The market for apples is perfectly competitive. The market demand for apples has been estimated...

4. The market for apples is perfectly competitive. The market demand for apples has been estimated as follows: Qd = 54,400 - 900P, where is measured in thousands of cases The market supply is Qs 4000 + 800P Each apple producer has a total cost function given as: TC = 2400 + 54 +0.0625q? Find the market price and quantity, firm output and profits. How many firms are there? Market price $. Market output. Firm output Firm profits $ Number...

4. The market for apples is perfectly competitive. The market demand for apples has been estimated as follows: Qd = 54,400 - 900P, where is measured in thousands of cases The market supply is Qs 4000 + 800P Each apple producer has a total cost function given as: TC = 2400 + 54 +0.0625q? Find the market price and quantity, firm output and profits. How many firms are there? Market price $. Market output. Firm output Firm profits $ Number...

Suppose that the market for a children’s book is given by the following demand and supply...

Suppose that the market for a children’s book is given by the following demand and supply functions: Demand: QD= 98 - 4P Supply: QS= -4 + 2P Where: QD and QS are quantity demand and quantity supplied respectively, and P is the price. The equilibrium price is $______

1. For a perfectly competitive firm, long-run average cost is: LAC = 300 - 20Q +...

1. For a perfectly competitive firm, long-run average cost is: LAC = 300 - 20Q + 1.8Q2, where Q denotes the firm’s output. The firm’s long-run profit-maximizing price is _____. 2. Demand for a good is given by: QD = 50 – 2P and supply by QS = 1P – 10, where P is the market price of the good. In equilibrium, price would be ___. 3. Demand for a good is given by: QD = 50 – 2P and...

Suppose that the market for a children’s book is given by the following demand and supply...

Suppose that the market for a children’s book is given by the following demand and supply functions: Demand: QD= 98 - 4P Supply: QS= -4 + 2P Where: QD and QS are quantity demand and quantity supplied respectively, and P is the price. The equilibrium quantity is ______ units

The market demand for a product is Q_d=500−4PQd=500−4P and the total supply curve of the smaller...

The market demand for a product is Q_d=500−4PQd=500−4P and the total supply curve of the smaller firms is Q_s =20+6PQs=20+6P. The total cost curve for the dominant firm is TC=20QTC=20Q How many units of output will the dominant firm produce?

Market demand is given as QD = 220 – 4P. Market supply is given as QS...

Market demand is given as QD = 220 – 4P. Market supply is given as QS = 2P + 40. Each identical firm has MC = 0.5Q and ATC = 0.25Q. What is a firm’s average total cost? 2. Describe what happens to output, price, and economic profit in the short run and in the long run in a competitive market following: a) An increase in demand. b) A decrease in demand. c) The adoption of a new technology that...

[1] A perfectly competitive aluminum producer is currently producing a quantity where the market price is...

[1] A perfectly competitive aluminum producer is currently producing a quantity where the market price is $0.67 per pound (i.e., 67 cents per pound), average total cost is $0.70, and average variable cost of $0.60 (which corresponds to the minimum point on the average variable cost curve). Would you recommend this firm expand output, contract output, or shut down in the short-run? Provide a graph to illustrate your answer. [2] Suppose the local crawfish market is perfectly competitive, with the...

Question 5 (15 marks) Market demand is given as QD = 120 - P. Market supply is given as QS = 4P. Each identical firm has MC = 6Q and ATC = 3Q. Showing your calculations, answer the following questions: A) What quantity of output will a typical firm produce? (5 marks) B) What is a typical firm's average total cost? (5 marks) C) What is a a typical firm's profit? (5 marks)

Question 5 (15 marks) Market demand is given as QD = 120 - P. Market supply is given as QS = 4P. Each identical firm has MC = 6Q and ATC = 3Q. Showing your calculations, answer the following questions: A) What quantity of output will a typical firm produce? (5 marks) B) What is a typical firm's average total cost? (5 marks) C) What is a a typical firm's profit? (5 marks)

4. The market for apples is perfectly competitive. The market demand for apples has been estimated as follows: Qd = 54,400 - 900P, where Q is measured in thousands of cases The market supply is Qs = 4000 + 800P Each apple producer has a total cost function given as: TC = 2400 +59 +0.0625q? Find the market price and quantity, firm output and profits. How many firms are there? Market price $ Market output Firm output Firm profits $...

4. The market for apples is perfectly competitive. The market demand for apples has been estimated as follows: Qd = 54,400 - 900P, where Q is measured in thousands of cases The market supply is Qs = 4000 + 800P Each apple producer has a total cost function given as: TC = 2400 +59 +0.0625q? Find the market price and quantity, firm output and profits. How many firms are there? Market price $ Market output Firm output Firm profits $...

4. The market for apples is perfectly competitive. The market demand for apples has been estimated as follows: Qd = 54,400 - 900P, where is measured in thousands of cases The market supply is Qs 4000 + 800P Each apple producer has a total cost function given as: TC = 2400 + 54 +0.0625q? Find the market price and quantity, firm output and profits. How many firms are there? Market price $. Market output. Firm output Firm profits $ Number...

4. The market for apples is perfectly competitive. The market demand for apples has been estimated as follows: Qd = 54,400 - 900P, where is measured in thousands of cases The market supply is Qs 4000 + 800P Each apple producer has a total cost function given as: TC = 2400 + 54 +0.0625q? Find the market price and quantity, firm output and profits. How many firms are there? Market price $. Market output. Firm output Firm profits $ Number...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago